Answered step by step

Verified Expert Solution

Question

1 Approved Answer

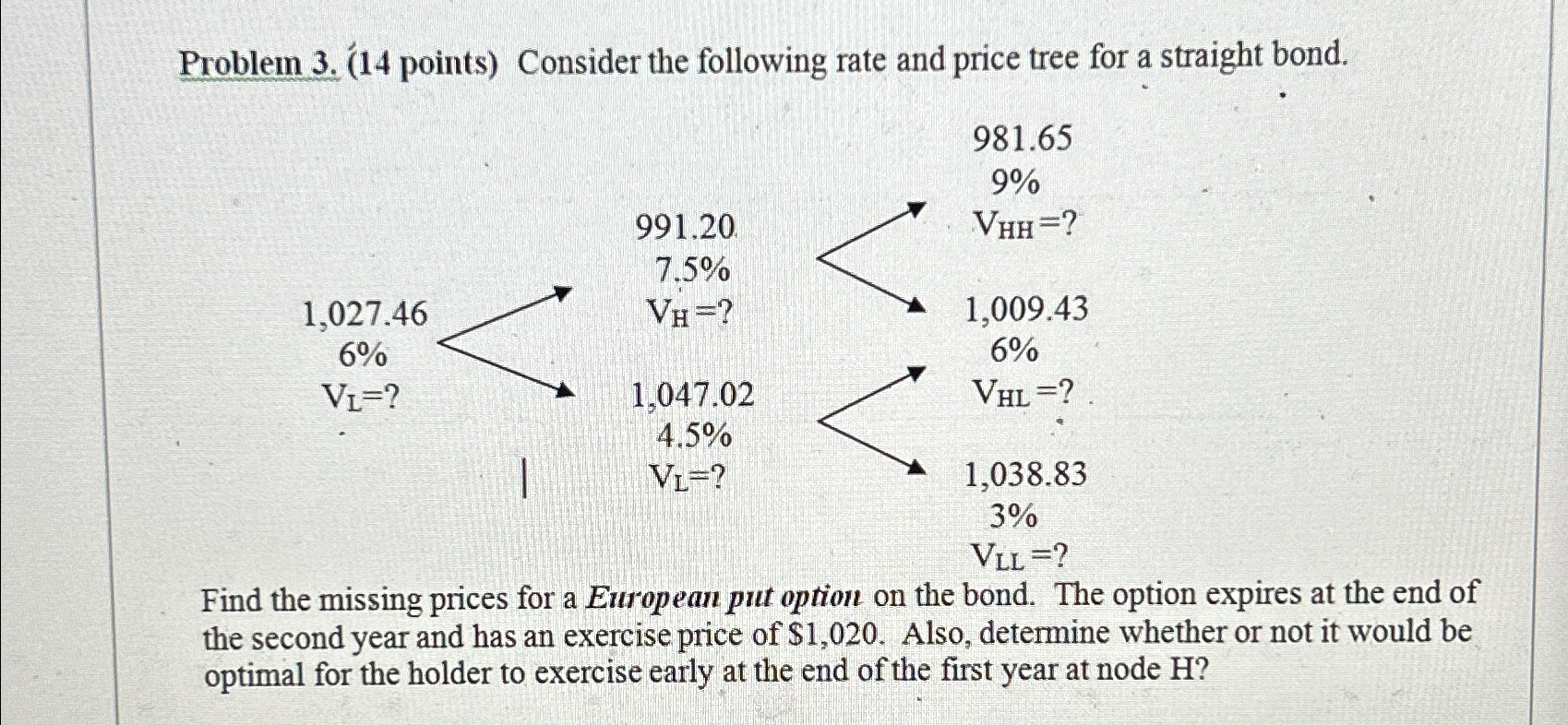

Problem 3. (14 points) Consider the following rate and price tree for a straight bond. 981.65 9% 991.20 VHH=? 7.5% 1,027.46 6% VL=? VH=?

Problem 3. (14 points) Consider the following rate and price tree for a straight bond. 981.65 9% 991.20 VHH=? 7.5% 1,027.46 6% VL=? VH=? 1,009.43 6% 1,047.02 VHL=? 4.5% VL=? 1,038.83 3% VLL =? Find the missing prices for a European put option on the bond. The option expires at the end of the second year and has an exercise price of $1,020. Also, determine whether or not it would be optimal for the holder to exercise early at the end of the first year at node H?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance Applications and Theory

Authors: Marcia Cornett, Troy Adair

3rd edition

1259252221, 007786168X, 9781259252228, 978-0077861681