Answered step by step

Verified Expert Solution

Question

1 Approved Answer

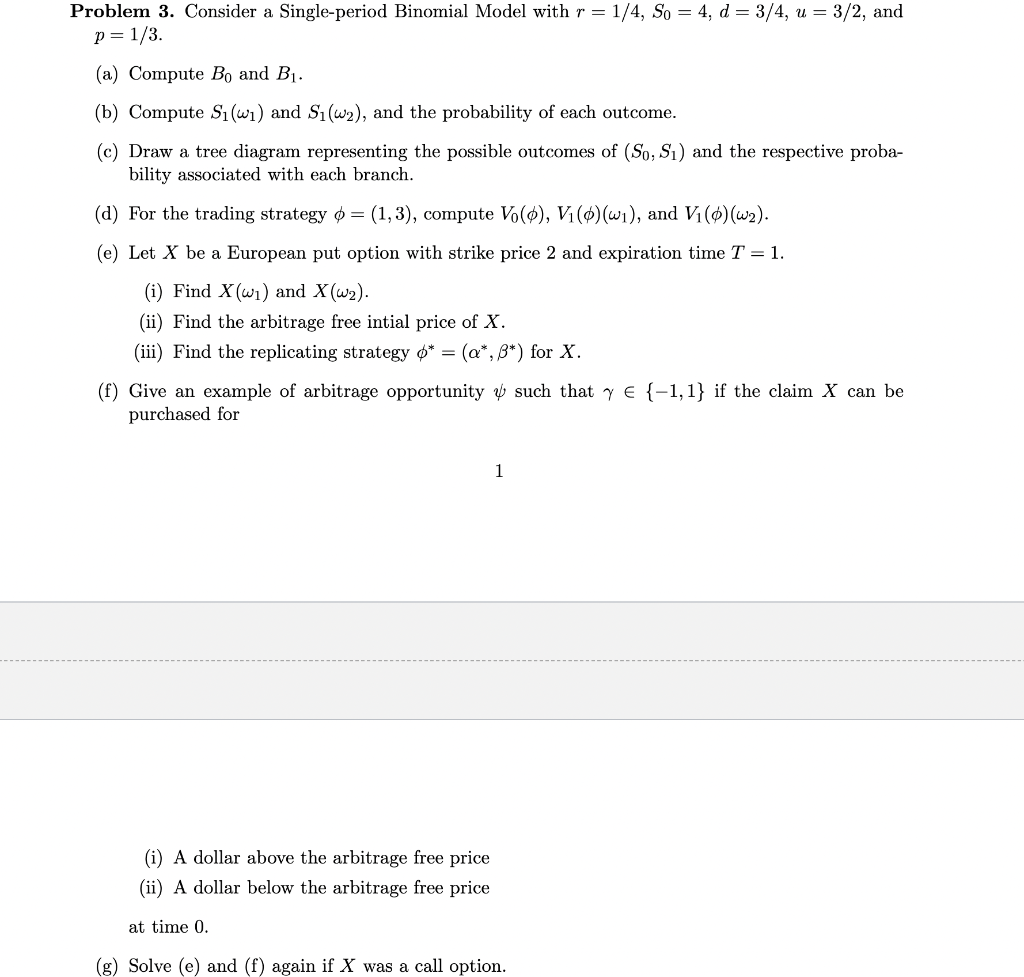

Problem 3. Consider a Single-period Binomial Model with r = 1/4, So = 4, d = 3/4, u = 3/2, and p = 1/3.

Problem 3. Consider a Single-period Binomial Model with r = 1/4, So = 4, d = 3/4, u = 3/2, and p = 1/3. (a) Compute Bo and B. (b) Compute S(w) and S (w2), and the probability of each outcome. (c) Draw a tree diagram representing the possible outcomes of (So, S) and the respective proba- bility associated with each branch. (d) For the trading strategy = (1,3), compute Vo(), V(o)(w), and V()(w2). (e) Let X be a European put option with strike price 2 and expiration time T = 1. (i) Find X(wi) and X(w2). (ii) Find the arbitrage free intial price of X. (iii) Find the replicating strategy o* = (a*, 8*) for X. (f) Give an example of arbitrage opportunity purchased for such that y = {-1,1} if the claim X can be 1 (i) A dollar above the arbitrage free price (ii) A dollar below the arbitrage free price at time 0. (g) Solve (e) and (f) again if X was a call option.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Business Math

Authors: Cheryl Cleaves, Margie Hobbs, Jeffrey Noble

10th edition

133011208, 978-0321924308, 321924304, 978-0133011203