Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Problem 3- Deviations from APT Model The estimated parameters of a three-factor APT model are: R-Rfree = 0.09 +0.03F1 +0.03F2 -0.04F3. Suppose that the risk

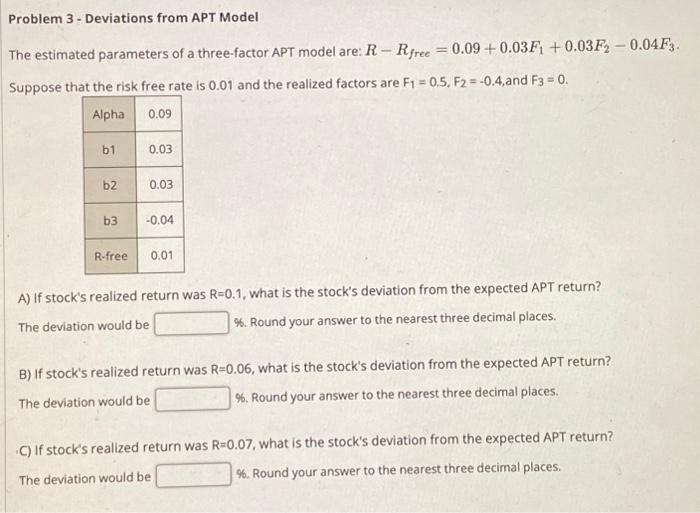

Problem 3- Deviations from APT Model The estimated parameters of a three-factor APT model are: R-Rfree = 0.09 +0.03F1 +0.03F2 -0.04F3. Suppose that the risk free rate is 0.01 and the realized factors are F = 0.5, F2 = -0.4,and F3 = 0. Alpha b1 b2 b3 R-free 0.09 0.03 0.03 -0.04 0.01 A) If stock's realized return was R=0.1, what is the stock's deviation from the expected APT return? The deviation would be %. Round your answer to the nearest three decimal places. B) If stock's realized return was R=0.06, what is the stock's deviation from the expected APT return? The deviation would be %. Round your answer to the nearest three decimal places. C) If stock's realized return was R=0.07, what is the stock's deviation from the expected APT return? %. Round your answer to the nearest three decimal places. The deviation would be

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Mortgage And Interest Rates What You Should Know To Get A Risk Free Deal

Authors: Bert Rivers

1st Edition

979-8866678877