Answered step by step

Verified Expert Solution

Question

1 Approved Answer

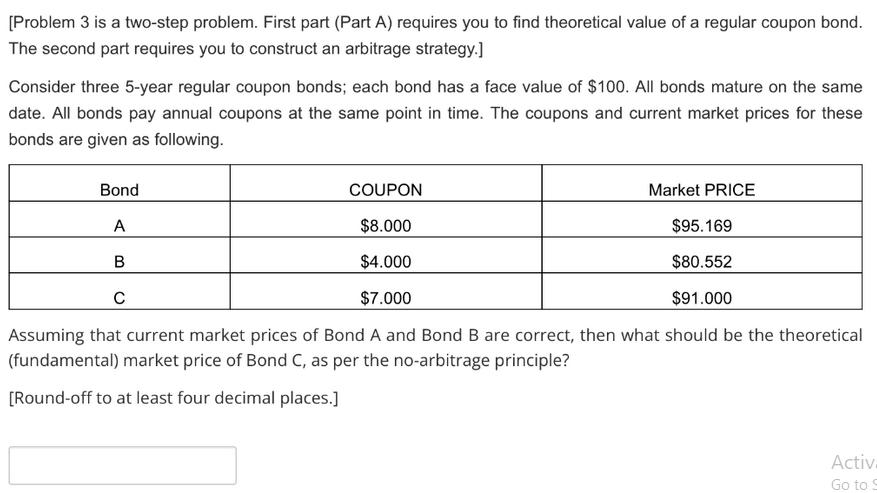

[Problem 3 is a two-step problem. First part (Part A) requires you to find theoretical value of a regular coupon bond. The second part

[Problem 3 is a two-step problem. First part (Part A) requires you to find theoretical value of a regular coupon bond. The second part requires you to construct an arbitrage strategy.] Consider three 5-year regular coupon bonds; each bond has a face value of $100. All bonds mature on the same date. All bonds pay annual coupons at the same point in time. The coupons and current market prices for these bonds are given as following. Bond A B C COUPON $8.000 $4.000 $7.000 Market PRICE $95.169 $80.552 $91.000 Assuming that current market prices of Bond A and Bond B are correct, then what should be the theoretical (fundamental) market price of Bond C, as per the no-arbitrage principle? [Round-off to at least four decimal places.] Activ Go to S

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments

Authors: Zvi Bodie, Alex Kane, Alan J. Marcus

9th Edition

73530700, 978-0073530703