Answered step by step

Verified Expert Solution

Question

1 Approved Answer

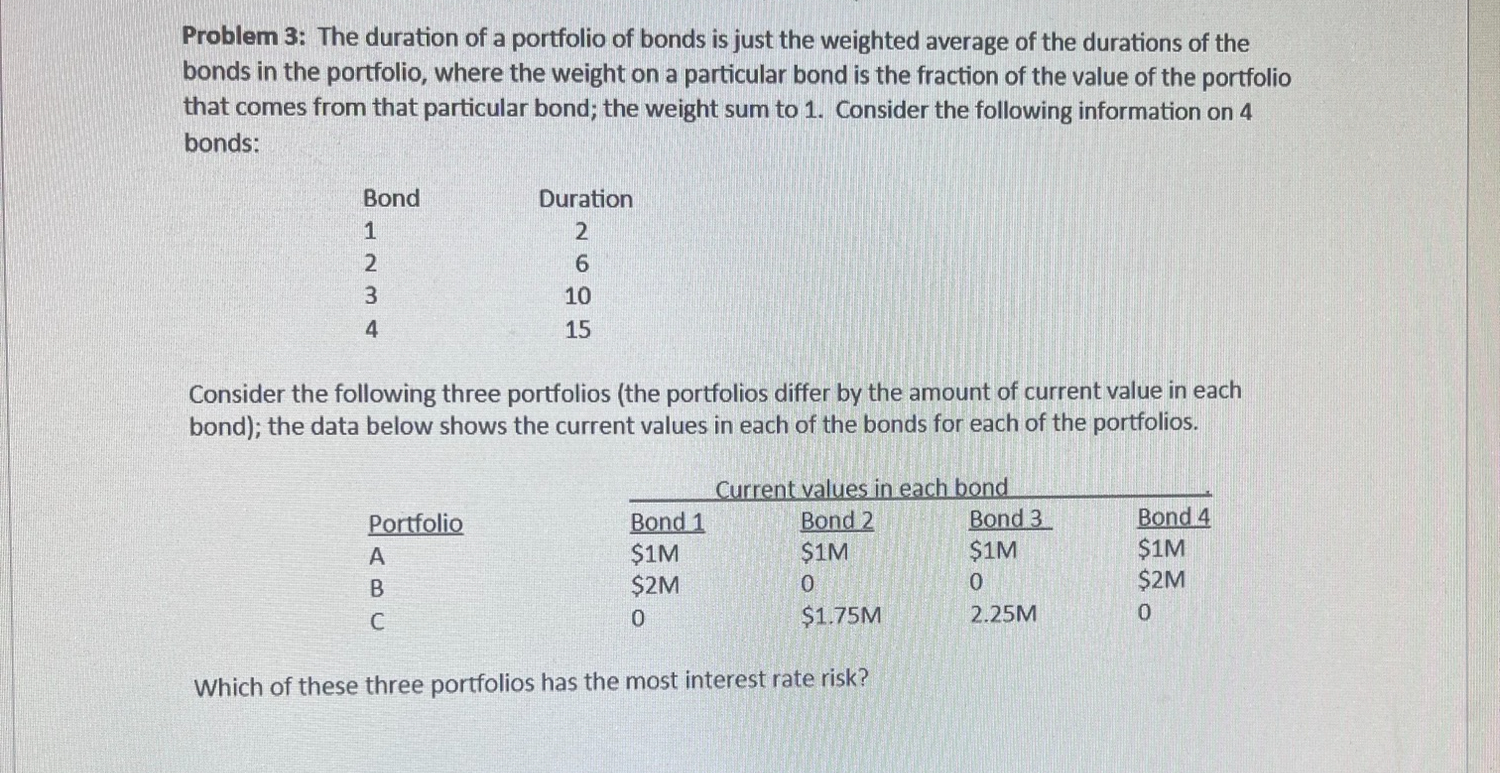

Problem 3 : The duration of a portfolio of bonds is just the weighted average of the durations of the bonds in the portfolio, where

Problem : The duration of a portfolio of bonds is just the weighted average of the durations of the

bonds in the portfolio, where the weight on a particular bond is the fraction of the value of the portfolio

that comes from that particular bond; the weight sum to Consider the following information on

bonds:

Consider the following three portfolios the portfolios differ by the amount of current value in each

bond; the data below shows the current values in each of the bonds for each of the portfolios.

Which of these three portfolios has the most interest rate risk?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Management

Authors: Cheol S. Eun, Bruce G.Resnick

6th Edition

71316973, 978-0071316972, 78034655, 978-0078034657