Answered step by step

Verified Expert Solution

Question

1 Approved Answer

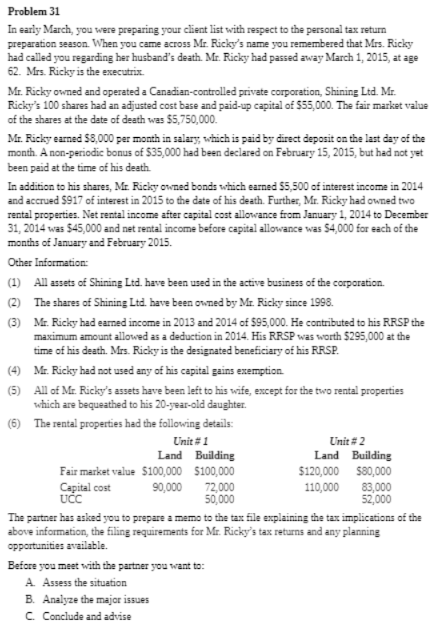

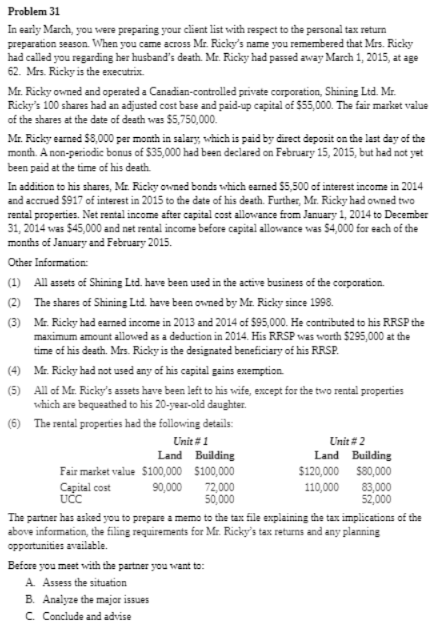

Problem 31 In early March, you were preparing your client list with respect to the personal tax return preparation season. When you came across Mr.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Modern Advanced Accounting in Canada

Authors: Hilton Murray, Herauf Darrell

8th edition

1259087557, 1057317623, 978-1259087554