Answered step by step

Verified Expert Solution

Question

1 Approved Answer

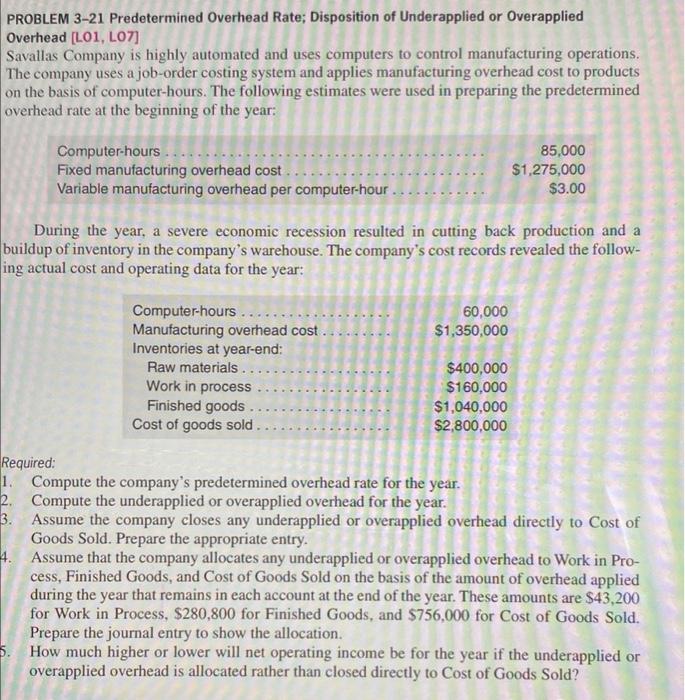

PROBLEM 3-21 Predetermined Overhead Rate; Disposition of Underapplied or Overapplied Overhead (L01, LO7] Savallas Company is highly automated and uses computers to control manufacturing operations.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Strategy Mapping An Interventionist Examination Of A Homebuilders Performance Measurement And Incentive Systems

Authors: Kenneth Merchant

1st Edition

0080965946, 9780080965949