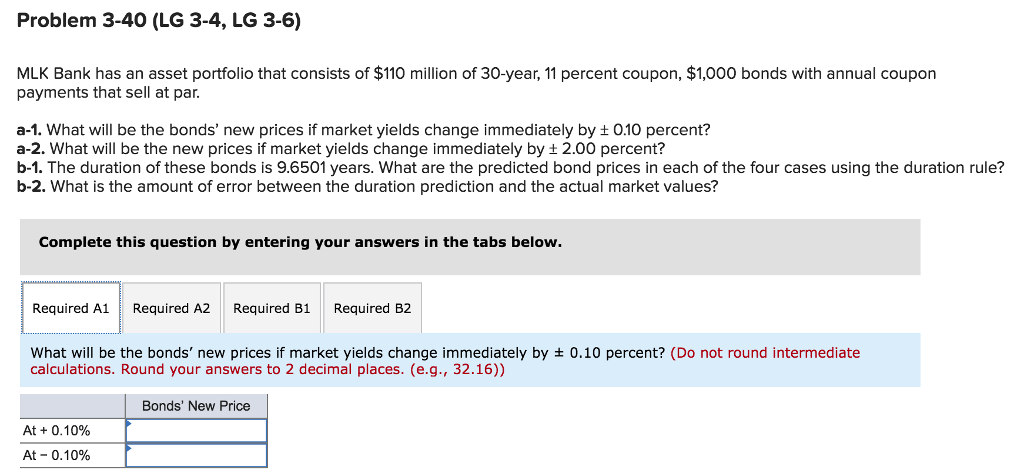

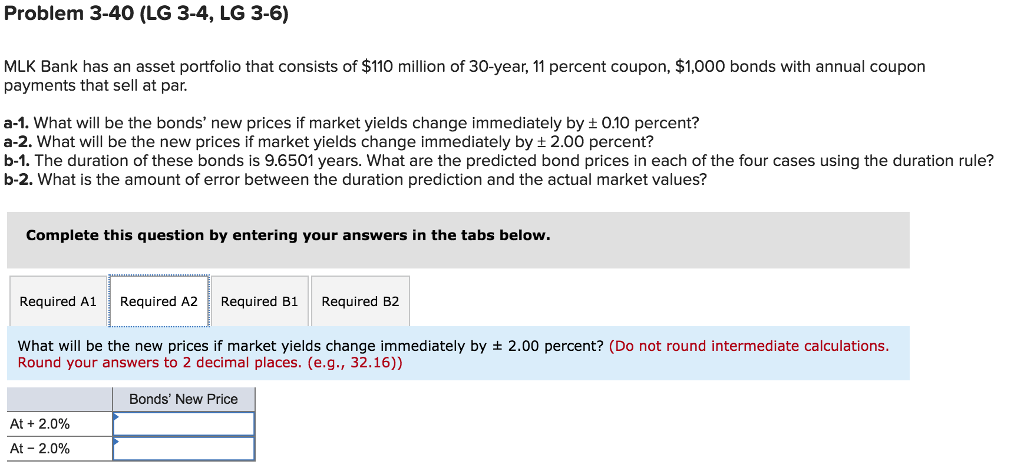

Problem 3-40 (LG 3-4, LG 3-6) MLK Bank has an asset portfolio that consists of $110 million of 30-year, 11 percent coupon, $1,000 bonds with annual coupon payments that sell at par a-1. What will be the bonds' new prices if market yields change immediately by t 0.10 percent? a-2. What will be the new prices if market yields change immediately by t 2.00 percent? b-1. The duration of these bonds is 9.6501 years. What are the predicted bond prices in each of the four cases using the duration rule? b-2. What is the amount of error between the duration prediction and the actual market values? Complete this question by entering your answers in the tabs below. Required A1Required A2 Required B1 Required B2 what will be the bonds, new prices if market yields change immediately by 0.10 percent? (Do not round intermediate calculations. Round your answers to 2 decimal places. (e.g., 32.16)) Bonds' New Price At + 0.10% At-0.10% Problem 3-40 (LG 3-4, LG 3-6) MLK Bank has an asset portfolio that consists of $110 million of 30-year, 11 percent coupon, $1,000 bonds with annual coupon payments that sell at par. a-1. What will be the bonds' new prices if market yields change immediately by t 0.10 percent? a-2. What will be the new prices if market yields change immediately by t 2.00 percent? b-1. The duration of these bonds is 9.6501 years. What are the predicted bond prices in each of the four cases using the duration rule? b-2. What is the amount of error between the duration prediction and the actual market values? Complete this question by entering your answers in the tabs below Required A1Required A2Required B1 Required B2 what will be the new prices if market yields change immediately by Round your answers to 2 decimal places. (e.g., 32.16)) 2.00 percent? (Do not round intermediate calculations Bonds' New Price At + 2.0% At-2.0% MLK Bank has an asset portfolio that consists of $110 million of 30-year, 11 percent coupon, $1,000 bonds with annual coupon payments that sell at par. a-1. What will be the bonds' new prices if market yields change immediately by t 0.10 percent? a-2. What will be the new prices if market yields change immediately by t 2.00 percent? b-1. The duration of these bonds is 9.6501 years. What are the predicted bond prices in each of the four cases using the duration rule? b-2. What is the amount of error between the duration prediction and the actual market values? Complete this question by entering your answers in the tabs below Required A1 Required A2Required B1 Reqired B2 The duration of these bonds is 9.6501 years. What are the predicted bond prices in each of the four cases using the duration rule? (Do not round intermediate calculations. Round your answers to 2 decimal places. (e.g., 32.16)) Bonds' New Price At 0, 1 0% At-0.10% At + 2.0% At-2.0% MLK Bank has an asset portfolio that consists of $110 million of 30-year, 11 percent coupon, $1,000 bonds with annual coupon payments that sell at par. a-1. What will be the bonds' new prices if market yields change immediately by+0.10 percent? a-2. What will be the new prices if market yields change immediately by t 2.00 percent? b-1. The duration of these bonds is 9.6501 years. What are the predicted bond prices in each of the four cases using the duration rule? b-2. What is the amount of error between the duration prediction and the actual market values? Complete this question by entering your answers in the tabs below Required A1 Required A2 Required B1 Required B2 What is the amount of error between the duration prediction and the actual market values? (Do not round intermediate calculations. Round your answers to 2 decimal places. (e.g., 32.16)) Amount of Error At + 0.10% At-0.10% At + 2.0% At-20%