Answered step by step

Verified Expert Solution

Question

1 Approved Answer

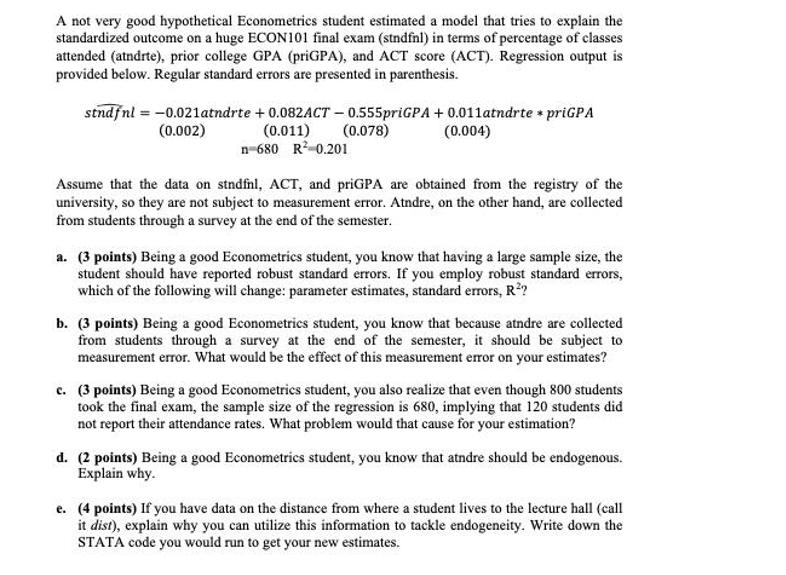

A not very good hypothetical Econometrics student estimated a model that tries to explain the standardized outcome on a huge ECON101 final exam (stndfnl)

A not very good hypothetical Econometrics student estimated a model that tries to explain the standardized outcome on a huge ECON101 final exam (stndfnl) in terms of percentage of classes attended (atndrte), prior college GPA (priGPA), and ACT score (ACT). Regression output is provided below. Regular standard errors are presented in parenthesis. stndfnl = -0.021atndrte + 0.082ACT 0.555priGPA + 0.011atndrte * priGPA (0.078) (0.002) (0.011) n-680 R-0.201 (0.004) Assume that the data on stndfnl, ACT, and priGPA are obtained from the registry of the university, so they are not subject to measurement error. Atndre, on the other hand, are collected from students through a survey at the end of the semester. a. (3 points) Being a good Econometrics student, you know that having a large sample size, the student should have reported robust standard errors. If you employ robust standard errors, which of the following will change: parameter estimates, standard errors, R? b. (3 points) Being a good Econometrics student, you know that because atndre are collected from students through a survey at the end of the semester, it should be subject to measurement error. What would be the effect of this measurement error on your estimates? c. (3 points) Being a good Econometrics student, you also realize that even though 800 students took the final exam, the sample size of the regression is 680, implying that 120 students did not report their attendance rates. What problem would that cause for your estimation? d. (2 points) Being a good Econometrics student, you know that atndre should be endogenous. Explain why. e. (4 points) If you have data on the distance from where a student lives to the lecture hall (call it dist), explain why you can utilize this information to tackle endogeneity. Write down the STATA code you would run to get your new estimates.

Step by Step Solution

★★★★★

3.46 Rating (156 Votes )

There are 3 Steps involved in it

Step: 1

a If robust standard error is employed then parameter estimates and R2 value remain the same However ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Econometric Analysis

Authors: William H. Greene

5th Edition

130661899, 978-0130661890