Answered step by step

Verified Expert Solution

Question

1 Approved Answer

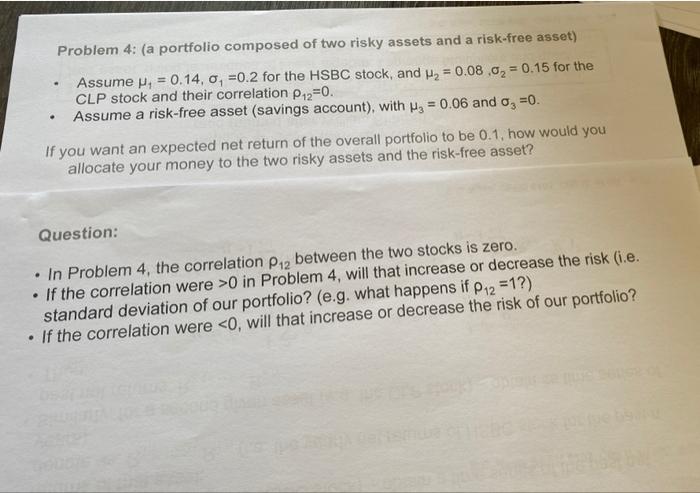

Problem 4: (a portfolio composed of two risky assets and a risk-free asset) Assume , = 0.14, 0, =0.2 for the HSBC stock, and H2

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Crush Debt Now Pay Off Debt Fight Collection Lawsuits Negotiate And Settle Your Debts Using 3 Step Strategy To Be Debt Free

Authors: Tom Cromwell

1st Edition

979-8577027728