Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Problem 4. A stock index St follows the lognormal stock price model with the lognormal distribution. ln(St/S0)=N(t,2t), where =0.12 and =0.3 and S0=50. You have

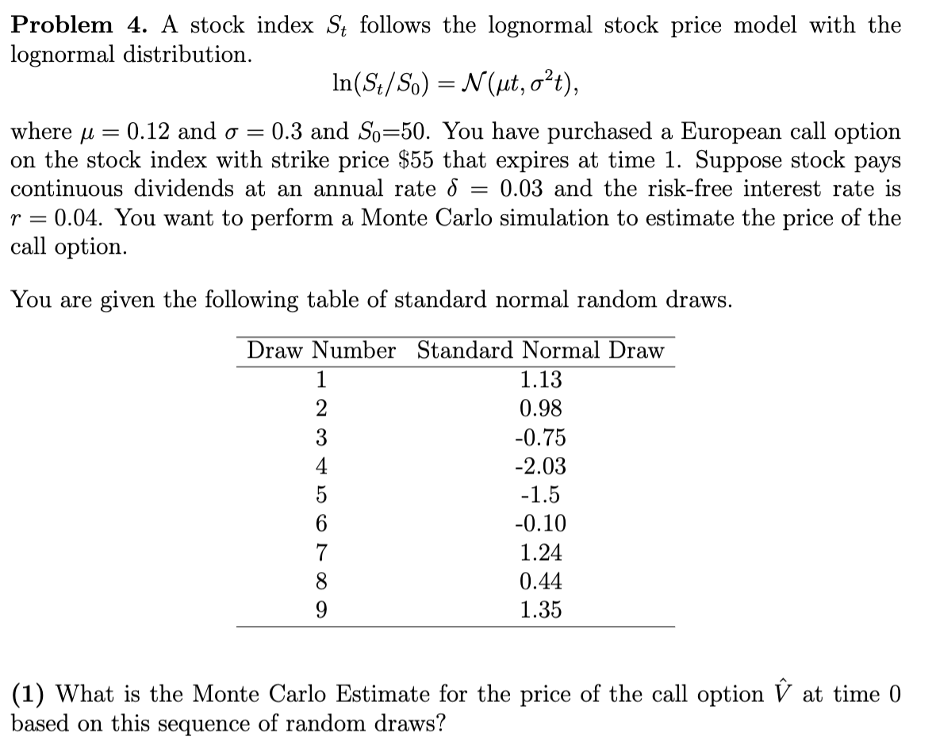

Problem 4. A stock index St follows the lognormal stock price model with the lognormal distribution. ln(St/S0)=N(t,2t), where =0.12 and =0.3 and S0=50. You have purchased a European call option on the stock index with strike price $55 that expires at time 1 . Suppose stock pays continuous dividends at an annual rate =0.03 and the risk-free interest rate is r=0.04. You want to perform a Monte Carlo simulation to estimate the price of the call option. You are given the following table of standard normal random draws. (1) What is the Monte Carlo Estimate for the price of the call option V^ at time 0 based on this sequence of random draws

Problem 4. A stock index St follows the lognormal stock price model with the lognormal distribution. ln(St/S0)=N(t,2t), where =0.12 and =0.3 and S0=50. You have purchased a European call option on the stock index with strike price $55 that expires at time 1 . Suppose stock pays continuous dividends at an annual rate =0.03 and the risk-free interest rate is r=0.04. You want to perform a Monte Carlo simulation to estimate the price of the call option. You are given the following table of standard normal random draws. (1) What is the Monte Carlo Estimate for the price of the call option V^ at time 0 based on this sequence of random draws Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Markets And Institutions

Authors: Anthony Saunders, Marcia Cornett

5th Edition

0078034663, 978-0078034664