Question

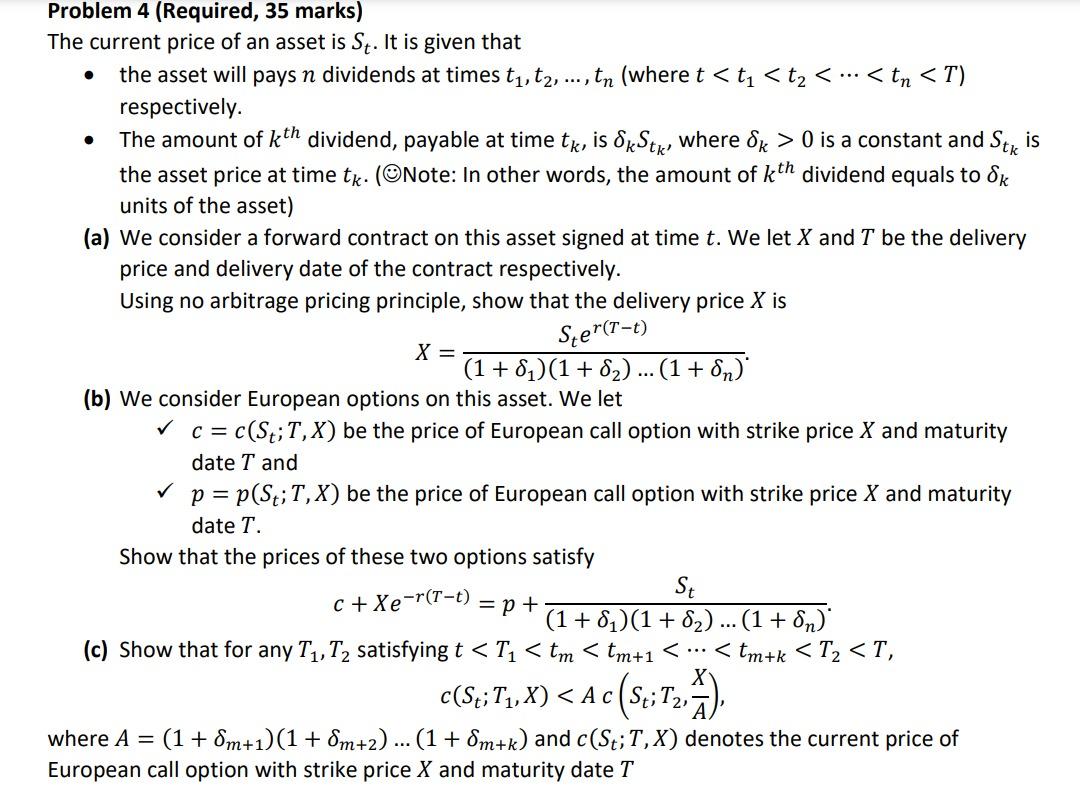

Problem 4 (Required, 35 marks) The current price of an asset is . It is given that the asset will pays dividends at times 1,2,

Problem 4 (Required, 35 marks) The current price of an asset is . It is given that the asset will pays dividends at times 1,2, , (where < 1 < 2 < < < ) respectively. The amount of dividend, payable at time , is , where > 0 is a constant and is the asset price at time . (Note: In other words, the amount of dividend equals to units of the asset) (a) We consider a forward contract on this asset signed at time . We let and be the delivery price and delivery date of the contract respectively. Using no arbitrage pricing principle, show that the delivery price is = () (1 + 1 )(1 + 2 ) (1 + ) . (b) We consider European options on this asset. We let = ( ; , ) be the price of European call option with strike price and maturity date and = ( ; , ) be the price of European call option with strike price and maturity date . Show that the prices of these two options satisfy + () = + (1 + 1 )(1 + 2 ) (1 + ) . (c) Show that for any 1, 2 satisfying < 1 < < +1 < < + < 2 < , ( ; 1, ) < ( ; 2, ), where = (1 + +1 )(1 + +2 ) (1 + + ) and ( ; , ) denotes the current price of European call option with strike price and maturity date

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance Capital A Study In The Latest Phase Of Capitalist Development

Authors: Rudolph Hilferding

1st Edition

0415436648, 978-0415436649