Answered step by step

Verified Expert Solution

Question

1 Approved Answer

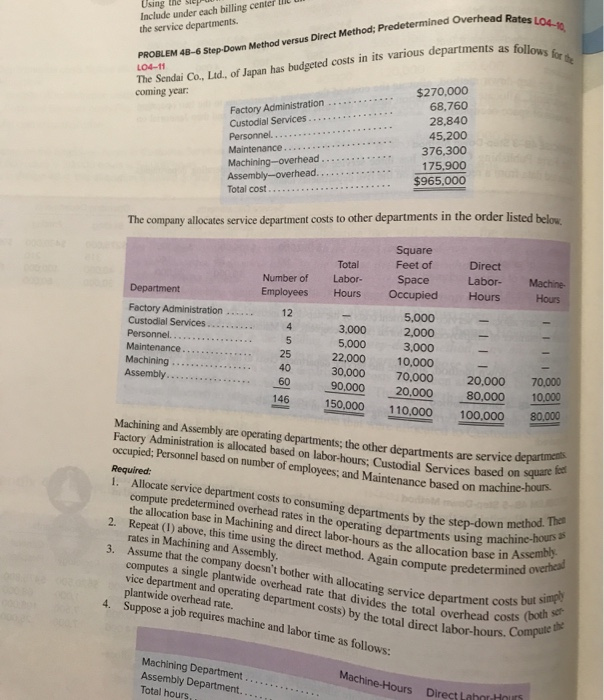

PROBLEM 48-6 Step-Down Method versus Direct Method; Predetermined Overhead Rates L04-10 The Sendai Co., Ltd., of Japan has budgeted costs in its various departments as

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quality And GMP Auditing Clear And Simple

Authors: James L. Vesper

1st Edition

0367400901, 978-0367400903