Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Problem 5. (9 pts) Consider three uncorrelated risky assets in the market. Each of the assets has variance 1 . The mean returns are given

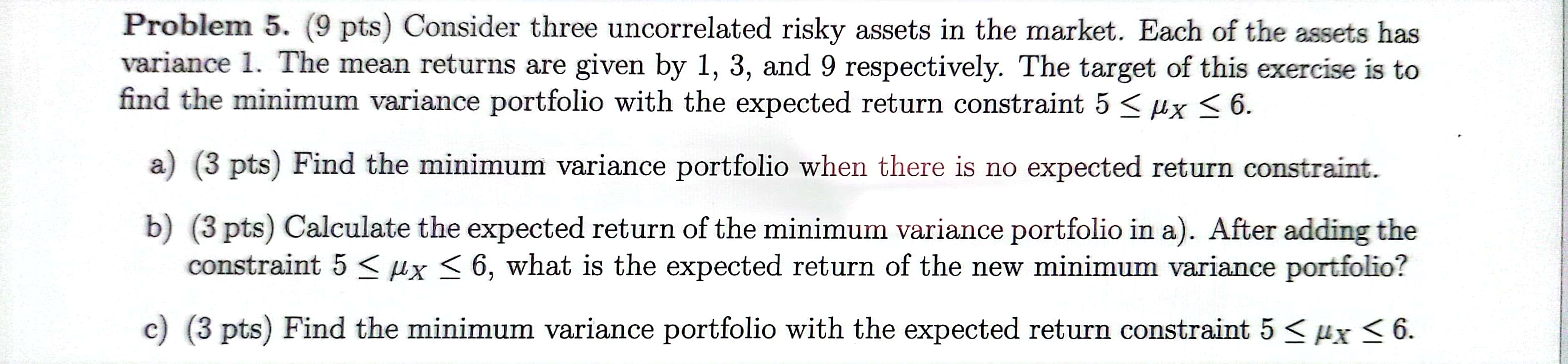

Problem 5. (9 pts) Consider three uncorrelated risky assets in the market. Each of the assets has variance 1 . The mean returns are given by 1,3 , and 9 respectively. The target of this exercise is to find the minimum variance portfolio with the expected return constraint 5X6. a) (3 pts) Find the minimum variance portfolio when there is no expected return constraint. b) (3 pts) Calculate the expected return of the minimum variance portfolio in a). After adding the constraint 5X6, what is the expected return of the new minimum variance portfolio? c) (3 pts) Find the minimum variance portfolio with the expected return constraint 5X6

Problem 5. (9 pts) Consider three uncorrelated risky assets in the market. Each of the assets has variance 1 . The mean returns are given by 1,3 , and 9 respectively. The target of this exercise is to find the minimum variance portfolio with the expected return constraint 5X6. a) (3 pts) Find the minimum variance portfolio when there is no expected return constraint. b) (3 pts) Calculate the expected return of the minimum variance portfolio in a). After adding the constraint 5X6, what is the expected return of the new minimum variance portfolio? c) (3 pts) Find the minimum variance portfolio with the expected return constraint 5X6 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Valuation Workbook

Authors: James Hitchner, Michael J. Mard

1st Edition

0471220833, 978-0471220831