Answered step by step

Verified Expert Solution

Question

1 Approved Answer

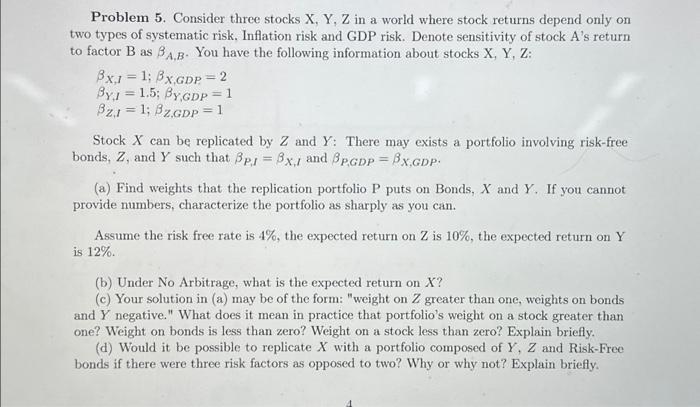

Problem 5. Consider three stocks X, Y, Z in a world where stock returns depend only on two types of systematic risk, Inflation risk and

Problem 5. Consider three stocks X, Y, Z in a world where stock returns depend only on two types of systematic risk, Inflation risk and GDP risk. Denote sensitivity of stock A's return to factor B as BA,B. You have the following information about stocks X, Y, Z: Bx,11; 8x,GDP = 2 ByI 1.5; By.GDP = 1 = BzI1; BZ.GDP = 1 = Stock X can be replicated by Z and Y: There may exists a portfolio involving risk-free bonds, Z, and Y such that 3P,1 = 3x,I and BP,GDP = x,GDP. (a) Find weights that the replication portfolio P puts on Bonds, X and Y. If you cannot provide numbers, characterize the portfolio as sharply as you can. Assume the risk free rate is 4%, the expected return on Z is 10%, the expected return on Y is 12%. (b) Under No Arbitrage, what is the expected return on X? (c) Your solution in (a) may be of the form: "weight on Z greater than one, weights on bonds and Y negative." What does it mean in practice that portfolio's weight on a stock greater than one? Weight on bonds is less than zero? Weight on a stock less than zero? Explain briefly. (d) Would it be possible to replicate X with a portfolio composed of Y, Z and Risk-Free bonds if there were three risk factors as opposed to two? Why or why not? Explain briefly.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Ziglar On Selling The Ultimate Handbook For The Complete Sales Professional

Authors: Zig Ziglar

1st Edition

0785288937, 978-0785288930