Answered step by step

Verified Expert Solution

Question

1 Approved Answer

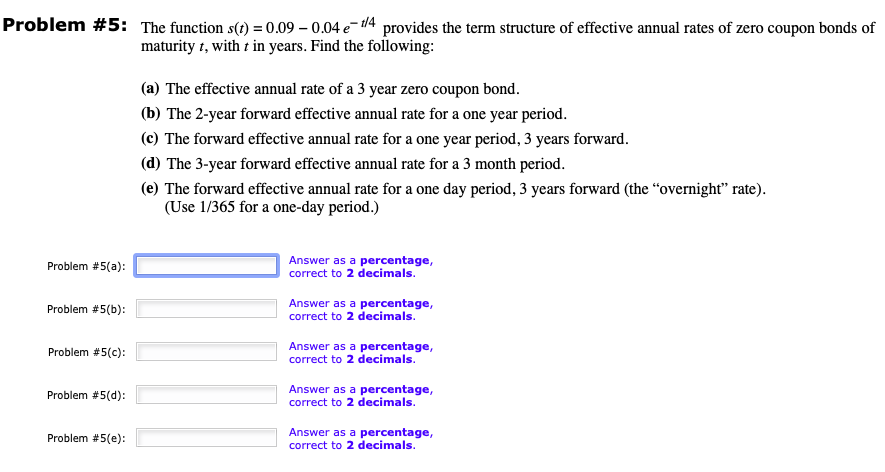

Problem #5: The function s(t) = 0.09 -0.04 e - 1/4 provides the term structure of effective annual rates of zero coupon bonds of maturity

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Managerial Finance

Authors: Lawrence J Gitman, Chad J Zutter

7th Edition

0133546403, 9780133546408