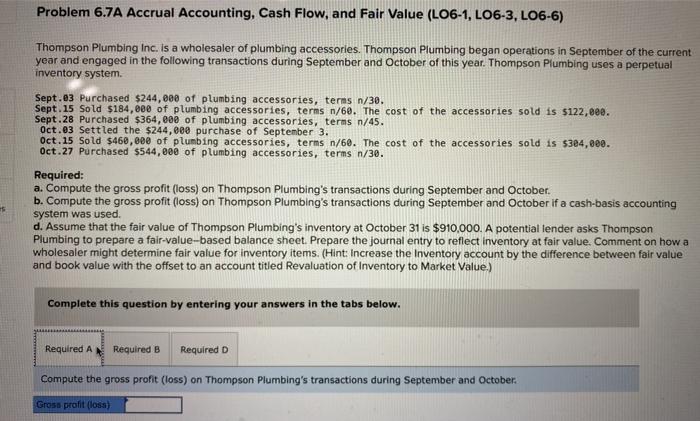

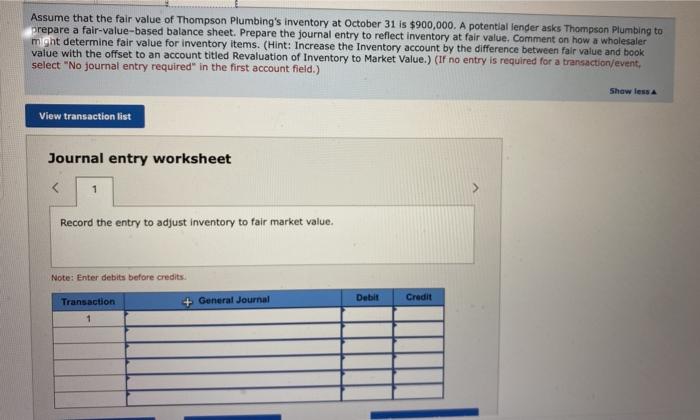

Problem 6.7A Accrual Accounting, Cash Flow, and Fair Value (L06-1, LO6-3, L06-6) Thompson Plumbing Inc. is a wholesaler of plumbing accessories. Thompson Plumbing began operations in September of the current year and engaged in the following transactions during September and October of this year. Thompson Plumbing uses a perpetual inventory system. Sept.3 Purchased $244,000 of plumbing accessories, terms n/30. Sept. 15 Sold $184,000 of plumbing accessories, terms n/60. The cost of the accessories sold is $122,888. Sept. 28 Purchased $364,000 of plumbing accessories, terms n/45. Oct.03 Settled the $244,000 purchase of September 3. Oct. 15 Sold $460,000 of plumbing accessories, terms n/60. The cost of the accessories sold is $384,000. Oct.27 Purchased $544,000 of plumbing accessories, terms n/30. Required: a. Compute the gross profit (loss) on Thompson Plumbing's transactions during September and October. b. Compute the gross profit (loss) on Thompson Plumbing's transactions during September and October if a cash-basis accounting system was used. d. Assume that the fair value of Thompson Plumbing's inventory at October 31 is $910,000. A potential tender asks Thompson Plumbing to prepare a fair-value-based balance sheet. Prepare the journal entry to reflect inventory at fair value. Comment on how a wholesaler might determine fair value for inventory items. (Hint: Increase the inventory account by the difference between fair value and book value with the offset to an account titled Revaluation of Inventory to Market Value) Complete this question by entering your answers in the tabs below. Required A Required B Required D Compute the gross profit (loss) on Thompson Plumbing's transactions during September and October Gross profit (loss) Compute the gross profit (loss) on Thompson Plumbing's transactions during September and October if a cash-basis accounting system was used. Gross profit (los) Assume that the fair value of Thompson Plumbing's inventory at October 31 is $900,000. A potential lender asks Thompson Plumbing to Prepare a fair-value-based balance sheet. Prepare the journal entry to reflect inventory at fair value. Comment on how a wholesaler might determine fair value for inventory items. (Hint: Increase the Inventory account by the difference between fair value and book value with the offset to an account titled Revaluation of Inventory to Market Value.) (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) Show less View transaction list Journal entry worksheet Record the entry to adjust inventory to fair market value. Note: Enter debits before credits Credit Debit + General Journal Transaction 1