Answered step by step

Verified Expert Solution

Question

1 Approved Answer

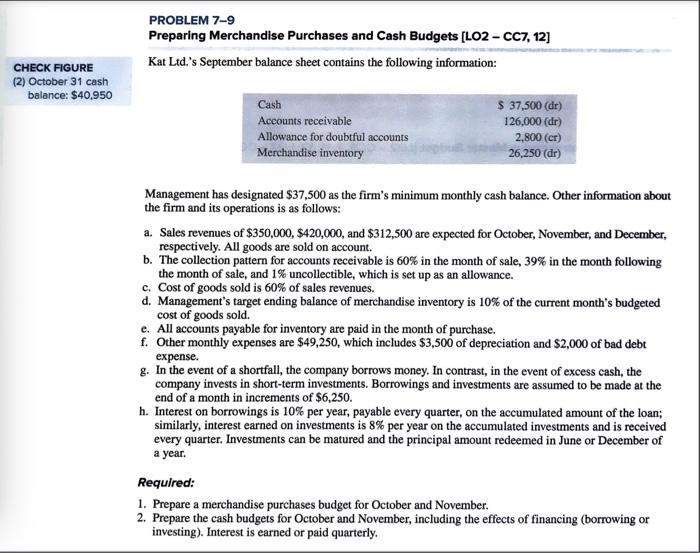

PROBLEM 7-9 Preparing Merchandise Purchases and Cash Budgets [LO2-CC7, 12] Kat Ltd.'s September balance sheet contains the following information: CHECK FIGURE (2) October 31 cash

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Internal Audit Emphasis Management In Organizations

Authors: Juarez Pinto, Anísio Cândido Pereira, Joshua Onome Imoniana

1st Edition

3659942332, 978-3659942334