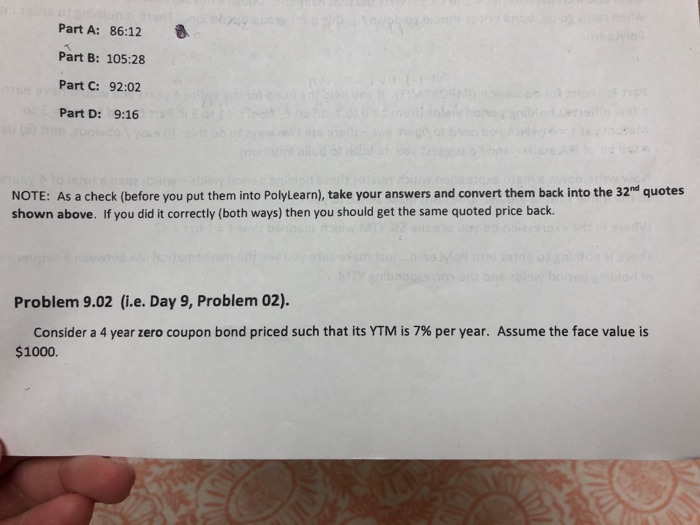

Problem 9.02

Part A: 86:12 Part B: 105:28 Part C: 92:02 Part D: 9:16 NOTE: As a check (before you put them into Polylearn), take your answers and convert them back into the 32" quotes shown above. If you did it correctly (both ways) then you should get the same quoted price back. Problem 9.02 (i.e. Day 9, Problem 02). Consider a 4 year zero coupon bond priced such that its YTM is 7% per year. Assume the face value is $1000. Part A: Determine the dollar price of the bond. (Enter the dollar price into PolyLearn, such as $876.25 (without the dollar sign)). Do not enter the 32nd conventional equivalent price. Part B: Now assume that one year later interest rates have fallen and now the bond has a YTM of 5% (down from 7% one year earlier). What is the dollar price of the bond now? Part C: If you purchased the bond for price computed in Part A and sold it one year later for the price computed in Part B, then what is the holding period yield? Le. what is the holding period yield from t = 0 to t = 1? Enter your answer as a decimal, not as a percent. Point for Group discussion: Why is it that your answer to Part C is not equal to 7% (YTM In Part A) or 5% (YTM in Part B)? Part D: With only one year remaining on the bond le at t = 3), the YTM on the bond is 10%. Compute the annualized effective holding period yield assuming you hold the bond from t 1 (when it was, as described in Part B) tot 3. Notice that this rate spans the two year period from t = 1 tot 3, but should be expressed as an annual value (in decimal form). Enter the effective annualized holding period yield into Polylearn. Part Notice that at t - 1 the YTM was 5%, but 2 years later the YTM Increased to 10% - yet the price of the bond also increased from t - 1 tot 3. WHY did that happen? Doesn't this seem to contradict the idea that when rates go up, bond prices should go down? This is for group discussion. There is nothing to enter into Polylearn. Bart F. Point for discussion (IMPORTANT). If you held the bond for the entire 4 years you would have earned few different holding period yields (from 0 to 1 in Part C, from t 1 to 3 in Part D. and from t= 3 to Maturity at t = 4 (which you need to figure out there are two ways to do this: (1) easy / obvious, and (ii) using tad bit of IRR math - and I'd suggest you do both to build intuition). Now write down a math expression which relates these holding period yields - which span a total of 4 years - to the initial YTM of 7.00%. Does this make sense to you? where in the expression do you see the 5% YTM which spanned timet1 tot 47 There is not is nothing to enter into Polylearn...just make sure you see the mathematical link between a sequence of holding period yields and the corresponding YTM