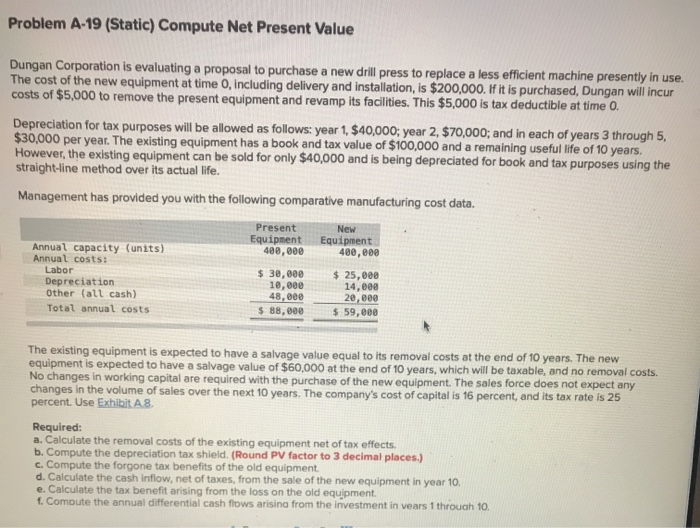

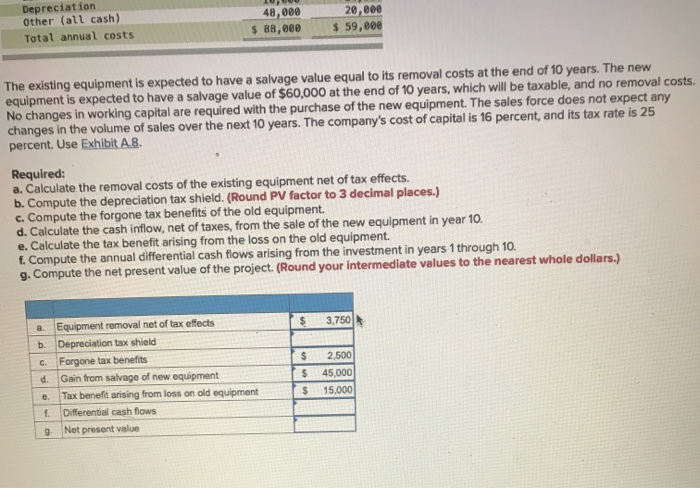

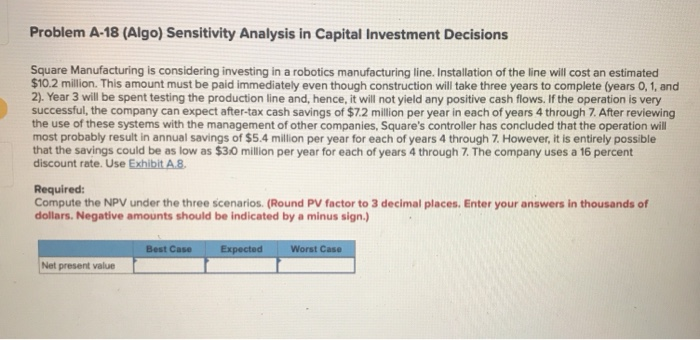

Problem A-19 (Static) Compute Net Present Value Dungan Corporation is evaluating a proposal to purchase a new drill press to replace a less efficient machine presently in use. The cost of the new equipment at time o, including delivery and installation, is $200,000. If it is purchased, Dungan will incur costs of $5,000 to remove the present equipment and revamp its facilities. This $5,000 is tax deductible at time 0. Depreciation for tax purposes will be allowed as follows: year 1, $40,000; year 2, $70,000; and in each of years 3 through 5. $30,000 per year. The existing equipment has a book and tax value of $100,000 and a remaining useful life of 10 years. However, the existing equipment can be sold for only $40,000 and is being depreciated for book and tax purposes using the straight-line method over its actual life. Management has provided you with the following comparative manufacturing cost data. Present Equipment 400,000 New Equipment 400,000 Annual capacity (units) Annual costs: Labor Depreciation Other (all cash) Total annual costs $ 30,000 10,000 48,000 $ 88,000 $ 25,000 14,000 20,000 $ 59,000 The existing equipment is expected to have a salvage value equal to its removal costs at the end of 10 years. The new equipment is expected to have a salvage value of $60,000 at the end of 10 years, which will be taxable, and no removal costs. No changes in working capital are required with the purchase of the new equipment. The sales force does not expect any changes in the volume of sales over the next 10 years. The company's cost of capital is 16 percent, and its tax rate is 25 percent. Use Exhibit A 8. Required: a. Calculate the removal costs of the existing equipment net of tax effects. b. Compute the depreciation tax shield. (Round PV factor to 3 decimal places.) c. Compute the forgone tax benefits of the old equipment. d. Calculate the cash inflow, net of taxes, from the sale of the new equipment in year 10. e. Calculate the tax benefit arising from the loss on the old equipment f. Comoute the annual differential cash flows arisina from the investment in vears 1 through 10. Depreciation Other (all cash) Total annual costs 48,000 $ 88,000 20, eee $ 59,800 The existing equipment is expected to have a salvage value equal to its removal costs at the end of 10 years. The new equipment is expected to have a salvage value of $60,000 at the end of 10 years, which will be taxable, and no removal costs. No changes in working capital are required with the purchase of the new equipment. The sales force does not expect any changes in the volume of sales over the next 10 years. The company's cost of capital is 16 percent, and its tax rate is 25 percent. Use Exhibit A.8. Required: a. Calculate the removal costs of the existing equipment net of tax effects. b. Compute the depreciation tax shield. (Round PV factor to 3 decimal places.) c. Compute the forgone tax benefits of the old equipment. d. Calculate the cash inflow, net of taxes, from the sale of the new equipment in year 10. e. Calculate the tax benefit arising from the loss on the old equipment. f. Compute the annual differential cash flows arising from the investment in years 1 through 10. g. Compute the net present value of the project. (Round your intermediate values to the nearest whole dollars.) 3,750 $ a. Equipment removal net of tax effects b Depreciation tax shield C Forgone tax benefits d. Gain from salvage of new equipment e. Tax benefit arising from loss on old equipment Differential cash flows 9 Net present value $ $ 2,500 45,000 15,000 Problem A-18 (Algo) Sensitivity Analysis in Capital Investment Decisions Square Manufacturing is considering investing in a robotics manufacturing line. Installation of the line will cost an estimated $10.2 million. This amount must be paid immediately even though construction will take three years to complete (years 0, 1, and 2). Year 3 will be spent testing the production line and, hence, it will not yield any positive cash flows. If the operation is very successful, the company can expect after-tax cash savings of $7.2 million per year in each of years 4 through 7. After reviewing the use of these systems with the management of other companies, Square's controller has concluded that the operation will most probably result in annual savings of $5.4 million per year for each of years 4 through 7. However, it is entirely possible that the savings could be as low as $3.0 million per year for each of years 4 through 7. The company uses a 16 percent discount rate. Use Exhibit A.8. Required: Compute the NPV under the three scenarios. (Round PV factor to 3 decimal places. Enter your answers in thousands of dollars. Negative amounts should be indicated by a minus sign.) Best Case Expected Worst Case Net present value