Question

Problem Karen Johnson, CFO for Raucous Roasters (RR), a specialty coffee manufacturer, is rethinking her companys working capital policy in light of a recent scare

Problem

Karen Johnson, CFO for Raucous Roasters (RR), a specialty coffee manufacturer, is rethinking her companys working capital policy in light of a recent scare she faced when RRs corporate banker, citing a nationwide credit crunch, balked at renewing RRs line of credit. Had the line of credit not been renewed, RR would not have been able to make payroll, potentially forcing the company out of business. Although the line of credit was ultimately renewed, the scare has forced Johnson to examine carefully each component of RRs working capital to make sure it is needed, with the goal of determining whether the line of credit can be eliminated entirely. In addition to (possibly) freeing RR from the need for a line of credit, Johnson is well aware that reducing working capital can also add value to a company by improving its EVA (Economic Value Added). In her corporate finance course Johnson learned that EVA is calculated by taking net operating profit after taxes (NOPAT) and then subtracting the dollar cost of all the capital the firm uses:

If EVA is positive, then the firms management is creating value. On the other hand, if EVA is negative, then the firm is not covering its cost of capital and stockholders value is being eroded. If RR could generate its current level of sales with fewer assets, it would need less capital. This would, other things held constant, lower capital costs and increase its EVA.

Historically, RR has done little to examine working capital, mainly because of poor communication among business functions. In the past, the production manager resisted Johnsons efforts to question his holdings of raw materials, the marketing manager resisted questions about finished goods, the sales staff resisted questions about credit policy (which affects accounts receivable), and the treasurer did not want to talk about the cash and securities balances. However, with the recent credit scare, this resistance became unacceptable and Johnson has undertaken a company-wide examination of cash, marketable securities, inventory, and accounts receivable levels.

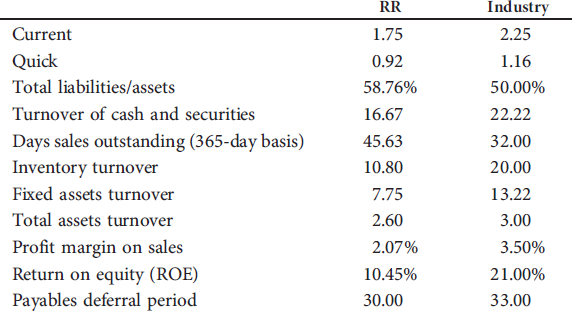

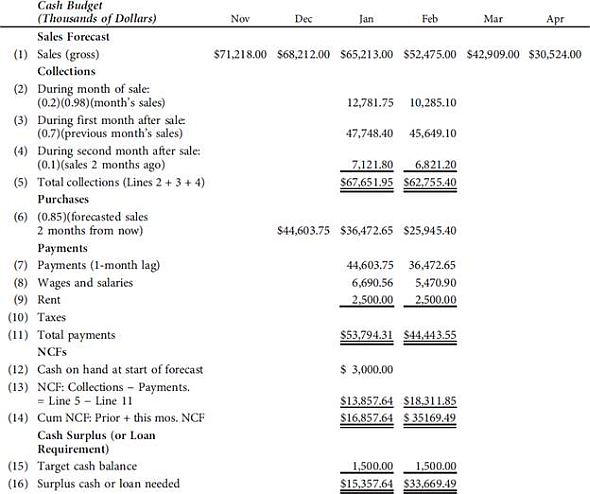

Johnson also knows that decisions about working capital cannot be made in a vacuum. For example, if inventories could be lowered without adversely affecting operations, then less capital would be required, the dollar cost of capital would decline, and EVA would increase. However, lower raw materials inventories might lead to production slowdowns and higher costs, and lower finished goods inventories might lead to stock-outs and loss of sales. So, before inventories are changed, it will be necessary to study operating as well as financial effects. The situation is the same with regard to cash and receivables. Johnson has begun her investigation by collecting the ratios shown below. (The partial cash budget shown after the ratios is used later in this mini case.)

EVA=NOPATCapitalcosts=EBIT(1T)WACC(Totalcapitalemployed) \begin{tabular}{lcc} & RR & Industry \\ \hline Current & 1.75 & 2.25 \\ Quick & 0.92 & 1.16 \\ Total liabilities/assets & 58.76% & 50.00% \\ Turnover of cash and securities & 16.67 & 22.22 \\ Days sales outstanding (365-day basis) & 45.63 & 32.00 \\ Inventory turnover & 10.80 & 20.00 \\ Fixed assets turnover & 7.75 & 13.22 \\ Total assets turnover & 2.60 & 3.00 \\ Profit margin on sales & 2.07% & 3.50% \\ Return on equity (ROE) & 10.45% & 21.00% \\ Payables deferral period & 30.00 & 33.00 \end{tabular} Cash Budget (Thousands of Dollars) Now Dec Jan Feb Mar Apr Sales Forecast (1) Sales (gross) $71,218.00 $68,212.00 $65,213.00 $52,475.00 $42,909.00 $30,524,00 Collections (2) During month of sale: (0.2)(0.98)(month's sales) 12,781.75 10,285.10 (3) During first month after sale(0.7)(previous month's sales) 47,748.4045,649,10 (4) During second month after sale: (0.1)(sales 2 months ago) (5) Total collections (Lines 2+3+4 ) Purchases $67,651.957,121.80$62,755.40 (6) (0.85) (forecasted sales 2 months from now) $44,603.75$36,472.65$25,945.40 Payments (7) Payments (1-month lag) (8) Wages and salaries (9) Rent (10) Taxes (11) Total payments NCFs (12) Cash on hand at start of forecast \begin{tabular}{rr} 44,603.75 & 36,472.65 \\ 6,690.56 & 5,470.90 \\ 2,500.00 & 2,500.00 \\ \hline \end{tabular} (13) NCF: Collections - Payments. = Line 5-Line 11 (14) Cum NCF: Prior + this mos. NCF Cash Surplus (or Loan Requirement) $53,794.31$44,443.55 (15) Target cash balance (16) Surplus cash or loan needed $3,000.00 $15,357.641,500.00$33,669.491,500.00 EVA=NOPATCapitalcosts=EBIT(1T)WACC(Totalcapitalemployed) \begin{tabular}{lcc} & RR & Industry \\ \hline Current & 1.75 & 2.25 \\ Quick & 0.92 & 1.16 \\ Total liabilities/assets & 58.76% & 50.00% \\ Turnover of cash and securities & 16.67 & 22.22 \\ Days sales outstanding (365-day basis) & 45.63 & 32.00 \\ Inventory turnover & 10.80 & 20.00 \\ Fixed assets turnover & 7.75 & 13.22 \\ Total assets turnover & 2.60 & 3.00 \\ Profit margin on sales & 2.07% & 3.50% \\ Return on equity (ROE) & 10.45% & 21.00% \\ Payables deferral period & 30.00 & 33.00 \end{tabular} Cash Budget (Thousands of Dollars) Now Dec Jan Feb Mar Apr Sales Forecast (1) Sales (gross) $71,218.00 $68,212.00 $65,213.00 $52,475.00 $42,909.00 $30,524,00 Collections (2) During month of sale: (0.2)(0.98)(month's sales) 12,781.75 10,285.10 (3) During first month after sale(0.7)(previous month's sales) 47,748.4045,649,10 (4) During second month after sale: (0.1)(sales 2 months ago) (5) Total collections (Lines 2+3+4 ) Purchases $67,651.957,121.80$62,755.40 (6) (0.85) (forecasted sales 2 months from now) $44,603.75$36,472.65$25,945.40 Payments (7) Payments (1-month lag) (8) Wages and salaries (9) Rent (10) Taxes (11) Total payments NCFs (12) Cash on hand at start of forecast \begin{tabular}{rr} 44,603.75 & 36,472.65 \\ 6,690.56 & 5,470.90 \\ 2,500.00 & 2,500.00 \\ \hline \end{tabular} (13) NCF: Collections - Payments. = Line 5-Line 11 (14) Cum NCF: Prior + this mos. NCF Cash Surplus (or Loan Requirement) $53,794.31$44,443.55 (15) Target cash balance (16) Surplus cash or loan needed $3,000.00 $15,357.641,500.00$33,669.491,500.00a. Johnson plans to use the preceding ratios as the starting point for discussions with RRs operating team. She wants everyone to think about the pros and cons of changing each type of current asset and how changes would interact to affect profits and EVA. Based on the data, does RR seem to be following a relaxed, moderate, or restricted working capital policy?

b. How can one distinguish between a relaxed but rational working capital policy and a situation in which a firm simply has excessive current assets because it is inefficient? Does RRs working capital policy seem appropriate?

c. Calculate the firms cash conversion cycle given that annual sales are $660,000 and cost of goods sold represents 90% of sales. Assume a 365-day year.

d. What might RR do to reduce its cash without harming operations?

e. In an attempt to better understand RRs cash position, Johnson developed a cash budget for the first 2 months of the year. She has the figures for the other months, but they are not shown. Should depreciation expense be explicitly included in the cash budget? Why or why not?

f. In her preliminary cash budget, Johnson has assumed that all sales are collected and thus that RR has no bad debts. Is this realistic? If not, how would bad debts be dealt with in a cash budgeting sense? (Hint: Bad debts will affect collections but not purchases.)

g. Johnsons cash budget for the entire year, although not given here, is based heavily on her forecast for monthly sales. Sales are expected to be extremely low between May and September but then to increase dramatically in the fall and winter. November is typically the firms best month, when RR ships its holiday blend of coffee. Johnsons forecasted cash budget indicates that the companys cash holdings will exceed the targeted cash balance every month except for October and November, when shipments will be high but collections will not be coming in until later. Based on the ratios shown earlier, does it appear that RRs target cash balance is appropriate? In addition to possibly lowering the target cash balance, what actions might RR take to better improve its cash management policies, and how might that affect its EVA?

h. What reasons might RR have for maintaining a relatively high amount of cash?

i. Is there any reason to think that RR may be holding too much inventory? If so, how would that affect EVA and ROE?

j. If the company reduces its inventory without adversely affecting sales, what effect should this have on the companys cash position (1) in the short run and (2) in the long run? Explain in terms of the cash budget and the balance sheet.

k. Johnson knows that RR sells on the same credit terms as other firms in its industry. Use the ratios presented earlier to explain whether RRs customers pay more or less promptly than those of its competitors. If there are differences, does that suggest RR should tighten or loosen its credit policy? What four variables make up a firms credit policy, and in what direction should each be changed by RR?

l. Does RR face any risks if it tightens its credit policy?

m. If the company reduces its DSO without seriously affecting sales, what effect would this have on its cash position (1) in the short run and (2) in the long run? Answer in terms of the cash budget and the balance sheet. What effect should this have on EVA in the long run?

n. In addition to improving the management of its current assets, RR is also reviewing the ways in which it finances its current assets. Is it likely that RR could make significantly greater use of accruals?

o. Assume that RR purchases $200,000 (net of discounts) of materials on terms of 1/10, net 30, but that it can get away with paying on the 40th day if it chooses not to take discounts. How much free trade credit can the company get from its equipment supplier, how much costly trade credit can it get, and what is the nominal annual interest rate of the costly credit? Should RR take discounts?

p. RR tries to match the maturity of its assets and liabilities. Describe how RR could adopt either a more aggressive or a more conservative financing policy.

q. What are the advantages and disadvantages of using short-term debt as a source of financing?

r. Would it be feasible for RR to finance with commercial paper?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options Trading For Beginners

Authors: Mike Hartley

1st Edition

979-8864514832