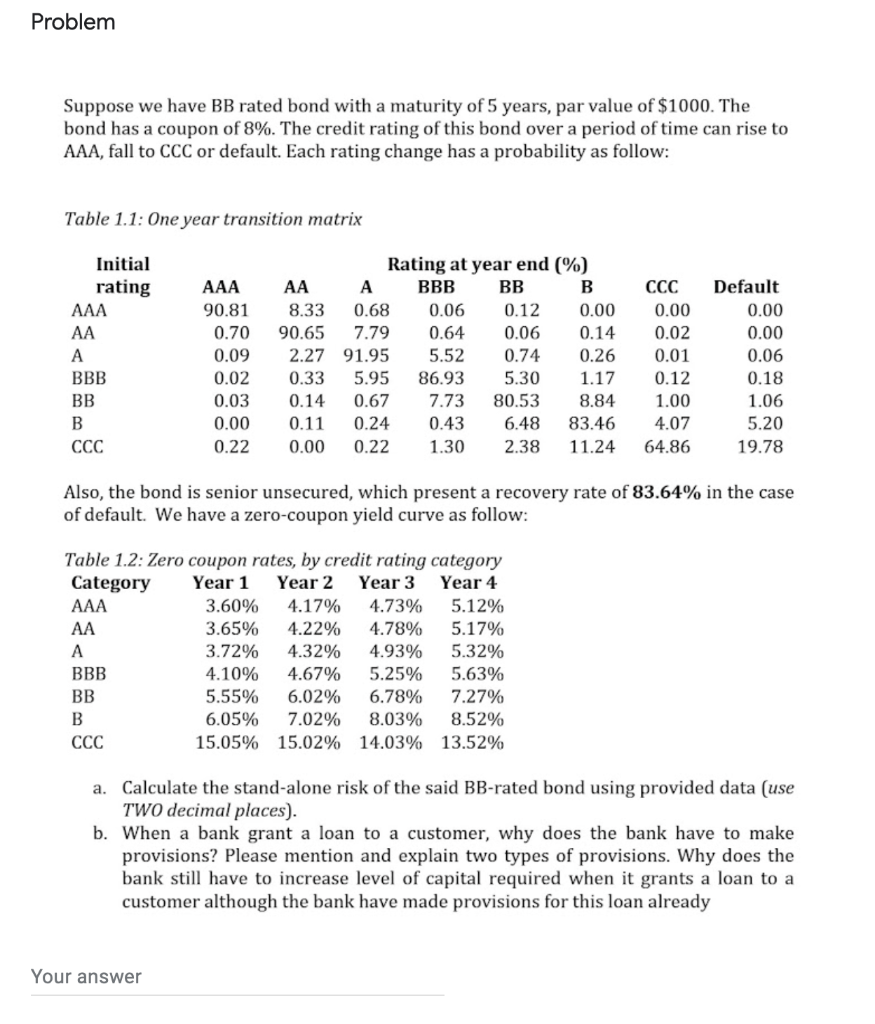

Problem Suppose we have BB rated bond with a maturity of 5 years, par value of $1000. The bond has a coupon of 8%. The credit rating of this bond over a period of time can rise to AAA, fall to CCC or default. Each rating change has a probability as follow: Table 1.1: One year transition matrix Initial rating AAA AA A BBB BB B AAA 90.81 0.70 0.09 0.02 0.03 0.00 0.22 AA 8.33 90.65 2.27 0.33 0.14 0.11 0.00 Rating at year end (%) A BBB BB B 0.68 0.06 0.12 0.00 7.79 0.64 0.06 0.14 91.95 5.52 0.74 0.26 5.95 86.93 5.30 1.17 0.67 7.73 80.53 8.84 0.24 0.43 6.48 83.46 0.22 1.30 2.38 11.24 0.00 0.02 0.01 0.12 1.00 4.07 64.86 Default 0.00 0.00 0.06 0.18 1.06 5.20 19.78 Also, the bond is senior unsecured, which present a recovery rate of 83.64% in the case of default. We have a zero-coupon yield curve as follow: Table 1.2: Zero coupon rates, by credit rating category Category Year 1 Year 2 Year 3 Year 4 AAA 3.60% 4.17% 4.73% 5.12% AA 3.65% 4.22% 4.78% 5.17% A 3.72% 4.32% 4.93% 5.32% BBB 4.10% 4.67% 5.25% 5.63% BB 5.55% 6.02% 6.78% 7.27% B 6.05% 7.02% 8.03% 8.52% 15.05% 15.02% 14.03% 13.52% a. Calculate the stand-alone risk of the said BB-rated bond using provided data (use TWO decimal places). b. When a bank grant a loan to a customer, why does the bank have to make provisions? Please mention and explain two types of provisions. Why does the bank still have to increase level of capital required when it grants a loan to a customer although the bank have made provisions for this loan already Your answer Problem Suppose we have BB rated bond with a maturity of 5 years, par value of $1000. The bond has a coupon of 8%. The credit rating of this bond over a period of time can rise to AAA, fall to CCC or default. Each rating change has a probability as follow: Table 1.1: One year transition matrix Initial rating AAA AA A BBB BB B AAA 90.81 0.70 0.09 0.02 0.03 0.00 0.22 AA 8.33 90.65 2.27 0.33 0.14 0.11 0.00 Rating at year end (%) A BBB BB B 0.68 0.06 0.12 0.00 7.79 0.64 0.06 0.14 91.95 5.52 0.74 0.26 5.95 86.93 5.30 1.17 0.67 7.73 80.53 8.84 0.24 0.43 6.48 83.46 0.22 1.30 2.38 11.24 0.00 0.02 0.01 0.12 1.00 4.07 64.86 Default 0.00 0.00 0.06 0.18 1.06 5.20 19.78 Also, the bond is senior unsecured, which present a recovery rate of 83.64% in the case of default. We have a zero-coupon yield curve as follow: Table 1.2: Zero coupon rates, by credit rating category Category Year 1 Year 2 Year 3 Year 4 AAA 3.60% 4.17% 4.73% 5.12% AA 3.65% 4.22% 4.78% 5.17% A 3.72% 4.32% 4.93% 5.32% BBB 4.10% 4.67% 5.25% 5.63% BB 5.55% 6.02% 6.78% 7.27% B 6.05% 7.02% 8.03% 8.52% 15.05% 15.02% 14.03% 13.52% a. Calculate the stand-alone risk of the said BB-rated bond using provided data (use TWO decimal places). b. When a bank grant a loan to a customer, why does the bank have to make provisions? Please mention and explain two types of provisions. Why does the bank still have to increase level of capital required when it grants a loan to a customer although the bank have made provisions for this loan already Your