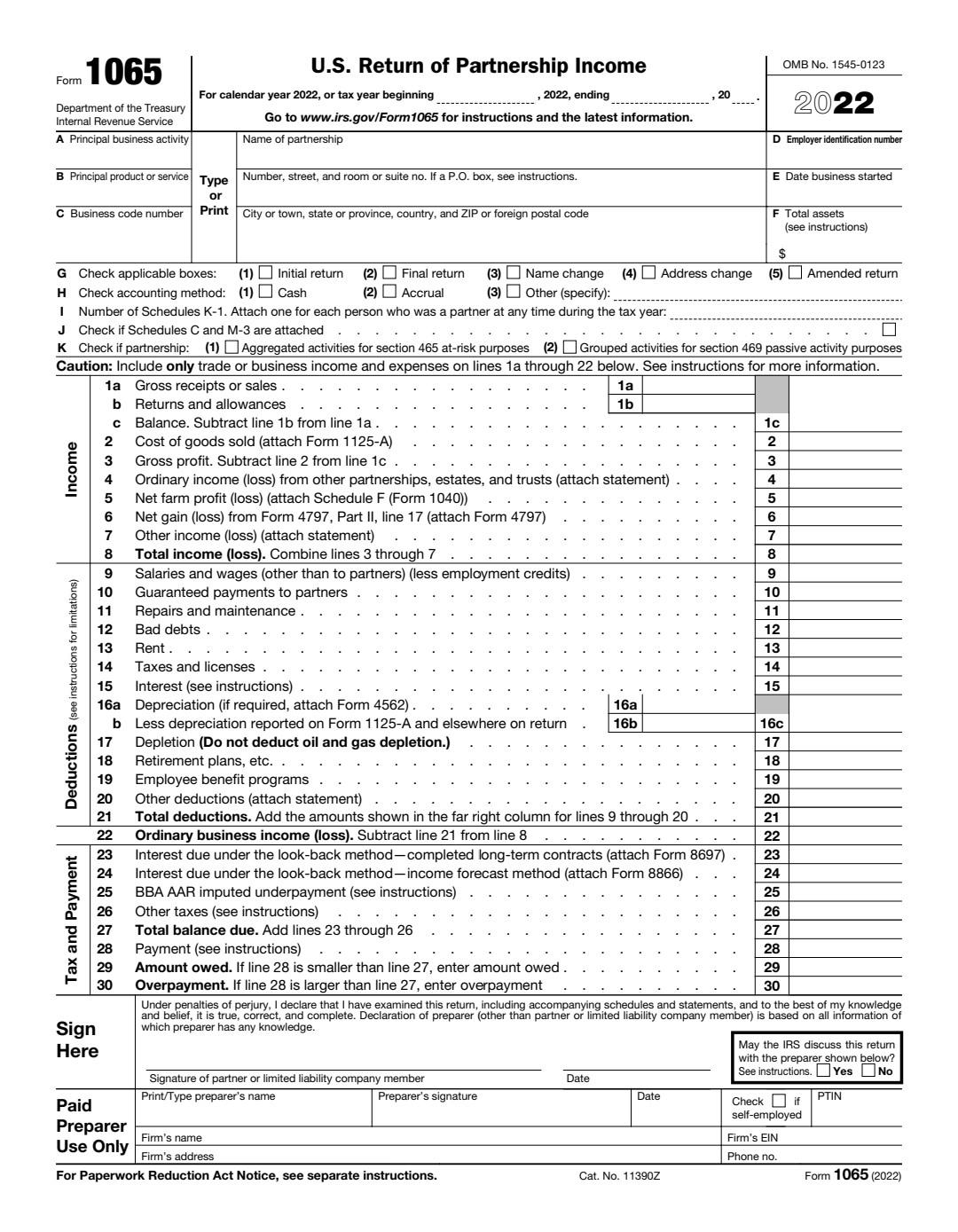

Question

Profit/Loss/Capital membership interest is 50%. Other information: AAA is a domestic limited liability company Michael and Devontae are not related. Michael and Devontae are both

Profit/Loss/Capital membership interest is 50%.

Other information:

AAA is a domestic limited liability company

Michael and Devontae are not related.

Michael and Devontae are both U.S. citizens.

Both Michael and Devontae are managing members and use the GAAP-basis to track their capital accounts

AAA has never had annual gross receipts in excess of $25,000,000.

AAA has not and did not file a Form 8893 or anything similar to it this year or in the past.

AAA is not a publicly traded partnership.

During the year, no debt was cancelled or forgiven in relation to AAA.

All of AAAs activities constitute a qualified trade or business, and the salaries and wages expense represents W-2 wages paid by AAA in 2022.

The total unadjusted basis for all assets placed in service for the prior 10 years matches the book value of all assets reported on the balance sheet.

AAA is not required to file a Form 8918.

AAA did not have or control a foreign bank account or have authority over any such financial account.

AAA was not the grantor of or a transferor to a foreign trust.

AAA has never made a Section 754 election.

AAA has never entered a like-kind exchange or distributed a tenancy-in-common or other undivided interest in partnership property.

AAA has never been required to file Form 8858.

AAA was required to file Form(s) 1099 related to certain payments it made during the year and those forms were filed on a timely basis.

AAA was not required to file any Form(s) 5471 during the year.

Michael is the Partnership Representative.

Both Michael and Devontae are active in the business and work full-time for AAA.

The debt owed to First National Bank is a non-recourse obligation and neither Michael nor Devontae have guaranteed its repayment (see balance sheet below). This debt is not directly tied to any specific asset but is rather a debt secured against all of the assets of the company.

During the year, Michael and Devontae each contributed $20,000 to the capital of AAA

AAA does not maintain any inventory. AAA purchases supplies and has a policy of expensing such purchases as paid for tax and book purposes consistent with existing tax law.

AAA uses MACRS depreciation for both tax and book purposes.

During the year, Michael and Devontae each received a $75,000 distribution from AAA.

During the year, AAA acquired the following assets (all assets were placed in service on the acquisition dates as indicated below):

o Service vans-new (not Luxury Automobiles) July 1, 2022 $500,000

o Plumbing machinery/equipment-new July 1, 2022 $250,000

AAA did not claim Section 179 expense for any of the current year asset additions and has opted out of bonus depreciation for 3 and 5- year recovery period assets.

Financial Statements:

Balance Sheet

Assets: 12/31/21 12/31/22

Cash $ 30,000 $ 45,000

Tax-exempt Securities 100,000 100,000

Building 4,000,000 4,000,000

Less: Acc. Depreciation (551,282) (653,842)

Equipment 2,500,000 3,250,000

Less: Acc. Depreciation (1,481,400) (2,138,800

Land 1,000,000 1,000,000

Total Assets: $5,597,318 $5,602,358

Liabilities and Capital:

Note Payable-First National Bank $4,267,318 $4,046,673

Note Payable-Michael Rodriguez 300,000 300,000

Note Payable-Devontae Johnson 200,000 200,000

Capital Account-MR 415,000 527,842.50

Capital Account-DJ 415,000 527,842.50

Total Liabilities and Capital: $5,597,318 $5,602,358

Income Statement for the year ending December 31, 2022

Item Amount

Income:

Service Revenue-Cash $ 343,570

Service Revenue-Credit Cards $1,922,710

Consulting Revenue-Cash $ 50,950

Consulting Revenue-Credit Cards $ 155,005

Interest Income-First National Bank $ 1,540

Municipal Bond Interest Income $ 2,500

Total Income: $2,476,275

Expenses:

Employee Salaries $ 515,735

Guaranteed payment-MR $ 50,000

Guaranteed payment-DJ $ 50,000

Repairs and Maintenance-Trucks $ 113,415

Rent $ 35,000

Payroll Taxes $ 41,260

Licensing Fees $ 1,750

Property Taxes $ 77,000

Interest Expense $ 235,000

Depreciation $ 759,960

Office Supplies $ 3,420

Employee Training $ 5,675

Advertising $ 18,850

Plumbing supplies $ 15,125

Meals (prior to disallowance) $ 13,740

Travel $ 4,210

Gasoline $ 158,675

Utilities $ 24,940

Telephone $ 16,830

Total Expenses: $2,140,585

Net Income: $ 335,690

For Paperwork Reduction Act Notice, see separate instructions. b Own directly an interest of 20% or more, or own, directly or indirectly, an interest of 50% or more in the profit, loss, or capital in any foreign or domestic partnership (including an entity treated as a partnership) or in the beneficial interest of a trust? For rules of constructive ownership, see instructions. If "Yes," complete (i) through (v) below . Form 1065 (2022) Page 4 Form 1065 (2022) Form 1065 (2022) Page 5 Analysis of Net Income (Loss) per Return 1 Net income (loss). Combine Schedule K, lines 1 through 11. From the result, subtract the sum of Schedule K, lines 12 through 13d, and 21 2 Analysis by partner type: a General partners b Limited partners \begin{tabular}{|c|c|c|c|c|c} \hline (i) Corporate & (ii)Individual(active) & (iii)Individual(passive) & (iv) Partnership & (v)ExemptOrganization & (vi)Nominee/Other \\ \hline & & & & & \\ \hline & & & & & \\ \hline \end{tabular} Assets \begin{tabular}{|l|} \hline Be \\ \hline \end{tabular} 1 Cash 2a Trade notes and accounts receivable. b Less allowance for bad debts 3 Inventories 4 U.S. Government obligations 5 Tax-exempt securities 6 Other current assets (attach statement) . 7a Loans to partners (or persons related to partners) b Mortgage and real estate loans 8 Other investments (attach statement). 9a Buildings and other depreciable assets b Less accumulated depreciation 10a Depletable assets b Less accumulated depletion 11 Land (net of any amortization) 12a Intangible assets (amortizable only) b Less accumulated amortization 13 Other assets (attach statement) 14 Total assets Liabilities and Capital 15 Accounts payable 16 Mortgages, notes, bonds payable in less than 1 year 17 Other current liabilities (attach statement) 18 All nonrecourse loans . 19a Loans from partners (or persons related to partners) . b Mortgages, notes, bonds payable in 1 year or more 20 Other liabilities (attach statement) . 21 Partners' capital accounts 22 Total liabilities and capital Schedule M-1 Reconciliation of Income (Loss) per Books With Analysis of Net Income (Loss) per Return Note: The partnership may be required to file Schedule M-3. See instructions. For Paperwork Reduction Act Notice, see separate instructions. b Own directly an interest of 20% or more, or own, directly or indirectly, an interest of 50% or more in the profit, loss, or capital in any foreign or domestic partnership (including an entity treated as a partnership) or in the beneficial interest of a trust? For rules of constructive ownership, see instructions. If "Yes," complete (i) through (v) below . Form 1065 (2022) Page 4 Form 1065 (2022) Form 1065 (2022) Page 5 Analysis of Net Income (Loss) per Return 1 Net income (loss). Combine Schedule K, lines 1 through 11. From the result, subtract the sum of Schedule K, lines 12 through 13d, and 21 2 Analysis by partner type: a General partners b Limited partners \begin{tabular}{|c|c|c|c|c|c} \hline (i) Corporate & (ii)Individual(active) & (iii)Individual(passive) & (iv) Partnership & (v)ExemptOrganization & (vi)Nominee/Other \\ \hline & & & & & \\ \hline & & & & & \\ \hline \end{tabular} Assets \begin{tabular}{|l|} \hline Be \\ \hline \end{tabular} 1 Cash 2a Trade notes and accounts receivable. b Less allowance for bad debts 3 Inventories 4 U.S. Government obligations 5 Tax-exempt securities 6 Other current assets (attach statement) . 7a Loans to partners (or persons related to partners) b Mortgage and real estate loans 8 Other investments (attach statement). 9a Buildings and other depreciable assets b Less accumulated depreciation 10a Depletable assets b Less accumulated depletion 11 Land (net of any amortization) 12a Intangible assets (amortizable only) b Less accumulated amortization 13 Other assets (attach statement) 14 Total assets Liabilities and Capital 15 Accounts payable 16 Mortgages, notes, bonds payable in less than 1 year 17 Other current liabilities (attach statement) 18 All nonrecourse loans . 19a Loans from partners (or persons related to partners) . b Mortgages, notes, bonds payable in 1 year or more 20 Other liabilities (attach statement) . 21 Partners' capital accounts 22 Total liabilities and capital Schedule M-1 Reconciliation of Income (Loss) per Books With Analysis of Net Income (Loss) per Return Note: The partnership may be required to file Schedule M-3. See instructionsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Environmental And Safety Auditing Program Strategies For Legal International And Financial Issues

Authors: Unhee Kim, John F. Falkenbury, Timothy A. Wilkins, Ralph Rhodes, Richard J. Satterfield

1st Edition

1566702461, 978-1566702461