Question

Prudential Bank has the following balance sheet (in millions) with the risk weights in parentheses. In addition, the bank has $30 million in performance-related standby

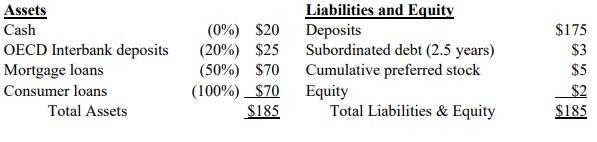

Prudential Bank has the following balance sheet (in millions) with the risk weights in parentheses.

In addition, the bank has $30 million in performance-related standby letters of credit (SLCs), $40 million in two-year forward FX contracts that are currently in the money by $1 million, and $300 million in six-year interest rate swaps that are currently out of the money by $2 million. Credit conversion factors follow:

Performance-related standby LCs 50%

1-5 year foreign exchange contracts 5%

1-5 year interest rate swaps 0.5%

5-10 year interest rate swaps 1.5%

And overall risk weight of 50%

questions:

a) What are the risk-adjusted on-balance-sheet assets of the bank as defined under the Basle Accord?

b) What is the total capital required for both off- and on-balance-sheet assets?

c) Does the bank have enough capital to meet the Basle requirements? If not, what minimum Tier 1 or total capital does it need to meet the requirement?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Legal Handbook For Financial Planning In 2019

Authors: Allen Buckley

1st Edition

1091578826, 978-1091578821