Answered step by step

Verified Expert Solution

Question

1 Approved Answer

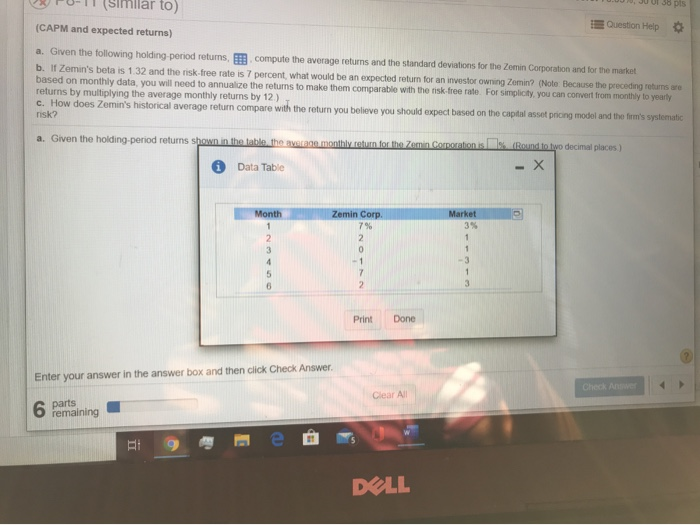

PU-I (Simllar to) TUU JUUL 38 pls (CAPM and expected returns) Question Help a. Given the following holding period retums, compute the average returns and

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Role Of Modern Accounting Practices In Businesses Financial Stability And Sustainable Development During Digital Era And Artificial Intelligence Applications

Authors: Ibrahim Mert

1st Edition

3631894252, 3631894333, 9783631894255, 9783631894330