Answered step by step

Verified Expert Solution

Question

1 Approved Answer

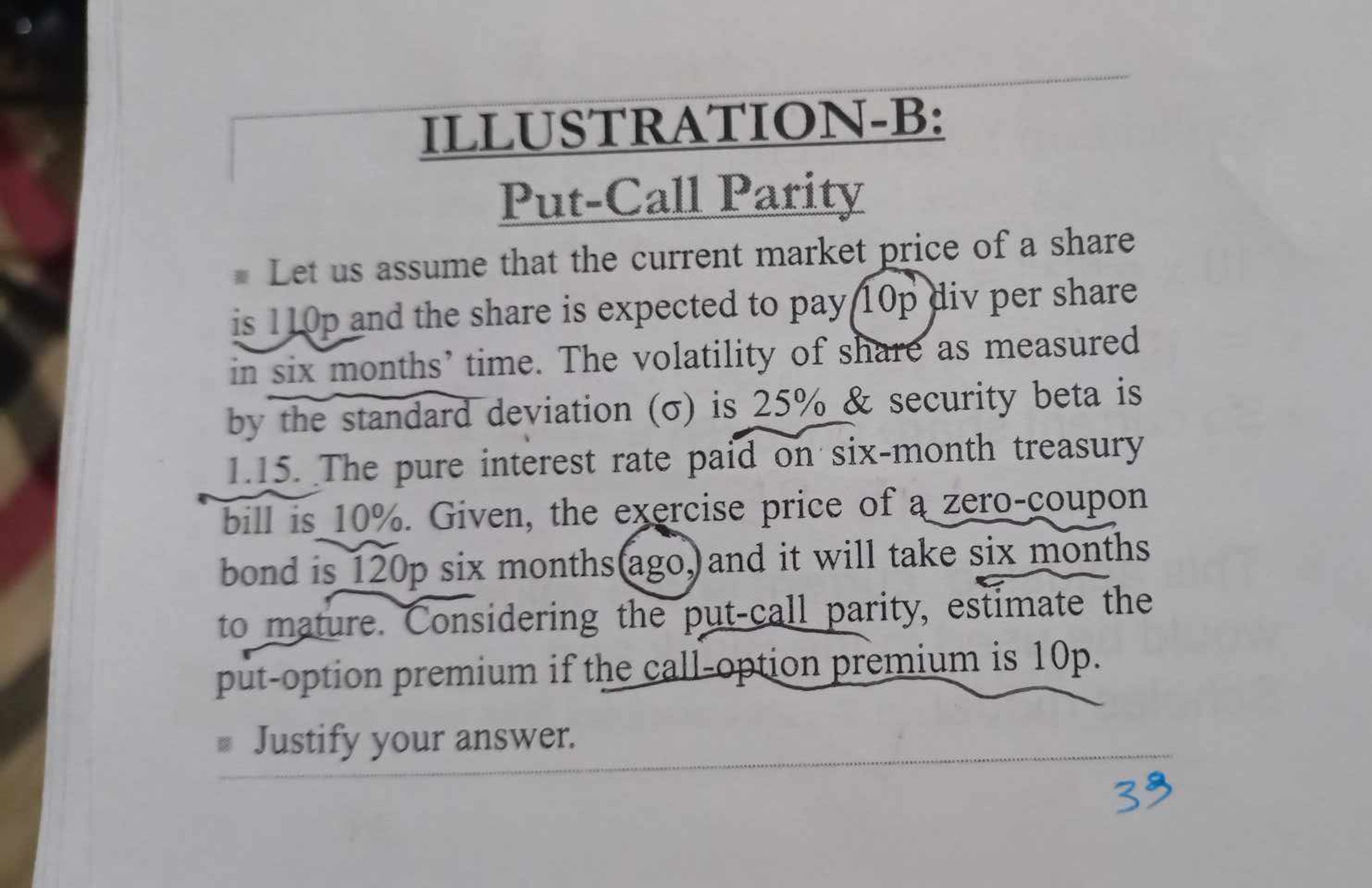

Put - Call Parity = Let us assume that the current market price of a share is 1 1 0 p and the share is

PutCall Parity

Let us assume that the current market price of a share

is and the share is expected to pay div per share

in six months' time. The volatility of share as measured

by the standard deviation is & security beta is

The pure interest rate paid on sixmonth treasury

bill is Given, the exercise price of a zerocoupon

bond is p six months ago. and it will take six months

to mature. Considering the putcall parity, estimate the

putoption premium if the calloption premium is

Justify your answer.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Energy And Finance Sustainability In The Energy Industry

Authors: André Dorsman, Özgür Arslan-Ayaydin, Mehmet Baha Karan

1st Edition

3319322664, 978-3319322667