Answered step by step

Verified Expert Solution

Question

1 Approved Answer

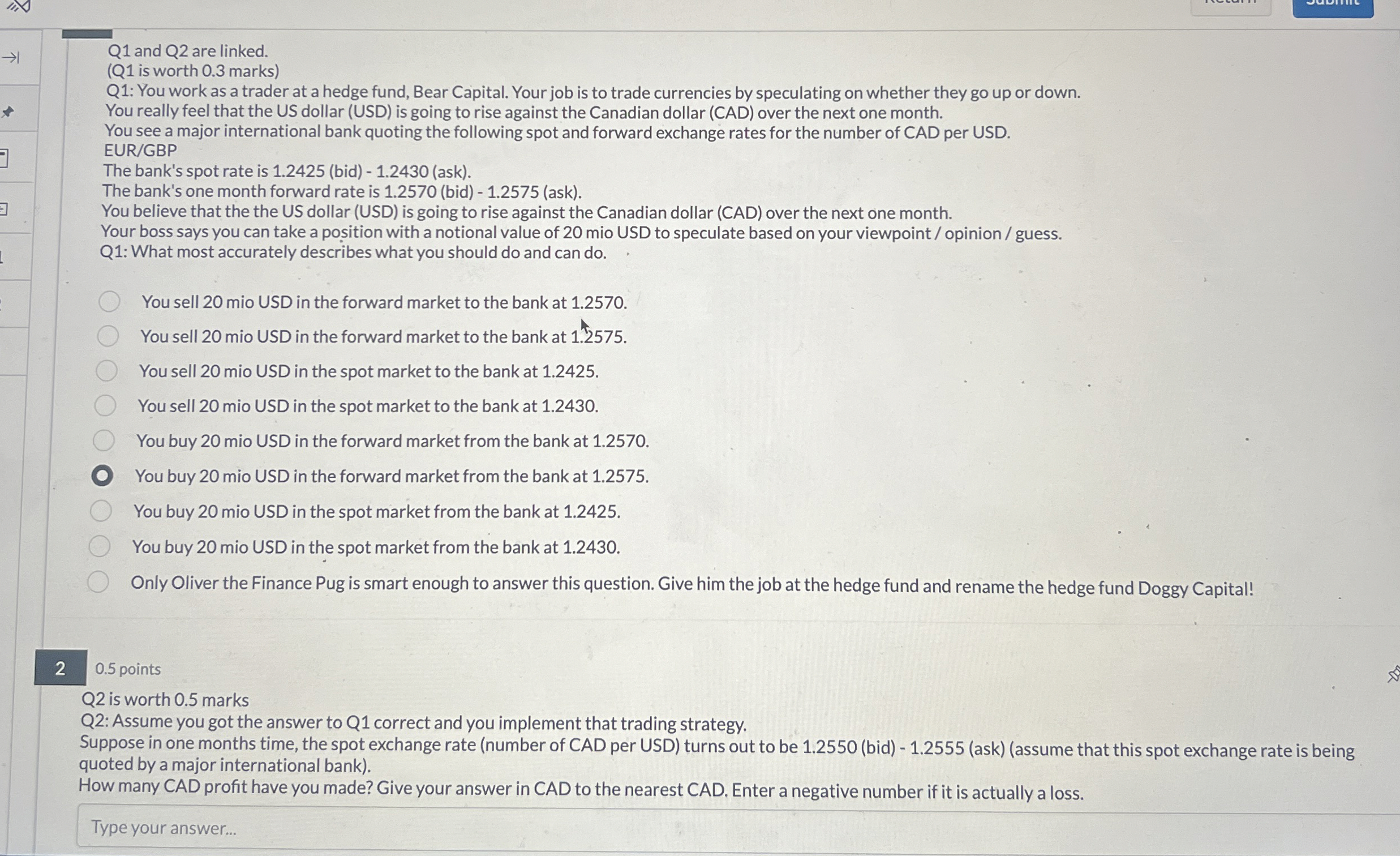

Q 1 and Q 2 are linked. ANSWER QUESTION 2 please ( Q 1 is worth 0 . 3 marks ) Q 1 : You

Q and Q are linked. ANSWER QUESTION please

Q is worth marks

Q: You work as a trader at a hedge fund, Bear Capital. Your job is to trade currencies by speculating on whether they go up or down.

You really feel that the US dollar USD is going to rise against the Canadian dollar CAD over the next one month.

You see a major international bank quoting the following spot and forward exchange rates for the number of CAD per USD.

EURGBP

The bank's spot rate is bidask

The bank's one month forward rate is bidask

You believe that the the US dollar USD is going to rise against the Canadian dollar CAD over the next one month.

Your boss says you can take a position with a notional value of mio USD to speculate based on your viewpoint opinion guess.

Q: What most accurately describes what you should do and can do

You sell mio USD in the forward market to the bank at

You sell mio USD in the forward market to the bank at

You sell mio USD in the spot market to the bank at

You sell mio USD in the spot market to the bank at

You buy mio USD in the forward market from the bank at

You buy mio USD in the forward market from the bank at

You buy mio USD in the spot market from the bank at

You buy mio USD in the spot market from the bank at

Only Oliver the Finance Pug is smart enough to answer this question. Give him the job at the hedge fund and rename the hedge fund Doggy Capital!

Q is worth marks

Q: Assume you got the answer to Q correct and you implement that trading strategy.

Suppose in one months time, the spot exchange rate number of CAD per USD turns out to be bidaskassume that this spot exchange rate is being

quoted by a major international bank

How many CAD profit have you made? Give your answer in CAD to the nearest CAD. Enter a negative number if it is actually a loss.

Type your answer...

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial management theory and practice

Authors: Eugene F. Brigham and Michael C. Ehrhardt

12th Edition

978-0030243998, 30243998, 324422695, 978-0324422696