Answered step by step

Verified Expert Solution

Question

1 Approved Answer

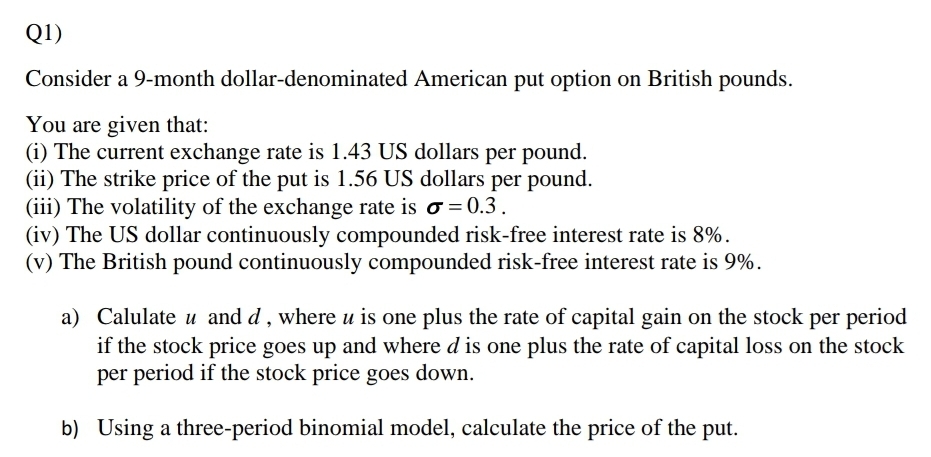

Q 1 ) Consider a 9 - month dollar - denominated American put option on British pounds. You are given that: ( i ) The

Q

Consider a month dollardenominated American put option on British pounds.

You are given that:

i The current exchange rate is US dollars per pound.

ii The strike price of the put is US dollars per pound.

iii The volatility of the exchange rate is

iv The US dollar continuously compounded riskfree interest rate is

v The British pound continuously compounded riskfree interest rate is

a Calulate and where is one plus the rate of capital gain on the stock per period if the stock price goes up and where is one plus the rate of capital loss on the stock per period if the stock price goes down.

b Using a threeperiod binomial model, calculate the price of the put.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of managerial finance

Authors: Lawrence J Gitman, Chad J Zutter

12th edition

9780321524133, 132479540, 321524136, 978-0132479547