Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Q 2 . Underlying priced at 5 0 0 with MAD of 1 0 0 . ( 1 5 points ) Q 2 a .

Q Underlying priced at with MAD of points

Qa What is the probability of option expiring ITM for a CALL? points

Qb What is the average underlying price when CALL expires ITM? points

Qc What is the average CALL option payment conditional on that the call expires in the money?

pointsnot this is asking for OPTION payment NOT average stock price when option expires ITM

Qd How much should the CALL be priced at today based on Qa and Qc points

Qe Out of the price in Qd how much of that is intrinsic value and how much is time value?

points Q Implied MAD with Uniform Distribution

Underlying price currently at and follows a uniform distribution. You observed strike

CALL priced at $ What is the implied MAD? points Q Delta and Gamma with Uniform Distribution points

Current underlying price at and you expect price at expiration follows uniform distribution

with mean absolute deviation of

You SHORT CALLs with strike at

Qa What is the TOTAL delta of your short CALL position? points

Qb How many shares do you need in order to offset CALL delta from Qa Do you long or short

the underlying shares points

Qc What is the total gamma value of your hedged SHORT CALL positions from Qa and Qb

points

Qd For the hedged CALL position short CALLs, hedged with shares what is the PnL from

starting delta, and from gamma when underlying moves from to respectively? pointsQe Calculate option price when stock moves $ How much of the total PnL of Qd is from

option position, and how much is from the stock position? points

Qf If underlying moves down from to what is the new delta at stock price of for your

overall position? If you need to rehedge to flatten delta with underlying shares, what trade do you

need to do in the shares to flatten the delta? How many shares to trade? Long or short? points

Qg What is the PnL from the delta and gamma when underlying moves from to

respectively? points

Qh For Qg how much of the total PnL is from option position, and how much is from stock

positions, when underlying moves from to points

Qi If underlying moves up from to If you need to rehedge to flatten delta with

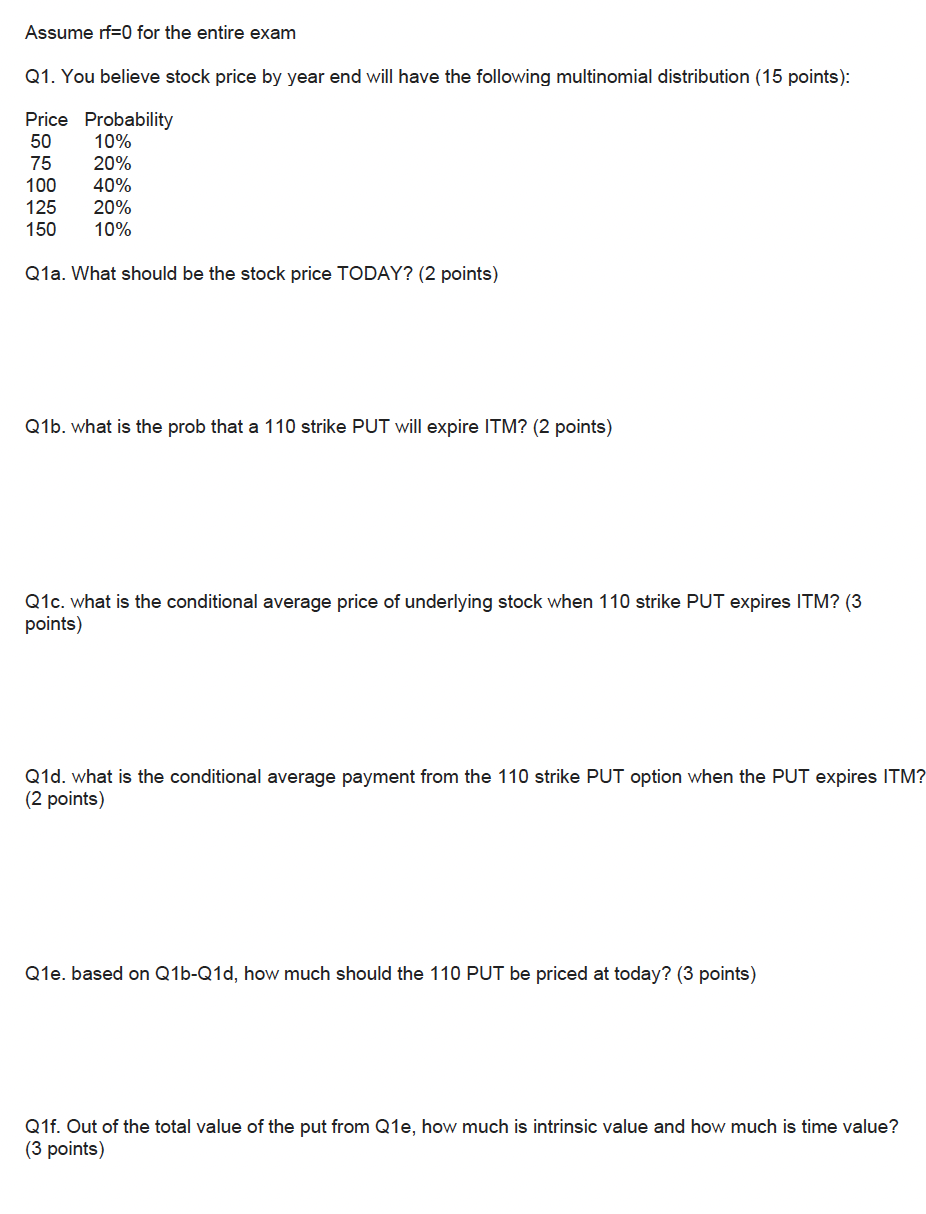

underlying shares, what trade do you need to do in the shares? pointsAssume for the entire exam

Q You believe stock price by year end will have the following multinomial distribution points:

Qa What should be the stock price TODAY? points

Qb what is the prob that a strike PUT will expire ITM? points

Qc what is the conditional average price of underlying stock when strike PUT expires ITM?

points

Qd what is the conditional average payment from the strike PUT option when the PUT expires ITM?

points

Qe based on QbQd how much should the PUT be priced at today? points

Qf Out of the total value of the put from Qe how much is intrinsic value and how much is time value?

points

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments An Introduction

Authors: Herbert B Mayo

9th Edition

324561385, 978-0324561388