Answered step by step

Verified Expert Solution

Question

1 Approved Answer

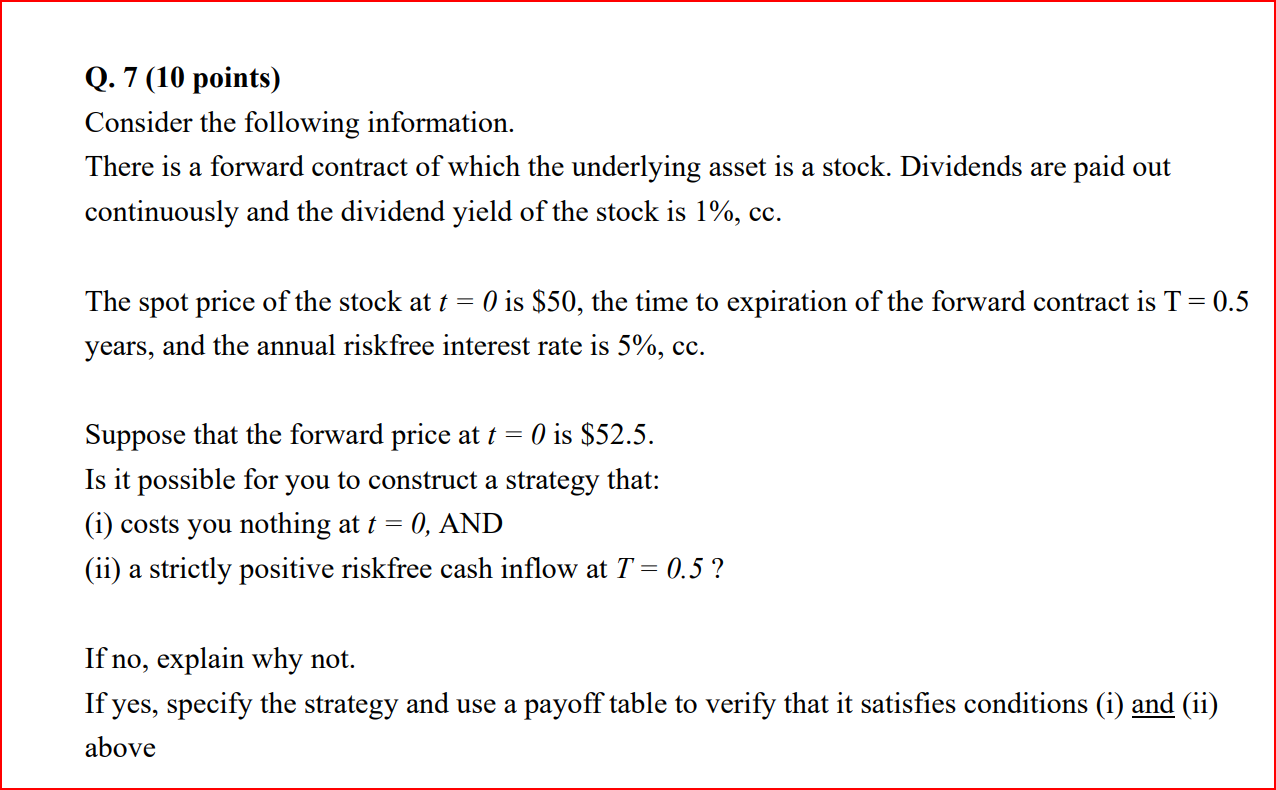

Q. 7 (10 points) Consider the following information. There is a forward contract of which the underlying asset is a stock. Dividends are paid out

Q. 7 (10 points) Consider the following information. There is a forward contract of which the underlying asset is a stock. Dividends are paid out continuously and the dividend yield of the stock is 1%, cc. The spot price of the stock at t=0 is $50, the time to expiration of the forward contract is T=0.5 years, and the annual riskfree interest rate is 5%, cc. Suppose that the forward price at t=0 is $52.5. Is it possible for you to construct a strategy that: (i) costs you nothing at t=0, AND (ii) a strictly positive riskfree cash inflow at T=0.5 ? If no, explain why not. If yes, specify the strategy and use a payoff table to verify that it satisfies conditions (i) and (ii) above

Q. 7 (10 points) Consider the following information. There is a forward contract of which the underlying asset is a stock. Dividends are paid out continuously and the dividend yield of the stock is 1%, cc. The spot price of the stock at t=0 is $50, the time to expiration of the forward contract is T=0.5 years, and the annual riskfree interest rate is 5%, cc. Suppose that the forward price at t=0 is $52.5. Is it possible for you to construct a strategy that: (i) costs you nothing at t=0, AND (ii) a strictly positive riskfree cash inflow at T=0.5 ? If no, explain why not. If yes, specify the strategy and use a payoff table to verify that it satisfies conditions (i) and (ii) above Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Meaningful Money Handbook

Authors: Pete Matthew

1st Edition

0857196510, 978-0857196514