Question: Q. Explain the factors behind GE's decline in financial performance from 2016 to 2018. * Case 20 can be found in the below book: Contemporary

Q. Explain the factors behind GE's decline in financial performance from 2016 to 2018.

* Case 20 can be found in the below book:

Contemporary Strategy Analysis 10th edition - for Robert M. Grant

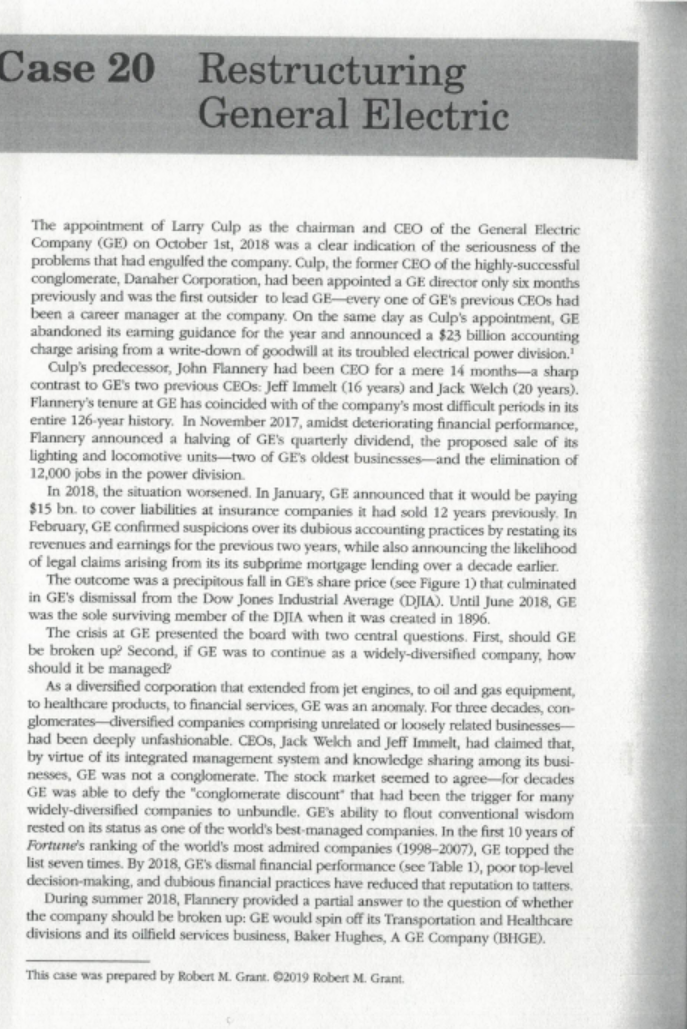

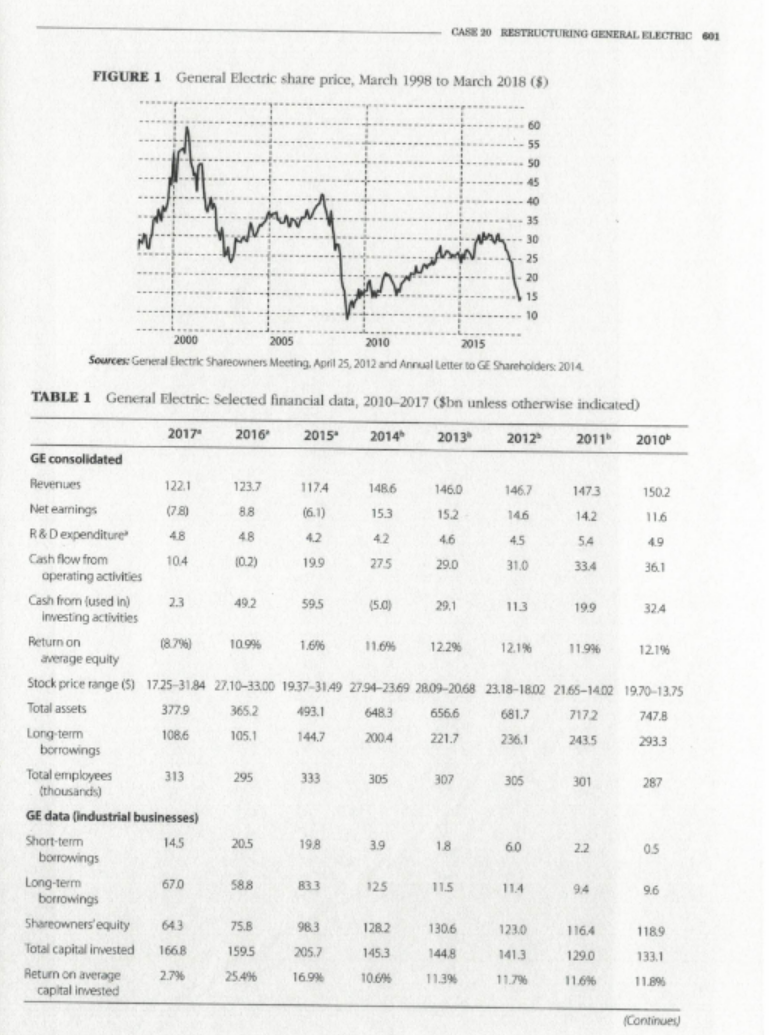

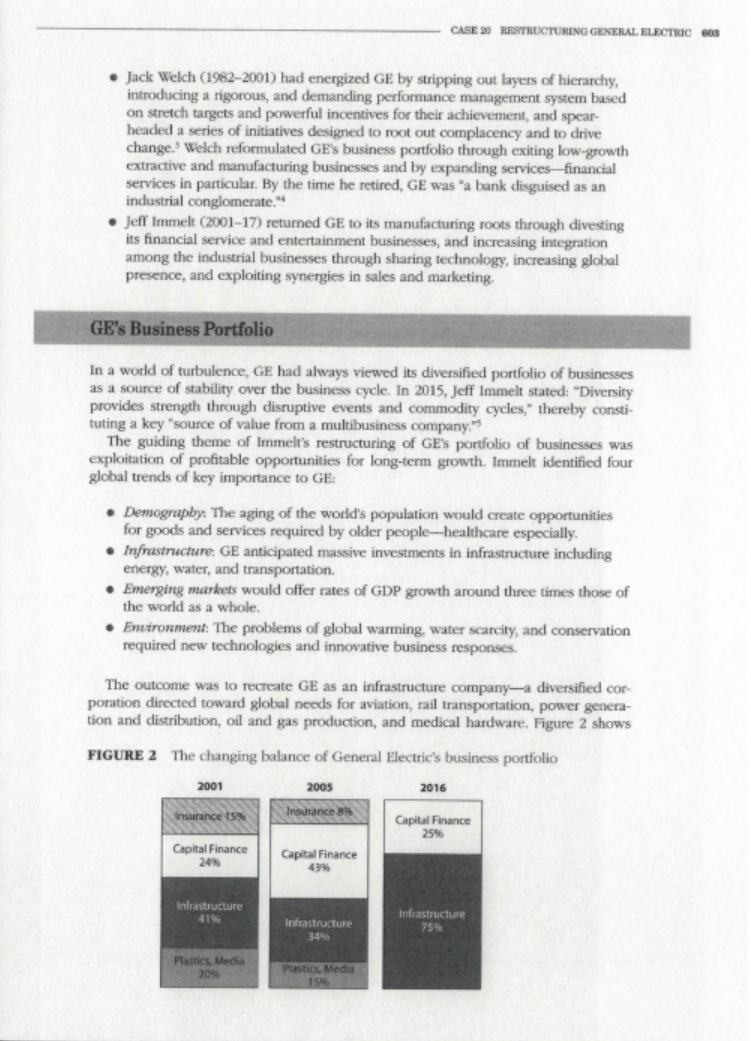

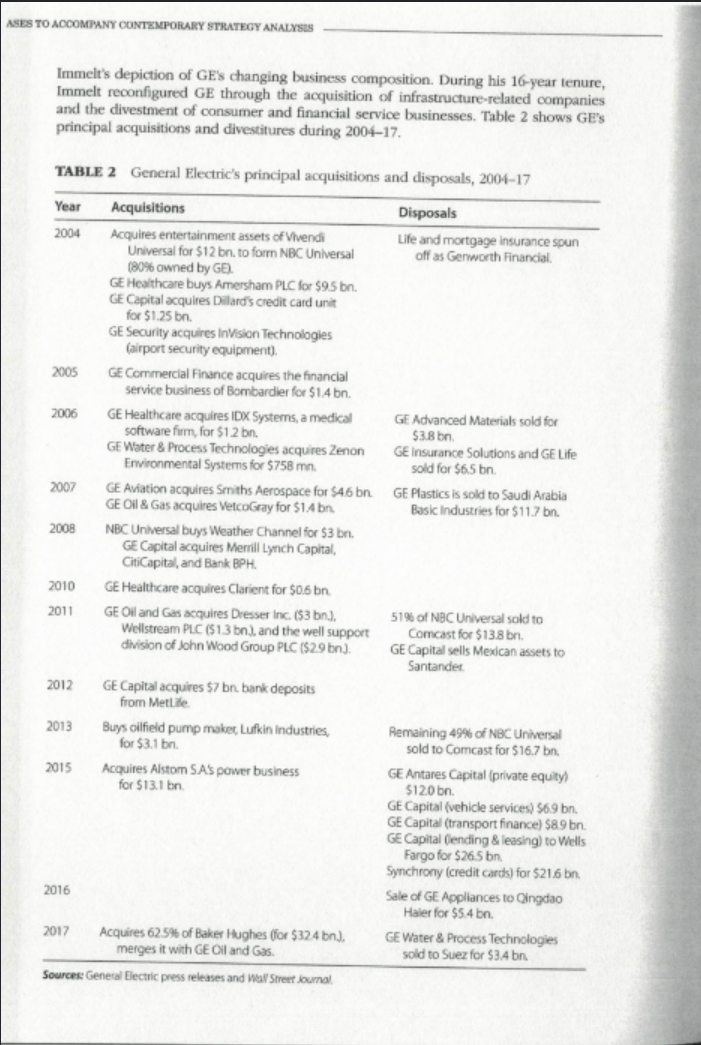

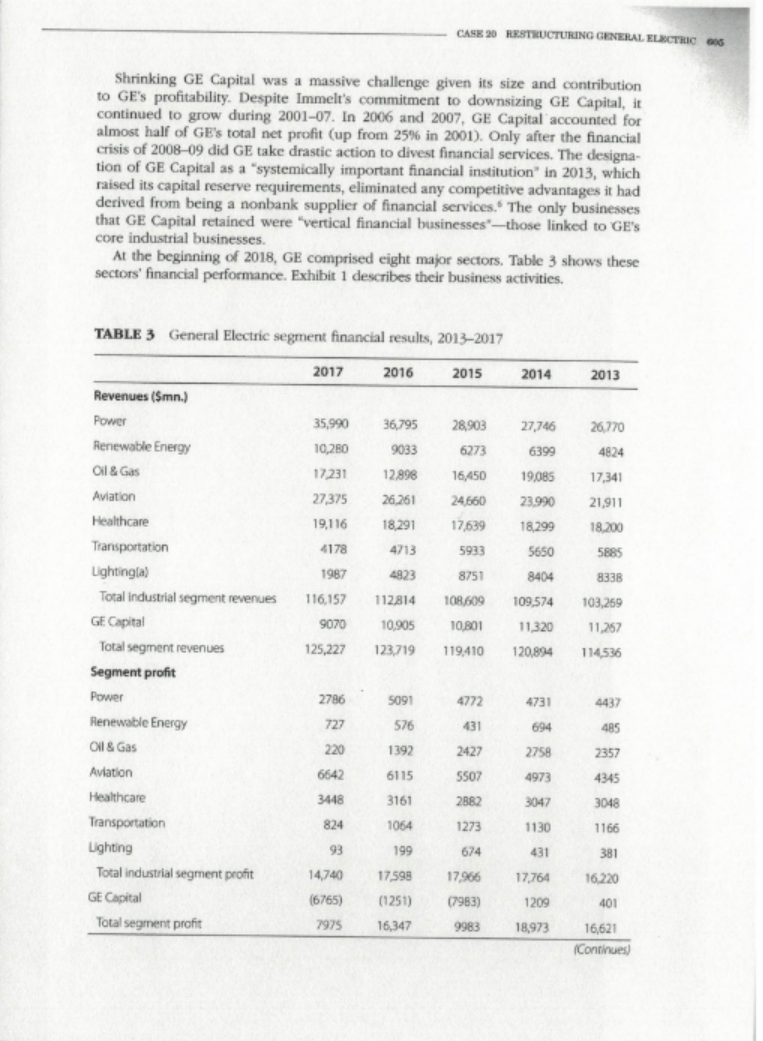

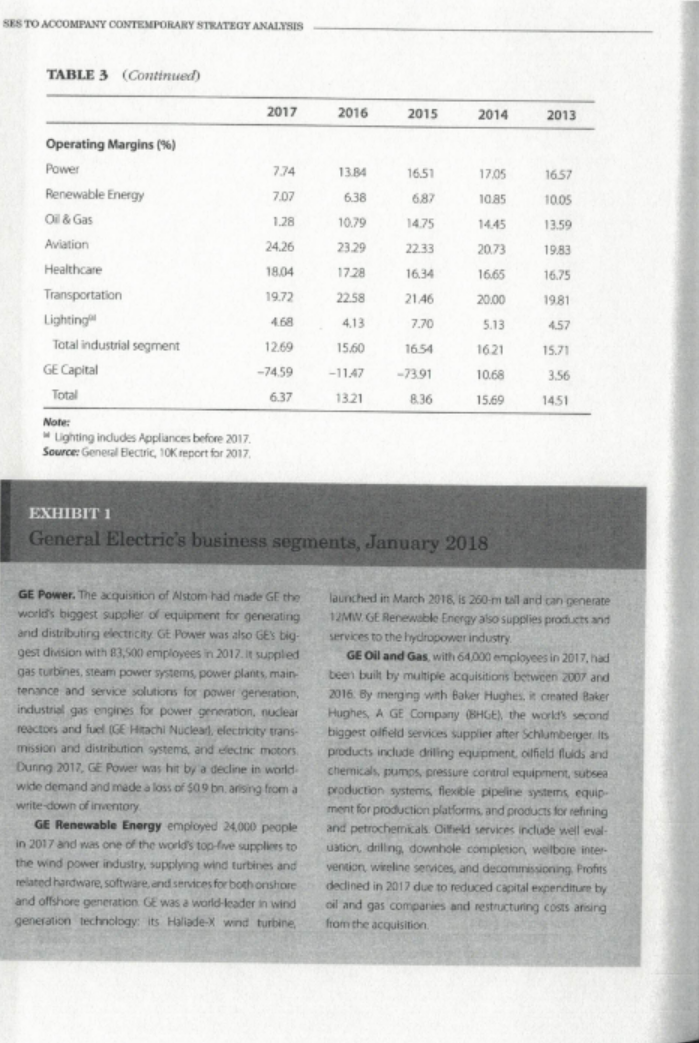

Case 20 Restructuring General Electric The appointment of Larry Culp as the chairman and CEO of the General Electric Company (GE) on October 1st, 2018 was a clear indication of the seriousness of the problems that had engulfed the company. Culp, the former CEO of the highly successful conglomerate, Danaher Corporation, had been appointed a GE director only six months previously and was the first outsider to lead Ge-every one of GE's previous CEOs had been a career manager at the company. On the same day as Culp's appointment, GE abandoned its earning guidance for the year and announced a $23 billion accounting charge arising from a write-down of goodwill at its troubled electrical power division.' Culp's predecessor, John Flannery had been CEO for a mere 14 months-a sharp contrast to GE's two previous CEOs: Jeff Immelt (16 years) and Jack Welch (20 years). Flannery's tenure at GE has coincided with of the company's most difficult periods in its entire 126-year history. In November 2017, amidst deteriorating financial performance, Flannery announced a halving of GE's quarterly dividend, the proposed sale of its lighting and locomotive units--two of GE's oldest businesses and the elimination of 12,000 jobs in the power division In 2018, the situation worsened. In January, GE announced that it would be paying $15 bn to cover liabilities at insurance companies it had sold 12 years previously. In February, GE confirmed suspicions over its dubious accounting practices by restating its revenues and earnings for the previous two years, while also announcing the likelihood of legal claims arising from its its subprime mortgage lending over a decade earlier. The outcome was a precipitous fall in GE's share price (see Figure 1) that culminated in GE's dismissal from the Dow Jones Industrial Average (DJIA). Until June 2018, GE was the sole surviving member of the DJIA when it was created in 1896. The crisis at GE presented the board with two central questions. First, should GE be broken up? Second, if GE was to continue as a widely-diversified company, how should it be managed? As a diversified corporation that extended from jet engines, to oil and gas equipment, to healthcare products, to financial services, GE was an anomaly. For three decades, con glomerates-diversified companies comprising unrelated or loosely related businesses had been deeply unfashionable. CEOs, Jack Welch and Jeff Immelt, had claimed that, by virtue of its integrated management system and knowledge sharing among its busi- nesses, GE was not a conglomerate. The stock market seemed to agree--for decades GE was able to defy the "conglomerate discount that had been the trigger for many widely-diversified companies to unbundle. GE's ability to flout conventional wisdom rested on its status as one of the world's best-managed companies. In the first 10 years of Fortune's ranking of the wodd's most admired companies (1998-2007), GE topped the list seven times. By 2018, GE's dismal financial performance (see Table 1), poor top-level decision-making, and dubious financial practices have reduced that reputation to tatters. During summer 2018, Flannery provided a partial answer to the question of whether the company should be broken up: GE would spin off its Transportation and Healthcare divisions and its oilfield services business, Baker Hughes, A GE Company (BHGE). This case was prepared by Robert M. Grant 2019 Robert M. Grant CASE 20 RESTRUCTURING GENERAL ELECTRIC 601 FIGURE 1 General Electric share price, March 1998 to March 2018 (5) 60 55 50 45 40 35 30 25 henta 20 15 10 2000 2005 2010 2015 Sources: General Electrk Shareowners Meeting, April 25, 2012 and Annual letter to GE Shareholders 2014 TABLE 1 General Electric: Selected financial data, 2010-2017 (Sbn unless otherwise indicated) Net earnings 2017 2016 2015 2014 2013 2012 2011 2010 GE consolidated Revenues 122.1 123.7 1174 148.6 146.0 1467 1473 1502 (7.80 8.8 (6.1) 153 15.2 146 142 116 R&D expenditure 48 48 42 42 4.6 4.5 54 49 Cash flow from 104 10.2) 199 275 29.0 31.0 33.4 361 operating activities Cash from (used in) 2.3 492 59.5 (5.0) 29.1 113 19.9 324 investing activities Return on (8.7%) 10.99 1.67% 11.6% 12.296 12.1% 11.996 12.196 average equity Stock price range (5) 17.25-3184 27.10-33.00 1937-3149 27.94-2369 28.09-2068 23.18-18.02 2165-1402 1970-13.75 Total assets 3779 3652 493.1 648.3 656.6 681.7 7172 7478 Long term 1086 105.1 144.7 200.4 221.7 236,1 2435 2933 borrowings Total employees 313 295 333 305 307 305 301 287 (thousands) GE data (Industrial businesses) 145 20.5 19,8 39 18 60 22 0.5 670 588 833 125 11.5 11.4 94 9.6 Short-term borrowings Long-term borrowings Shareowners' equity Total capital invested Return on average capital invested 643 75.8 983 1282 1306 123.0 116.4 1189 1668 159.5 145.3 144.8 141.3 129.0 133.1 205.7 16.9% 2.796 25.4% 10.6% 11.39 11.796 11.6% 11.89 Continues FASES TO ACCOMPANY CONTEMPORARY STRATEGY ANALYSIS TABLE 1 (Continued) 2017 2016 2015 2014 2013 2012 2011 2010 49.796 50.1% 11.296 9.2% 12.49 90% 7.696 10.9 427 44.1 45.4 49.1 499 10.8 (158) (22) 72 62 62 165 22 Borrowings as % of 489% capital invested SE capital data (financial services) Revenues 9.1 wet earnings (7.1) Shareowner's equity 135 otal borrowings 952 Ratio of debt to 7,061 equity Cotal assets 156.7 247 46.2 875 82.7 81.9 77.1 69,0 1173 1802 3495 371.1 443.1 4705 3970 485:18 4.75:1 3.90:1 3.99.1 4.49:1 5.75:1 6.821 1830 3160 5002 5168 539.4 5845 6053 Notes: As reported in 2017 financial statements As reported in 2014 financial statements Although Culp had endorsed this restructuring of GE's business portfolio, the board's decision to fire Flannery and appoint him CEO was a clear indication that these mea- sures were not enough. Culp would need to answer the fundamental questions relating to the identity and strategic rationale of GE. If GE really did add value to its constituent businesses, why divest these major divisions? If the synergies among GE's businesses really were illusory, then why not break up GE entirely The History of GE GE was created in 1892 from the merger of Thomas Edison's Electric Light Company with the Thomas Houston Company. Its business was based upon exploiting Edison's patents relating to electricity generation and distribution, light bulbs, and electric motors. Throughout the 20th century, GE was not only one of the world's biggest industrial corporations but also 'a model of management-a laboratory studied by business schools and raided by other companies seeking skilled executives." Each of GE's chairmen contributed to the development of GE's management system, and these contributions diffused well beyond GE's corporate boundaries: Charles Coffin (1892-1922) married Edison's industrial R&D laboratory to a business system capable of tuming scientific discovery into marketable products, Ralph Cordiner (1950-63), assisted by Peter Drucker, established GE's Crotonville management development institute and decentralized GE'S operational management to 120 departmental general managers. Fred Borsch (1963-72), devised GE's corporate planning system based on stra- tegic business units and guided by portfolio Management techniques, which became a model for most diversified corporations, Reg Jones (1972-81) integrated strategic planning with financial control to create a comprehensive system for the corporate headquarters to manage its businesses. CASE 20 RESTRUCTURING GENERAL ELECTRIC 603 Jack Welch (1982-2001) had energized GE by stripping out layers of hierarchy, introducing a rigorous, and demanding performance management system based on stretch targets and powerful incentives for their achievement, and spear- headed a series of initiatives designed to root out complacency and to drive change. Welch reformulated GE's business portfolio through exiting low-growth extractive and manufacturing businesses and by expanding services-financial services in particular. By the time he retired, GE was 'a bank disguised as an industrial conglomerate. Jeff Immel (2001-17) returned GE to its manufacturing roots through divesting its financial service and entertainment businesses, and increasing integration among the industrial businesses through sharing technology, increasing global presence, and exploiting synergies in sales and marketing GE's Business Portfolio In a world of turbulence, GE had always viewed its diversified portfolio of businesses as a source of stability over the business cycle. In 2015, Jeff Immelt stated: "Diversity provides strength through disruptive events and commodity cycles," thereby consti- tuting a key "source of value from a multibusiness company's The guiding theme of Immelt's restructuring of GE's portfolio of businesses was exploitation of profitable opportunities for long-term growth. Immelt identified global trends of key importance to GE: Demograpby: The aging of the world's population would create opportunities for goods and services required by older people-healthcare especially. Infrastructure: GE anticipated massive investments in infrastructure including energy, water, and transportation Emerging markets would offer rates of GDP growth around three times those of the world as a whole. Environment: The problems of global warming, water scarcity, and conservation required new technologies and innovative business responses The outcome was to recreate GE as an infrastructure company-a diversified cor poration directed toward global needs for aviation, rail transportation, power genera- tion and distribution, oil and gas production, and medical hardware. Figure 2 shows FIGURE 2 The changing balance of General Electric's business portfolio 2001 2005 2016 Insurance 15% Insurance Capital Finance 25% Capital Finance Capital Finance Infrastructure 4196 Infrastructure 345 Infrastructure 75% Plastics, Media 20% Pustics, Media 1546 ASES TO ACCOMPANY CONTEMPORARY STRATEGY ANALYSIS Immelt's depiction of GE's changing business composition. During his 16-year tenure, Immelt reconfigured GE through the acquisition of infrastructure-related companies and the divestment of consumer and financial service businesses. Table 2 shows GE's principal acquisitions and divestitures during 2004-17 TABLE 2 General Electric's principal acquisitions and disposals, 2004-17 Year 2004 Disposals Life and mortgage Insurance spun off as Genworth Financial 2005 2006 Acquisitions Acquires entertainment assets of Vivendi Universal for $12 bn to form NBC Universal (80% owned by GE GE Healthcare buys Amersham PLC for $9.5 bn. GE Capital acquires Dilard's credit card unit for $1.25 bn. GE Security acquires InVision Technologies (airport security equipment). GE Commercial Finance acquires the financial service business of Bombardier for $14 bn. GE Healthcare acquires IDX Systems, a medical software form for $1.2 bn. GE Water & Process Technologies acquires Zenon Environmental Systems for $758 m. GE Aviation acquires Smiths Aerospace for $46 bn GE Oil & Gas acquires VetcoGray for $14b NBC Universal buys Weather Channel for $3 bn. GE Capital acquires Merrill Lynch Capital, Citicapital and Bank BPH GE Healthcare acquires Clarient for $0.6 bn GE Oil and Gas acquires Dresser Inc. (53bn). Wellstream PLC (513 bn.. and the well support division of John Wood Group PLC (52.9 bn). GE Advanced Materials sold for $3.8 bn GE Insurance Solutions and GE Life sold for $6.5 bn GE Plastics is sold to Saudi Arabia Basic Industries for $11.7 bn. 2007 2008 2010 2011 51% of NBCUniversal sold to Comcast for $138 bn. GE Capital sells Mexican assets to Santander 2012 2013 GE Capital acquires $7 bn bank deposits from MetLife Buys oilfield pump maker, Lufkin Industries, for $3.1 bn Acquires Alstom SA's power business for $13.1 bn 2015 Remaining 49% of NBC Universal sold to Comcast for $16.7 bn. GE Antares Capital (private equity) $120 bn. GE Capital (vehicle services) $6.9 bn. GE Capital (transport finance) $89 bn GE Capital (ending & leasing) to Wells Fargo for $26.5 bn Synchrony (credit cards) for $216 bn. Sale of GE Appliances to Qingdao Haler for $5.4 bn. GE Water & Process Technologies sold to Suez for $34 bn 2016 2017 Acquires 62.5% of Baker Hughes (for $324 bn). merges it with GE Oil and Gas. Sources: General Electric press releases and all Street Journal CASE 20 RESTRUCTURING GENERAL ELECTRIC Shrinking GE Capital was a massive challenge given its size and contribution to GE's profitability. Despite Immelt's commitment to downsizing GE Capital, it continued to grow during 2001-07. In 2006 and 2007, GE Capital accounted for almost half of GE's total net profit (up from 25% in 2001). Only after the financial crisis of 2008-09 did GE take drastic action to divest financial services. The designa- tion of GE Capital as a "systemically important financial institution in 2013, which raised its capital reserve requirements, eliminated any competitive advantages it had derived from being a nonbank supplier of financial services. The only businesses that GE Capital retained were "vertical financial businesses'-those linked to GE's core industrial businesses. At the beginning of 2018, GE comprised eight major sectors. Table 3 shows these sectors' financial performance. Exhibit 1 describes their business activities. TABLE 3 General Electric segment financial results, 2013-2017 2017 2016 2015 2014 2013 36,795 28,903 27,746 26,770 Revenues (Smn.) Power Renewable Energy Oil & Gas 35,990 10,280 6273 6399 4824 9033 12.898 17231 17,341 Aviation Healthcare 27,375 19.085 23.990 16,450 24,660 17,639 26.261 18.291 21,911 19,116 18.299 18.200 4178 5933 5885 4713 4923 1987 8751 5650 8404 109,574 8338 116,157 112.814 108,609 103,269 Transportation Lightingla) Total industrial segment revenues GE Capital Total segment revenues Segment profit Power 9070 10,905 10.801 11,320 11,267 125,227 123,719 119.410 120,894 114536 2786 5091 4772 4731 4437 727 576 431 694 485 220 1392 2427 2357 2758 4973 6642 6115 5507 4345 3448 3161 2882 3047 3048 Renewable Energy Oll & Gas Aviation Healthcare Transportation Ughting Total industrial segment profit GE Capital Total segment profit 824 1064 1273 1130 1166 93 199 431 381 674 17966 14,740 17.598 17,764 16.220 (6765) (1251) (7983) 9983 1209 18,973 7975 16,347 401 16,621 (Continues SES TO ACCOMPANY CONTEMPORARY STRATEGY ANALYSIS TABLE 3 (Continued 2017 2016 2015 2014 2013 Operating Margins (%) Power Renewable Energy 7.74 13.84 16.51 17.05 16:57 7.07 6.38 6.87 10.85 1005 Oil & Gas 1.28 10.79 14.75 14.45 13.59 Aviation 24.26 23.29 22.33 20.73 19.83 Healthcare 18.04 1728 1634 16.65 16.75 Transportation 19.72 22:58 21.46 20.00 19.81 Lighting 468 413 7.70 5.13 4.57 12.69 15.60 Total industrial segment GE Capital 16:54 1621 15.71 -74.59 -11.47 - 7391 10.68 356 Total 6.37 1321 8.36 15.69 1451 Note: Lighting includes Appliances before 2017 Source: General Sectric 10K report for 2017, EXHIBITI General Electric's business segments, January 2018 GE Power. The acquisition of Alstom had made GE the world's biggest supplier of equipment for generating and distributing electricity GE Power was also GE's big- gest division with 83,500 employees in 2017. It suppled gas turbines, steam power systems, power plants, main tenance and service solutions for power generation, industrial gas engines for power generation, nuclear reactors and fuel (GE Hitachi Nuclearl. electricity trans- mission and distribution systems, and electric motors Dung 2017, GE Power was hit by a decline in world wide demand and made a loss of $09 bn arising from a write down of inventory GE Renewable Energy employed 24,000 people in 2017 and was one of the world's top five suppliers to the wind power industry, supplying wind turbines and related hardware, software, and services for both onshore and offshore generation GE was a world-leader in wind generation technology: its Haliade-x wind turbine launched in March 2016, is 250 m tall and can generate 12M. GE Renewable Energy also supplies products and services to the hydropower industry GE Oil and Gas, with 64.000 employees in 2017. had been built by multiple acquisitions between 2007 and 2016. By merging with Baker Hughes, created Baker Hughes, A GE Company (BHGE), the world's second biggest olfield services supplier after Schlumberger its products include driling equipment oilfield fluids and chemicals, pumps, pressure control equipment, subsea production systems flexible pipeline systems, equip ment for production platforms, and products for refining and petrochemicals. Oitfeld services include well eval ution, drilling, downhole completion welbore inter- vention, wireline services, and decommissioning Profits declined in 2017 due to reduced capital expenditure by oil and gas companies and restructuring costs arising from the acquisition CASX 20 RESTRUCTURING GENERAL ELDTIC 607 GE Aviation with 44,500 employees in 2017, was the world's leading supplier of jet engines together with avionics systems and after market services, GE Aviation's 40-year-old joint venture with Safran of France. CFM International supplies its highly successful LEAP engine for which there was an order backlog of 12.550 at the beginning of 2018, GES GE9X engine, bult using light- weight carbon fiber and 3D printing which is to be launched in 2018, is the world's biggest turbofan engine. GE Healthcare, with 52,000 employees, is the world's leading supplier of dagnostic imaging systems using X-rays digital mammography, computed tomography, magnetic resonance, molecular imaging and ultrasound It also provides systems for patient monitoring, Infant incubation, respiratory care, anesthesia, and cellular and gere therapy GE Transportation with 8000 employees in 2017, supples desel-electric locomotives together with support services parts software solutions and data analytics. It also supplies diesel engines and drive sys tems to the shipping and mining industries. Despite GES technical leadership in locomotives, the world market was dominated by CNR and CSR of China Following them was CLW of India and Bombardier of Canada in May 2018, the merger of GE Transportation with US rail equip mert manufacture, Wabtec Corp, was announced The combined company would be owned 499% by Watte shareholders 40 256 by GE shareholders, and 994 by G GE Lighting with 7500 employees in 2017, is com- prised of a consumer lighting business focused on LED lighting and Current, which provided lighting solutions for commercial, industrial and municipal customers. At the end of 2017, the business was put up for sale and a management buyout had been agreed upon for GE Lightings business in Europe, Middle East and Africa GE Capital with 4000 employees in 2017. had been reduced to financial services that were closely aligned with GE Industrial businesses. These included Industrial Finance, providing equipment financing for the health care and additive businesses, Energy Financial Services, which offers financial solutions and underwriting for Powes Renewable Energy, and Ol Gas and GE Capital Aviation Services the world's biggest aircraft leasing company. During 2018 its industrial Finance and Energy Financial Services would be shrunk considerably How evecit continued to be haunted by its past-during 2008 14, would pay $15 bilion to top up the reserves deficiencies of previously-owned insurance companies. Planning for a New General Electric During his 14 months as CEO, John Flannery had taken a systematic approach to GES restructuring, making it clear that a wide range of strategic options for GE were under consideration: "That assessment is continuing and focuses on maximizing value, all options on the table, no sacred cows." The corporate review "could result in many, many different permutations, including separately traded assets really in any one of our units, if that's what made sense." Any restructuring of GE would need to address two major questions: What were the sources of GE's current problems and, did GE add value to its constituent businesses or destroy it? The Sources of GE's Problems Analyses of what had gone wrong at GE were plentiful. Most of these focused on the role of Flannery's predecessor, Jeff Immelt, and some traced the problems further back to the Welch era CASES TO ACCOMPANY CONTEMPORARY STRATEGY ANALYSIS It was clear that Immelt was guilty of decision-making errors-particularly with regard to timing Criticisms focused in particular on the following: Il-judged acquisitions. Several commentators pointed to GE overpaying for the companies it acquired. The principal evidence of this related to Alstom. During the long delay in gaining approval for the acquisition, the market for power generating equipment took a downturn, and GE was forced to offer more concessions to Alstom and the French government. Hence, by the time the acquisition closed, Alstom was worth considerably less than the price GE was paying. Timing was also amiss for several of GE's acquisitions in oilfield services: Dresser, Wellstream, John Wood, and Lufkin were all bought when oil prices were booming. Scott Davis of Melius Research estimated that GE's total return on Immelt's acquisitions were less than half of what GE would have earned by simply investing in stock index mutual funds. The Economistesti- mated that GE was paying much more for the businesses it bought than what it received for those it sold.' Poor cash flow management. During the 21st century, GE lost its reputation for financial conservatism along with its triple-A credit rating. At the core of con- cerns over its financial management has been an erratic approach to cash-flow management. The financial crisis was, of course, unexpected, but the fact that GE was forced to obtain $3 bn. in emergency funding from Warren Buffett's Berkshire Hathaway Inc. and $139 bn. in loan guarantees from the federal government appears not to have alerted GE to the risks inherent in GE Capital. Particular criticism has been directed at GE's stock buyback program: in the three years prior to the dividend cut in 2017, GE spent $49 bn. on buying its own stock. According to the Financial Times, GE's free cash flows from its industrial businesses failed to cover its dividend during 2015-17.11 Over-optimism. GE's failure to guard itself against risk and pay adequate attention to early warning signs have been interpreted by some GE-watchers as symptoms of top-management's overconfidence and reckless optimism. According to some current and former GE executives, Immelt and his top dep- uties engaged in success theater"-they projected an optimism about GE'S businesses and its future that didn't always match the reality of its operations or its markets." In particular, during 2017, when signs of flagging sales and mounting inventory were emerging at GE Power, Immelt was slow in acknowl- edging the problems. Problems with GE's financial accounting. If GE had been slow to recognize and react to emerging problems, one factor might have been its accounting prac- tices, which for decades had been designed to impress Wall Street, but may also have insulated management from the reality of business performance. Under Jack Welch's leadership, GE Capital became a valuable tool for managing GE's quarterly earnings: "Unlike a factory, GE Capital's highly liquid assets could be bought or sold at the ends of quarters to ensure the smoothly rising earn ings that investors loved." Dubious accounting practices also surfaced in GES industrial businesses. At GE Power, sales of upgrades to make existing gas tur- bines run more efficiently were booked as current revenues, without taking into account the effects of these sales would have on reducing future service revenues CASE 2 RESTRUCTURING GENERAL ELECTRIC 609 Does GE Add Value to Its Businesses? Ultimately, the question of whether or not GE should be broken up rested on the issue of whether GE's corporate umbrella added or subtracted value from the businesses. At the time Culp was appointed CEO, with its share price depressed and facing a slew of legal and regulatory problems, it was likely that GE would be worth more if it was broken up and its constituent businesses either sold or floated as independent com- panies. In January 2018, the Financial Times valued GE's constituent businesses as Aviation at $85 bn., Healthcare at $56 bn., and Power at $36 bn. Adding other smaller businesses and subtracting debt and other liabilities (including pensions) gave a sum of-the-parts valuation of costs, the result was something close to $158 bn. Although this was greater than GE's market capitalization, the Financial Times cautioned that: "It does not look as though there is a pot of gold there waiting to be uncovered." Previous CEOs, Immelt and Welch, had argued that GE created value for its busi- nesses through several mechanisms. These were: 1 Reducing risk. According to Immelt: "The GE portfolio was put together for a purpose-to deliver earnings growth through every economic cycle. We're con- stantly managing these cycles in a business where the sum exceeds the parts. 136 To the extent that GE's business diversity did smooth its overall cash flows, then it seemed that the major benefit of this was giving GE greater independence from external financing 2 Portfolio management. Both Welch and Immelt had radically changed and reconstituted GE's business portfolio. Welch had built a huge financial services business; Immelt had re-created GE as an industrial corporation heavily focused on infrastructure. The rationale was to exit slow-growing, low.margin sectors to exploit the growth and profit opportunities of more attractive industries. In building GE's presence in jet engines, medical equipment, and systems for gener- ating and distributing electricity, Immelt was widely perceived as having aligned GE's businesses with long-term global growth trends. However, The Economist's Schumpeter column doubted the effectiveness of portfolio management in cre- ating value: "The cost of churning capital in predictable ways can be significant ... GE has paid a multiple of 13 times gross operating profits for the businesses it has bought and got 9 times for those it sold. Some nine-tenths of its industrial capital is now comprised of goodwill, or the premium that a firm paid above book value for its acquisitions." For portfolio management to work well, corporate management must be willing to exit businesses whose long-term prospects are deteriorating. This is easier for a private equity firm than for a diversified industrial corporation where long- established businesses are likely to be protected by sentimental attachment and entrenched political power. A feature of Immelt's leadership was the long length of time it took to exit from financial services and domestic appliances, 3 Exploiting synergies. A central theme of Immelt's 16-year tenure as CEO was building and exploiting linkages among GE's different businesses. While Welch had been a passionate advocate of knowledge sharing within GE, Immelt's emphasis was on putting in place the for such sharing to take pla Sharing technology was the priority. Under Immelt's leadership, GE built a net- work of eight Global Research Centers. By 2015, GE had 37,000 technologists STO ACCOMPANY CONTEMPORARY STRATEGY ANALYSIS engaged in R & D within its businesses and its corporate research centers. Corpo rate-level research programs addressed technologies with applications to multiple businesses. These included molecular imaging and diagnostics, nanotechnology, energy conversion, advanced propulsion, sustainable energy, and security tech- nologies. The greatest importance was attached to establishing GE's leadership in the Internet of things--the "interface of the physical and digital worlds through combining data and physics." This involved the use of the continuous data from embedded sensors on jet engines, locomotives, oil and gas equipment, medical diagnostic, electricity generators, and so on, as an input to the software that managed maintenance schedules, fuel optimization, accident prevention, factory automation, and enterprise management In 2011, GE opened a new software center in San Ramon, CA to develop applications of big data and artificial intelligence that would lead GE's digital transformation. The new software center formed the centerpiece of GE Digital, a new business division created in September 2015 that brings together all of the digital capabilities from across the company into one organization." GE Digi- tal's efforts focused on the development of its Predix platform, a cloud-based operating system for industrial applications that uses sensor-generated data within a next-generation industrial automation system. However, during 2016 and 2017, problems with the Predix platform had increased its development costs and slowed its rollout to third-party customers. As a result, in February 2018, Flannery announced narrowing the focus of GE's digital business and targeting existing customers with its Predix operating system." Sales and marketing provided another rich area for cross-business synergies Increasingly, Ge bundled products and support services to offer customized "customer solutions. In the case of a new hospital development, for example, there might be opportunities not just for medical equipment but also for lighting, turbines, and financing. Such opportunities were particularly impor tant internationally. In 2009, GE launched its Company-to-Country" strategy to build relationships with host governments across multiple infrastructure development projects. This strategy involved looking beyond China, India, and Brazil; in 2012, GE announced that "Nigeria should be our next billion-dollar country." 4 The GE management system. The management system that Larry Culp inherited was-despite its restructuring by Jack Welch and reformulation by Jeff Immelt-a product of 120 years of continuous development. Many of its processes were so deeply embedded within GE's culture that they were inte- gral to its identity and world view. At the core of GE's management system were management development-its "talent machine"-and its system of performance management. GE's commitment to leadership development was indicated by its reli- ance on internally developed senior executives. Its effectiveness in devel- oping leaders had given it the status of a "CEO factory-former GE managers are chief executives of companies throughout the world. Key components of its management development system were its corporate university at Crotonville, New York, and its 'Session C" system for tracking managers' performance, planning their careers, and formulating succession plans for every management position at GE from department heads upward. Did Culp's appointment as CEO imply that GE had lost faith in its management development capability? CASE 30 RESTRUCTURING GENERAL ELECTRIC 611 GE's performance management system was based heavily on objective, quantitative performance measures: "Nothing happens in this company without an output metric," observed Immelt. Managers were set demanding performance targets, then given strong incentives for their attainment. However, while many performance variables-revenue, profits, quality, safety-where conducive to quantification, many of the performance variables that had been emphasized by Immelt-innovation, cross-selling, knowledge sharing-were much more difficult to quantify and monitor. If, as Immelt had claimed, GE's performance depended upon integration-"Our managers have to work cross-function, cross-region, Cross-company then its performance management system needed to provide the right incentives for such collaboration Which Corporate Model for GE? As Larry Culp considered the restructuring initiatives that were currently underway-the merger of GE's Transportation division with US railroad equipment producer, Wabtech Corporation to create a jointly-owned company and the spin off of GE Heathcare and BHGE (Baker Hughes) as separately quoted companies with their shares distributed to GE shareholders-he pondered the type of company that GE should become. The obvious model was that of Danaher. Danaher was a widely diversified, technology- based company built through acquisition. Its strong performance was the result of the application of a common set of management principles and processes based upon lean production and continuous improvement Chaisen)the "Danaher Business System - to carefully selected acquisitions. Although Danaher's portfolio of over 100 businesses were clustered in four main areas: life sciences, diagnostics, dental, water quality, and product identification, Danaher did not attempt to create the huge integrated divisions that GE possessed. An alternative model was the business system created by Siemens AG. The German giant had a similar background and profile to GE: it was founded in the late 19th century and its biggest businesses were power generation systems (including wind power), medical equipment, and industrial automation. However, unlike GE, Siemens had moved toward greater decentralization rather than Ge's path of closer integration Siemens' CEO. Joe Kaeser, described the Siemens model as a "fleet of ships with divi- sions becoming semiautonomous and separately listed. Siemens' medical equipment unit, Healthineers, was listed in March 2018. Like GE, Siemens' had suffered from the sharp reduction in world demand for gas turbines-however, the fall in revenues and profits in its power division was much less than that experienced by GE. During the three years to June 2018, Siemens share price increased by 22% that of GE's fell by 48%. APPENDIX: Extracts from General Electric Company Update, June 26, 2018 As you know, we have been working to determine the appropriate longer term stra- tegic focus for GE. There are three essential elements of this strategy: one is focusing our portfolio for growth and shareholder value creation; the second is strengthening our balance sheet; and the third is a market shift in how we run the company. With respect to our portfolio, our Aviation, Power and Renewables businesses will be the core of GE going forward. These are three formidable franchises where we've TO ACCOMPANY CONTEMPORARY STRATEGY ANALYSIS built leadership positions over many decades. These businesses also have significant strategic linkages. They share technologies, digital and additive strategies, and business models. While our core Aviation, Power and Renewable businesses can thrive inside of the current GE framework, we think substantial value can be created by moving other businesses outside of GE. To implement that strategy, we are creating a separate stand-alone Healthcare company and we also intend to fully separate BHGE. These are two strong and competitive businesses with leading positions and strong growth pros- pects but they both have various constraints operating inside the current GE construct. We believe these businesses can achieve greater results for employees, customers, and our owners as stand-alone companies. The pending merger of our Transportation business with Wabtec was driven by the same strategic approach. We will begin the process of separating our Healthcare business immediately. We will monetize approx- imately 20% and approximately 80% of Healthcare will be distributed tax free to our shareholders through a spin or split ... Oil & Gas was separated from GE in July of 2017 when we made the strategic decision to combine it with Baker Hughes. There's strong industrial logic for the transaction, the companies are much stronger together and shareholders are getting the benefit of significant synergies both on the revenue and cost side as well as benefiting from substantial combined technology. We expect to pursue an orderly separation of the company within 2-3 years with a focus on max- imizing value for BHGE and GE. Strengthening the balance sheet of the company is a top priority for us. This will allow us the flexibility and capacity to invest in growing our core businesses going forward. We will reduce our net debt by about $25 billion, and this will bring our net debt-to-EBITDA below 2.5 times by 2020. We will run the company with a substantially higher cash balance and reduce our use of commercial paper. Our strategy with regard to GE Capital is clear, we're making it smaller and more focused. We are reducing assets by $25 billion, and we'll bring our debt to equity to less than 4 times by 2020. We are aggressively working on actions and alternatives to mitigate, reduce or eliminate our exposure to long-term care insurance. As I outlined at EPG, we will run GE Company in a fundamentally different way going forward. Our businesses will be the center of gravity and will run on a new operating system that we believe will improve our operations and cash performance. These changes will reduce corporate costs by at least 500 million by 2020. We expect this number to grow over time as this velocity is applied across all levels of the company, This is in addition to cost actions already announced in 2017 and 2018. In conjunction with previous actions, today's announcement marks the emergence of a new GE, a high-tech industrial GE. A simpler, stronger and more focused company at the core, a strengthened balance sheet, a new operating system and a bright future for our Healthcare and BHGE businesses. This is a GE that is equipped to fight for the future. ... As I've said previously, the steps we're taking are really a means to an end, the end being a simpler, stronger and more focused company where our quality assets can reach their true potential and flourish in the decades ahead. We sought to posi- tion the businesses in an environment guided by 4 basic principles: the maximum ability to pursue their organic and inorganic investment strategies, strong alignment for management incentives linking performance and reward; reducing complexity and cost, while improving decision-making speed; and making sure any central essential services are subject to a market test by the business units. We are fundamentally invert ing the company to make the business units the center of gravity. I want to focus the businesses externally into the market. CASE STRUCTURING GENERAL ELECTRIC 613 We'll have a much smaller corporate focused on strategy and execution, capital allo cation, talent development and governance. The entire fabric of the company will be one of continuous improvement driven by operating leaders using well-proven tools, like Lean and Six Sigma. Digital and Additive strategies will continue to drive customer value and performance. We believe that these changes will yield substantial improve ments in performance over time. There will be improved focus, better accountability, clear capital allocation decisions, more strategic optionality and better alignment of compensation. Our plan will create a strong, exciting and growing GE built on oper- ational execution and robust industrial logic. Going forward, GE will be comprised of Aviation, Power and Renewables, supported by Digital, Additive and the financing expertise of GE Capital These are leading businesses solving the world's toughest problems for our customers. By combining these strong franchises with a healthy balance sheet, we see numerous avenues to invest for growth. We see sustained strength and growth in Aviation going forward. We see growth in the overall Renewables market and in our expansion of market share into new areas, like offshore wind and storage. We see earnings growth in the turnaround of our Power business with 1/3 of the world's electricity from our installed base and 2 of every 3 flights on our engines, GE is a high-tech industrial company that forms the backbone of a connected and electrifying world in every sense of those words. In addition to the strength of GE going forward, we're also unlocking substantial value for our shareholders. GE Healthcare is a leader in the drive to more effective and more efficient health-care outcomes. BHGE is uniquely positioned across the value chain as a full stream, oil & gas company. Our merger with Wabtec creates a global leader in the rail industry. As focused pure plays, they'll have greater strategic flexibility and more resources to pursue strategies dedicated to their industries. I want to spend a minute touching on each of these franchises. Our Aviation business is a market leading business with industry firsts spanning back decades and our tech- nology stack has never been stronger. Both the commercial and military businesses are strong. Our fleet is young, with 61% of our engines not yet at their second shop visit. That bodes well for our service business. We're managing well through the LEAP ramp. Despite the LEAP growth, we're maintaining 20%-plus margins through the launch. Our military portfolio is broad and we see opportunities for growth with our next-gen technologies both in the US and internationally. We were encouraged by the strong first quarter performance, especially in services. And finally, across the whole business, we're leveraging the strength of Additive, which is a game changer for high-tech com- ponent manufacturing. Additive is allowing us to reset our supply chain cost entitle- ment and we're seeing proof points across parts, systems and products. Aviation is a premier asset with over $200 billion in backlog and good visibility to long-term growth. We want to continue to invest and grow this franchise. Next is Power. While our results here have been unacceptable, this is a fundamen tally strong franchise with leading technology, a valuable installed base and expansive global reach. GE generates about 1/3 of the world's electricity and has about 1600 gigawatts of installed capacity. Gas, which is our largest segment, remains a key part of the world's long-term power generation mix. GE has approximately 7000 gas turbines in our installed base and we have a 20-year plus track record that demonstrates we can improve output, reliability and performance of those assets when we service them. We are a big player in grid, equipping 90% of transmission utilities worldwide. There are certainly macro and secular challenges to this business, but we are taking actions to remediate the issues that we saw in 2017 and to right-size our cost structure for a lower heavy-duty gas turbine market in the near term. This is a turnaround story, and we are confident in our ability to improve the future operating performance. We have TO ACCOMPANY CONTEMPORARY STRATEGY ANALYSIS a well-thought-out and detailed plan to reach the 10%-plus margins outlined at EPG Overall, this is valuable franchise that will be run better moving forward. Our Renewables business is an important part of the energy mix. Sixty-seven percent of 2017 global power capacity additions were from renewable sources, with some sources estimating 70% of 2018-21 additions from renewable sources. We are a leading player in onshore wind, gaining market share in 2017. We are making inroads into off- shore wind and have a strong hydro business. Renewables is a competitive and evolv- ing industry but one, we think, we're positioned well in going forward. Aviation, Power and Renewables are businesses that we feel are best positioned together to deliver results and drive shareholder value. These are all businesses marked by deep and complementary technology investment and differentiation and using that investment to grow our installed base and build high-value service stream annuities. Whether generating electricity on land or thrust in propulsion in the skies, the machines from these segments share a common core set of technologies, service platforms and global markets that make them stronger together than they would be if innovated in isolation. In fact, the first US jet engine created by GE evolved from the industrial gas turbine. While one is for power and one for flight, they both share a common architecture and operating environment that allow them to naturally have a common set of technology needs. Wind turbines, too, share many common traits. They are large spinning machines that generate megawatts of torque and power. That's very familiar to GE. I'll give you two examples of technology synergies. First, edge controls. For decades, we've devel- oped industrial controls for gas turbines, jet engines and more recently, wind turbines to ensure each operates safely and at the highest levels of performance and efficiency possible. With the exponential growth of computing power in the past decade, we're now combining controls with digital technologies in a very powerful way to further optimize the way we operate and maintain these machines. At our global research center, we developed a common industrial operating system called [Edge OS), which works in a wind turbine, jet engine or gas turbine. A second example is material science. The LEAP engine was the first to have a rev olutionary new material called ceramic matrix composites, or CMCs. It's a lightweight ceramic material engineered to be as strong as metal but able to withstand much hotter temperatures. It has been a real difference maker in our LEAP product offering. The development of CMCs actually started as a project in our gas turbine business. In fact, it was because the material performed so well in the field testing with gas turbines that led us to discover it could work in jet engines as well. With polymer matrix composites, or PMCs, GE Aviation first introduced lightweight composite fan blades in the GE90 engine, and we took that knowledge and quickly adapted it for Renewable Energy's wind blades On the services side, we had a massive installed base across all three businesses with 65,000 aircraft engines, 7000 gas turbines, and 35,000 wind turbines. These prod- ucts all have long lives and our services business model provides a very profitable recurring revenue stream. We realized many common synergies around how to execute and manage these long-term service contracts. The markets are similar, they're global and this is where we can tap into GE's deep global network and experience. Digital and Additive are substantial opportunities across all 3 segments that provide benefits to enhance growth and lower cost. We are certain that with focus and a strong balance sheet, GE will be a technology- driven growth story again in the coming years. CASE 20 RESTRUCTURING GENERAL ELECTRIC 615 As I said before, we've been methodically reviewing the portfolio and looking at the best structure or structures to maximize value and position our businesses for suc- cess. We are excited about the future of GE Transportation, Baker Hughes GE, and GE Healthcare. We announced the merger of Wabtec and GE Transportation last month. We are contributing Transportation at an attractive multiple and realizing $2.9 billion of cash proceeds, while our shareholders will benefit from the compelling long-term prospects and synergies of the combined platform The industrial logic of this deal is strong and there are good growth opportunities with GE's installed base and services offering combining with Wabtec's portfolio We are beginning the process of separating Healthcare immediately and expect to complete it in the next 12-18 months. We plan to monetize approximately 20%. We expect it to have a capital structure and capital allocation aligned to its peers. As part of the transaction, we will transfer approximately $18 billion of debt and pension obligations to Healthcare. With respect to the impact this will have on future divi- dends, it's our intention to maintain the current $0.48 dividend until the time Health care is established as a stand-alone entity. At that time, both GE and GE Healthcare will determine their future dividends with an intended payout ratio in line with their respective industry peers. Given the typically lower payout ratios in the health-care industry, this will likely lead to a reduction in the aggregate GE dividend at that time, We like the BHGE combination Customer reception has been positive and we're gaining traction across product lines. The realization of synergies, both top and bot- tom line, was premised upon GE's sharing of significant technology and expert with BHGE. This was contracted for at the time of the merger and is going well. BHGE is well positioned to thrive as an independent company. As I said earlier, we expect to substantially exit our direct ownership of this business within 2-3 years, Running the businesses as the center of gravity is the third major point of our announcement today. We're implementing a new way to run the company. We will focus all of our activity in the company around our businesses with a much smaller cor- porate headquarters. Corporate will focus on strategy, capital allocation, talent and gov- ernance, and we will reduce the size of corporate significantly with at least $500 million of additional corporate cost-out by 2020. As we apply the same principle to our busi- nesses, we expect incremental cost savings in the businesses during this period of time. As you know, we have historically run several organizations centrally. This will change. Centrally, run activities in shared services will be placed back in the hands of the businesses. Our business leaders will have full accountability for and ownership of their operations, and everything we do will be subject to a market test. There will be no central residual cost. Global research will now align under David Joyce. Our Global Growth Organization will be significantly smaller and focused on government relations and developing markets where we need strong resources to play its scale and manage risk. And GE Ventures will be refocused. It'll be focused on only the most urgent mar kets and new technologies as determined and paid for by our business leaders. Our digital strategy continues to focus on our core industries in our installed base, and we expect no cost drag from digital by 2020. We believe these actions will result in better execution, increased speed and additional cost reductions of at least $500 million. This is incremental to the more than $2 billion of cost-out we're actioning in 2018 Source: https://www.ge.com/investor-relations/sites/default/files/ge_webcast transcript_06262018_0.pdfStep by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock