Question

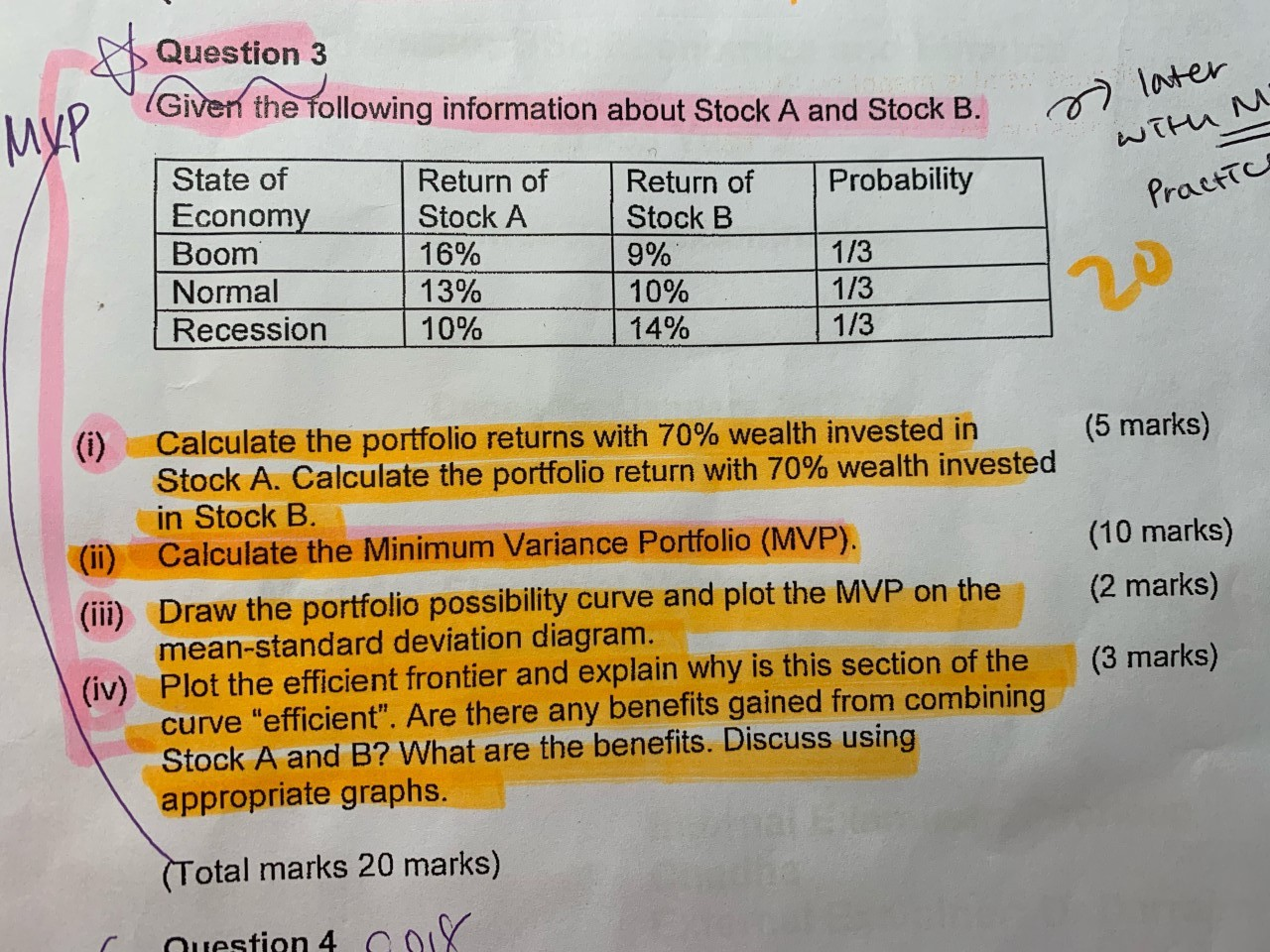

Q. given the following information about Stock A and Stock B. 1. Calculate the portfolio returns with 70% wealth invested in Stock A and Stock

Q. given the following information about Stock A and Stock B.

Q. given the following information about Stock A and Stock B.

1. Calculate the portfolio returns with 70% wealth invested in Stock A and Stock B.

2. Calculate the Minimum Variance Portfolio (MVP)

3.Draw the portfolio possibility curve and plot the MVP on the mean-standard deviation diagram.

4. Plot the efficient frontier and explain why is this section of the curve 'efficient'. Are there any benefits gained from combining Stock A and B? What are the benefits? Discuss using appropriate graphs.

Question 3 (Given the following information about Stock A and Stock B. MyP s later with M Practice Probability State of Economy Boom Normal Recession Return of Stock A 16% 13% 10% Return of Stock B 9% 10% 14% 1/3 1/3 1/3 (5 marks) (10 marks) (2 marks) (0) Calculate the portfolio returns with 70% wealth invested in Stock A. Calculate the portfolio return with 70% wealth invested in Stock B. (ii) Calculate the Minimum Variance Portfolio (MVP). (iii) Draw the portfolio possibility curve and plot the MVP on the mean-standard deviation diagram. (iv) Plot the efficient frontier and explain why is this section of the curve "efficient". Are there any benefits gained from combining Stock A and B? What are the benefits. Discuss using appropriate graphs. (3 marks) (Total marks 20 marks) nuestion 4 08Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Literacy And Money Script A Caribbean Perspective

Authors: Christine Sahadeo

1st Edition

3319770748, 978-3319770741