Q1)Assume today's date is 1 January 2034.

(please help do so i can understand my self in full details as much you can)

(not going to post anywhere)

(team 2 only)

The Board of Directors has asked you to evaluate an opportunity to export robots to a potential new overseas retail customer, 'Big Store Inc.'. 'Big Store Inc.' would like to run a trial promotion of your robots. The company would like to buy 100 robots from your company in 2034 at a special net sales price of W$2,500 per robot. If the 2034 trial is successful, the company has indicated it is likely to double the order quantity and would be prepared to match the net price you charge to your home customers in 2035.

Further information is provided below:

1. Special Equipment

The robots for this contract with 'Big Store Inc.' will require some modifications from the standard robot which your company produces and this will involve additional annual fixed production overheads of W$25,000 to cover the cost of hiring the special equipment required for this purpose.

2. Raw Materials: Standard Components

The robots manufactured for this order contract will require the same standard raw material components used in your business' regular production process.

3. Raw Materials: Special Components

The robots required for this contract will also require some 'special component' materials. The company has a stock of 150 units of these 'special components' in inventory which were purchased some years ago but which have been regarded as surplus to requirements and have been fully 'written off' in the accounts. These 'special components' originally cost W$500 per unit and they currently cost W$600 per unit to purchase. If not used for this project, the inventory of 'special components' will be sold in 2034 for sales proceeds of W$400 per unit. One 'special component' will be required per robot.

4. Staff Training

Also, an extra W$12,000 as a 'one-off cost' for staff training will be required to ensure that production staff are able to use the special equipment required for this contract.

5. Use of Factory Space

The project will require the use of some of the company's factory space which is currently surplus to requirements and would otherwise be sub-let, which would bring in income of W$16,000 in 2034.

6. Sales Staff Time

One of your company's sales staff estimates she spent 20% of her working hours in 2033 on this project which included travelling for meetings with 'Big Store Inc.' executives.

7. Marketing Costs

'Big Store Inc.' will run a special advertising campaign in 2034 to support this trial which will cost W$80,000 but requires your company to pay for 50% of these costs.

8. Fixed Cost Recovery Rate

For costing special projects such as this, your company has in the past applied a rate of 10% of net revenues arising when evaluating new orders in order to recover the business' recurring fixed costs (including admin expenses, overheads and direct labour costs).

explain the following

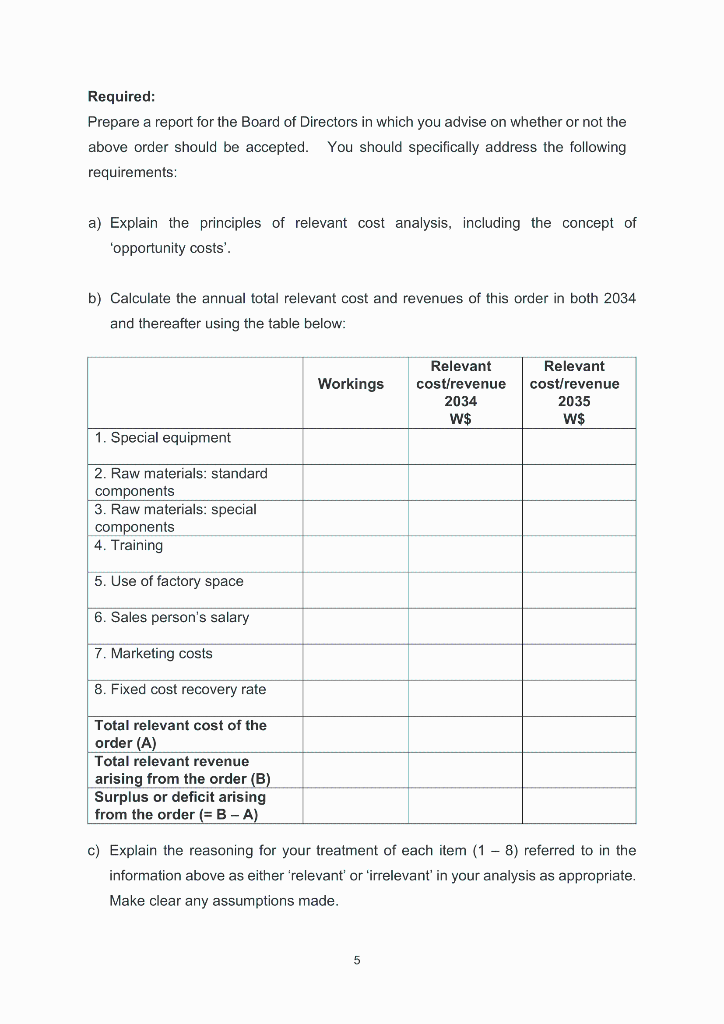

a) Explain the principles of relevant cost analysis, including the concept of 'opportunity costs'.

b) Calculate the annual total relevant cost and revenues of this order in both 2034 and thereafter using the table below:

c) Explain the reasoning for your treatment of each item (1 - 8) referred to in the information above as either 'relevant' or 'irrelevant' in your analysis as appropriate. Make clear any assumptions made.

d) Discuss two further considerations beyond the relevant cost analysis you have performed which you believe should be taken into account before a final decision is made.

e) Advise management on whether the order should be accepted.

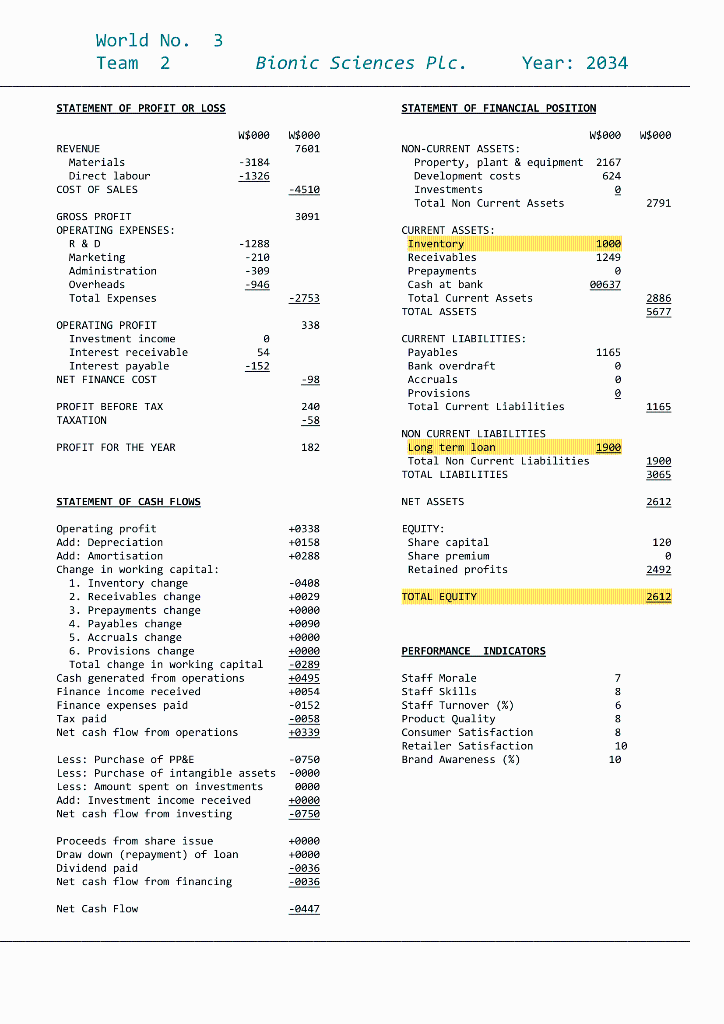

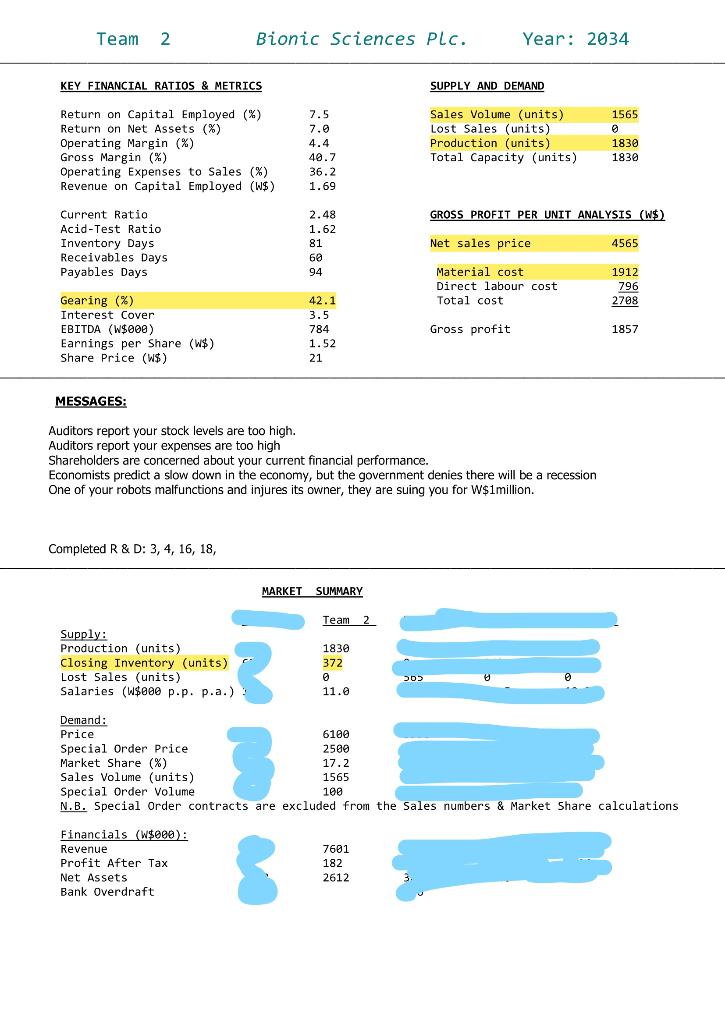

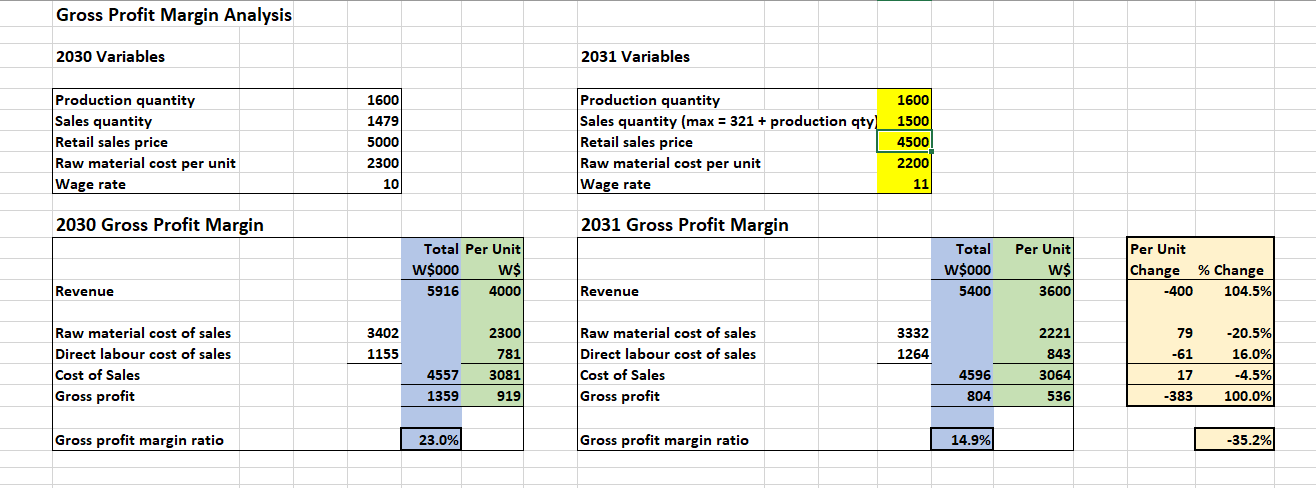

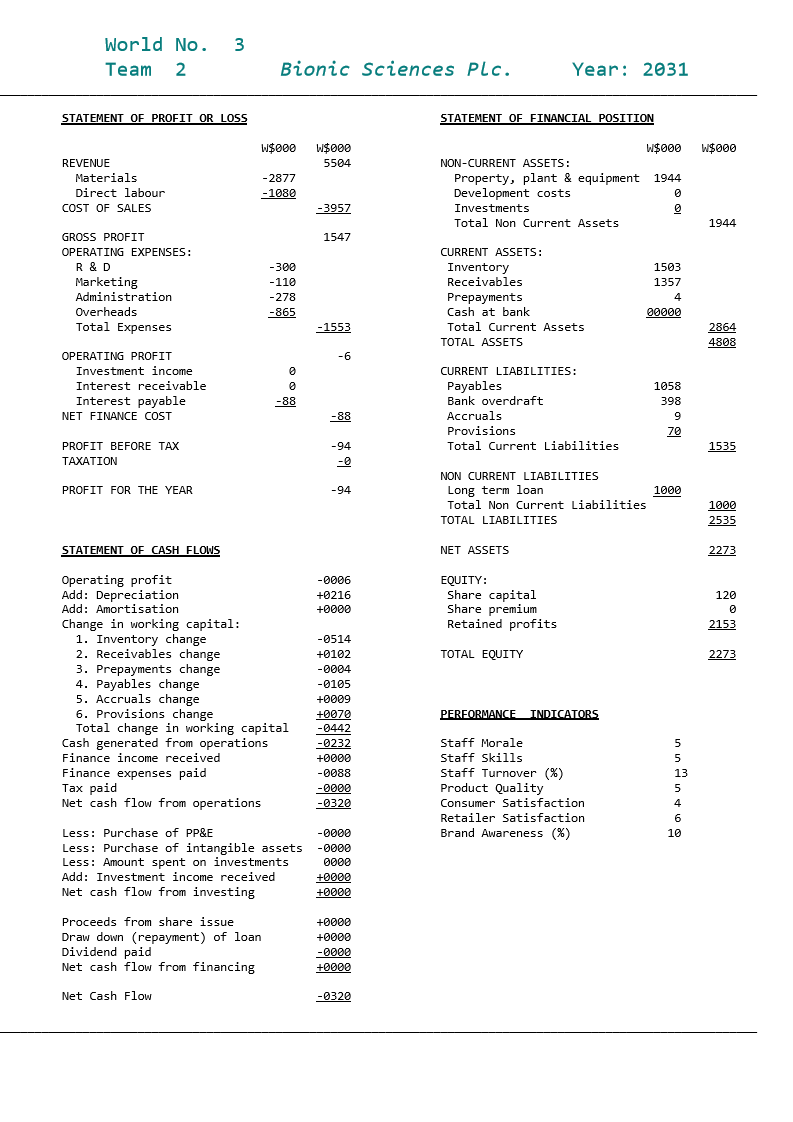

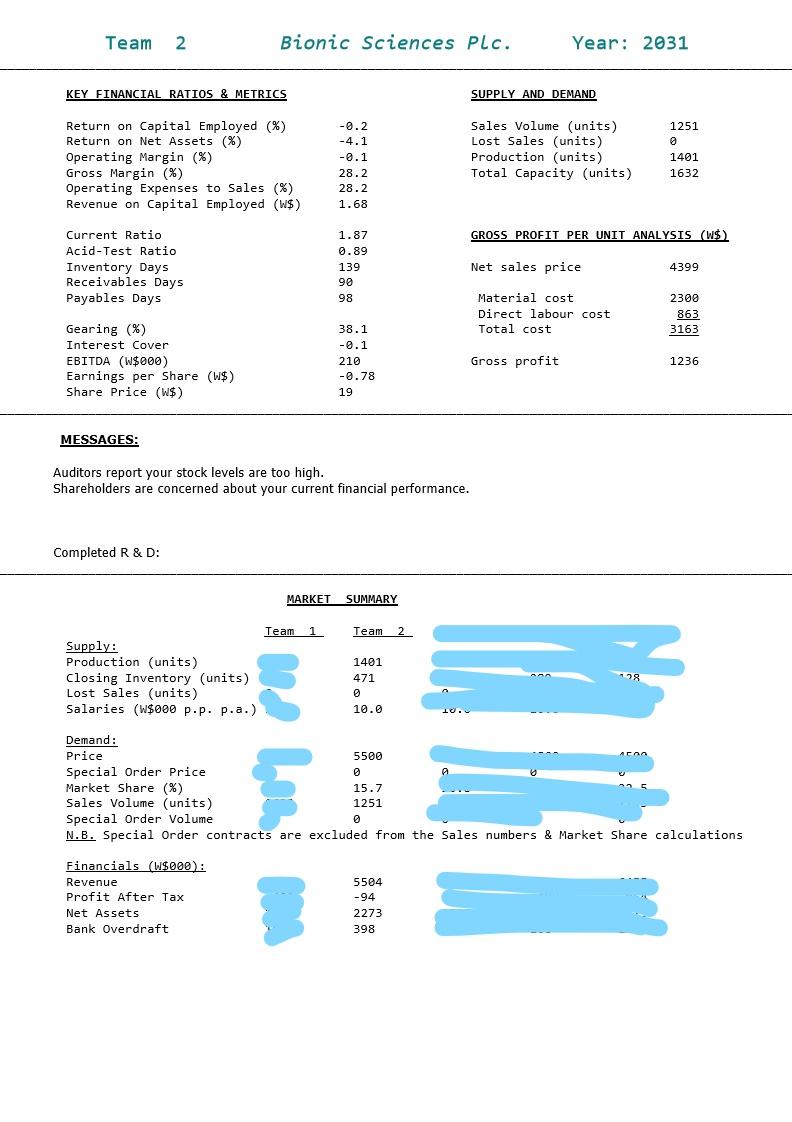

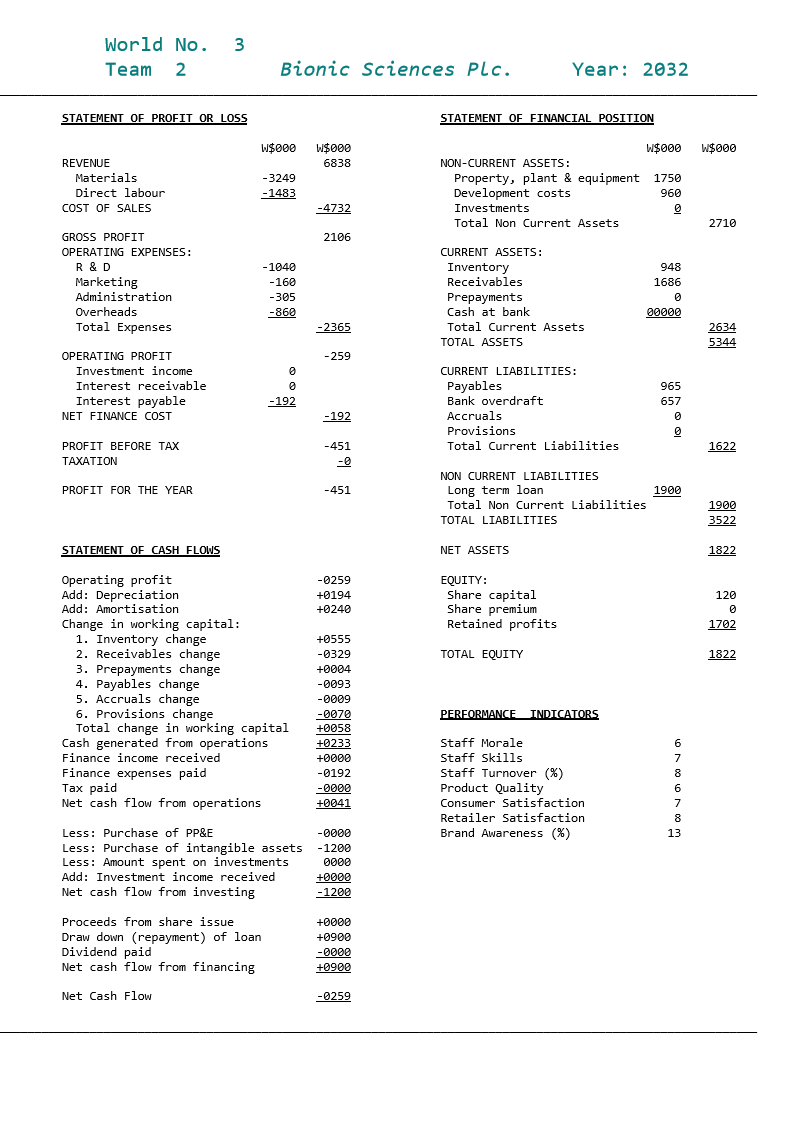

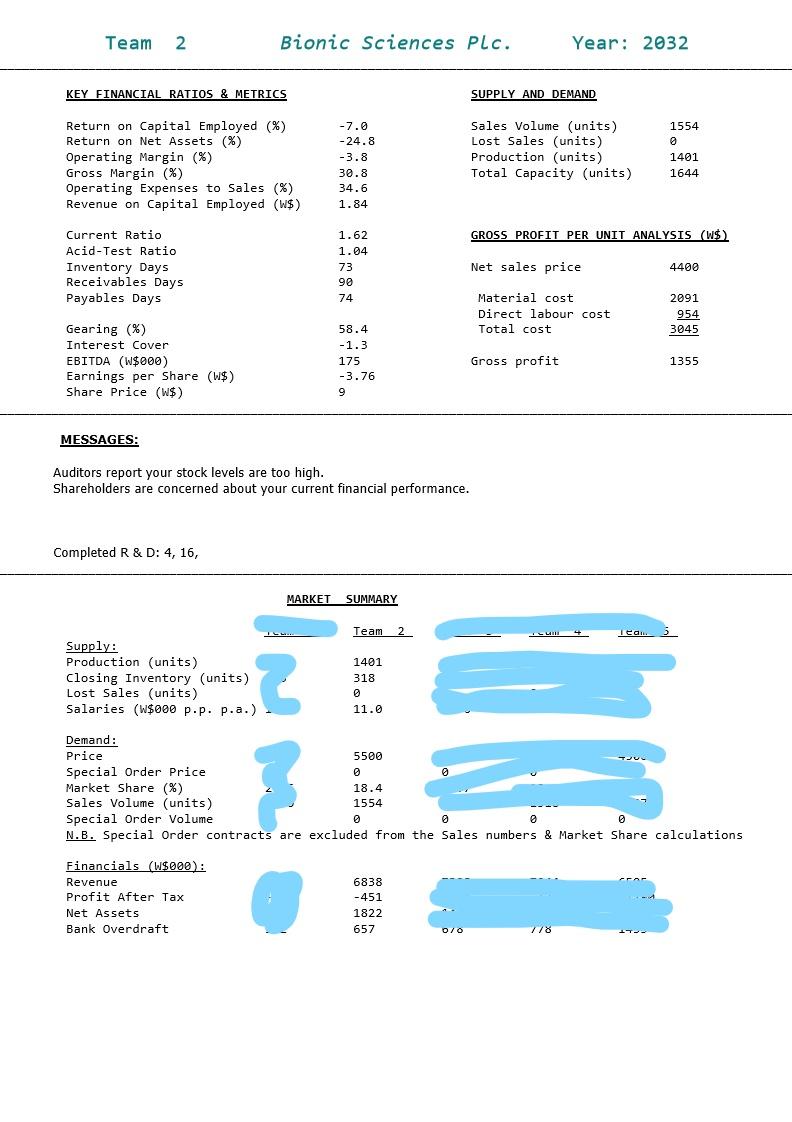

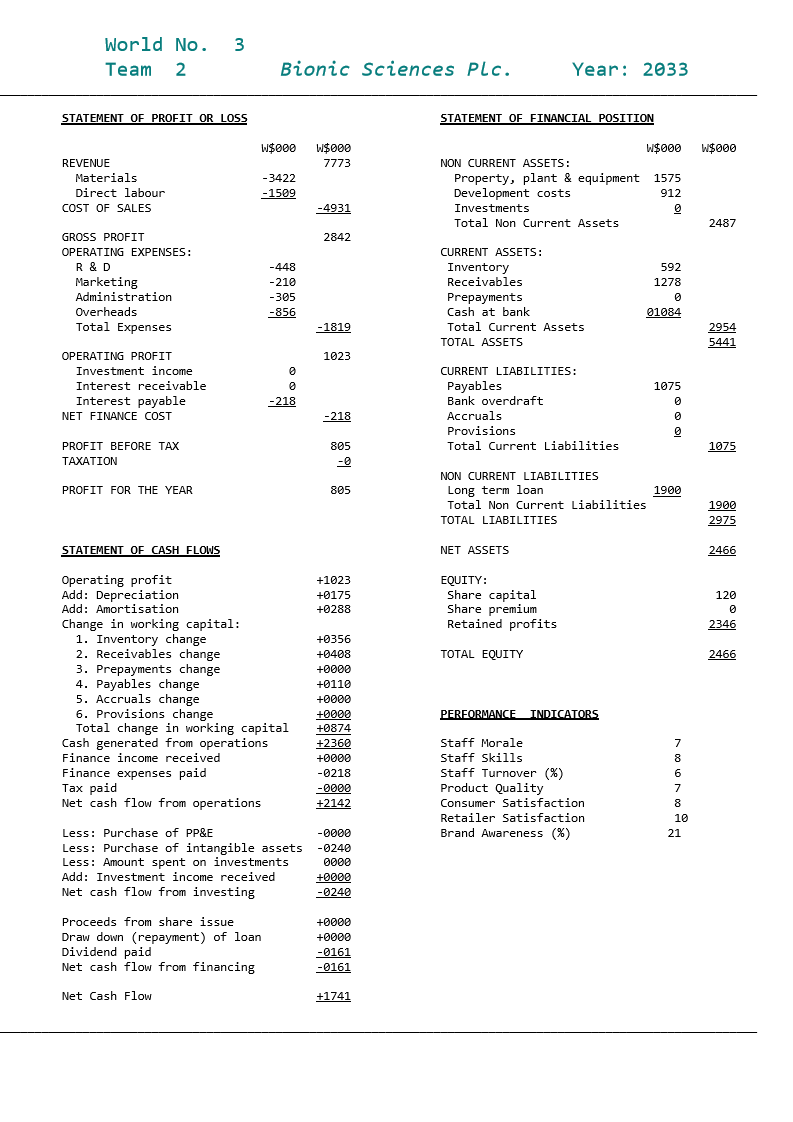

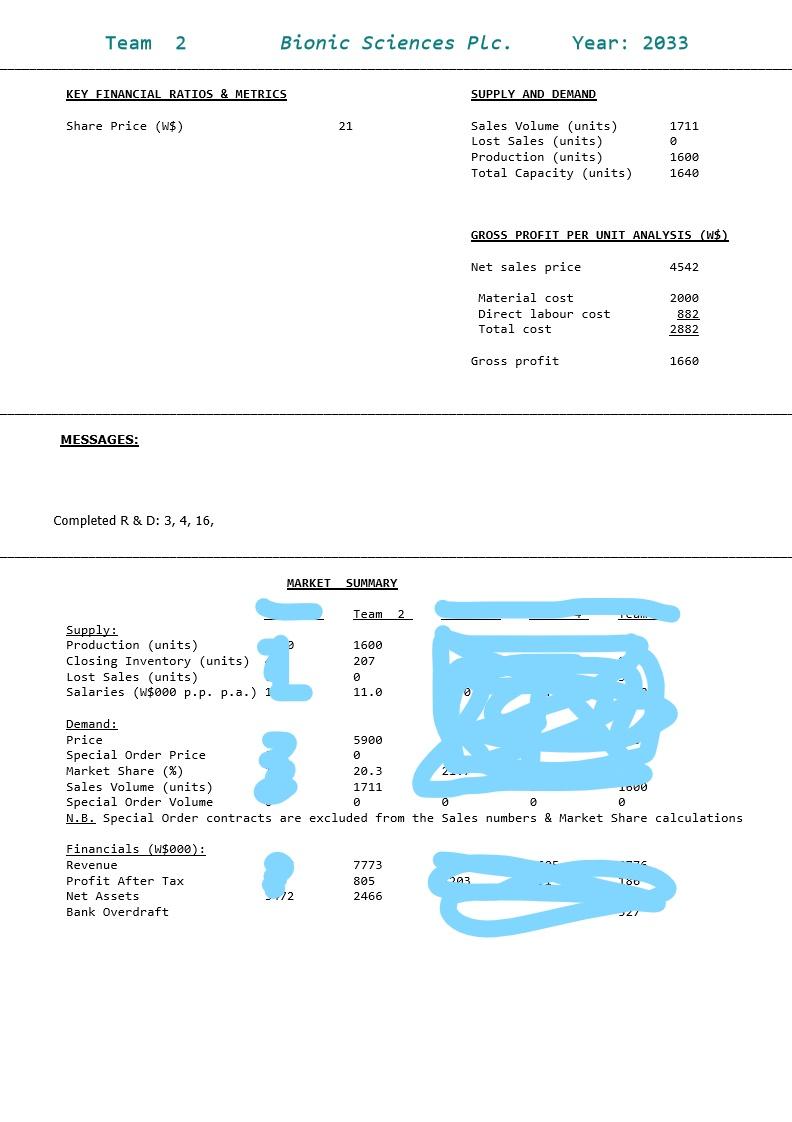

3 World No. Team 2 Bionic Sciences Plc. Year: 2034 STATEMENT OF PROFIT OR LOSS STATEMENT OF FINANCIAL POSITION W$ 000 W$000 W$ 000 7601 REVENUE Materials Direct labour COST OF SALES -3184 - 1326 W$ 000 NON-CURRENT ASSETS: Property, plant & equipment 2167 Development costs 624 Investments Total Non Current Assets -4510 2791 3091 GROSS PROFIT OPERATING EXPENSES: R&D Marketing Administration Overheads Total Expenses 1009 1249 - 1288 -210 -309 -946 CURRENT ASSETS: Inventory Receivables Prepayments Cash at bank Total Current Assets TOTAL ASSETS 08637 -2753 2886 5677 338 OPERATING PROFIT Investment income Interest receivable Interest payable NET FINANCE COST 1165 54 - 152 CURRENT LIABILITIES: Payables Bank overdraft Accruals Provisions Total Current Liabilities -98 3 1165 PROFIT BEFORE TAX TAXATION 240 -58 PROFIT FOR THE YEAR 182 1900 NON CURRENT LIABILITIES Long term loan Total Non Current Liabilities TOTAL LIABILITIES 1900 3065 STATEMENT OF CASH FLOWS NET ASSETS 2612 +9338 +0158 +0288 EQUITY: Share capital Share premium Retained profits 120 0 2492 TOTAL EQUITY 2612 Operating profit Add: Depreciation Add: Amortisation Change in working capital: 1. Inventory change 2. Receivables change 3. Prepayments change 4. Payables change 5. Accruals change 6. Provisions change Total change in working capital Cash generated from operations Finance income received Finance expenses paid Tax paid Net cash flow from operations PERFORMANCE INDICATORS -0408 +0029 +0000 +0090 +0000 +opee -289 +0495 +9054 -0152 -9058 +0339 Staff Morale Staff Skills Staff Turnover (%) Product Quality Consumer Satisfaction Retailer Satisfaction Brand Awareness (%) 7 8 6 8 8 10 19 Less: Purchase of PP&E Less: Purchase of intangible assets Less: Amount spent on investments Add: Investment income received Net cash flow from investing -75e -0000 0000 +0000 -0750 Proceeds from share issue Draw down (repayment) of loan Dividend paid Net cash flow from financing +0000 +0000 -0036 -8036 Net Cash Flow -9447 Team 2 Bionic Sciences Plc. Year: 2034 KEY FINANCIAL RATIOS & METRICS SUPPLY AND DEMAND Return on Capital Employed (%) Return on Net Assets (%) Operating Margin (%) Gross Margin (%) Operating Expenses to Sales (%) Revenue on Capital Employed (W$) 7.5 7.0 4.4 40.7 36.2 1.69 Sales Volume (units) Lost Sales (units) Production (units) Total Capacity (units) 1565 0 1830 1830 GROSS PROFIT PER UNIT ANALYSIS (W$) Current Ratio Acid-Test Ratio Inventory Days Receivables Days Payables Days 2.48 1.62 81 60 94 Net sales price 4565 Material cost Direct labour cost Total cost 1912 796 2708 Gearing (%) Interest Cover EBITDA (W$000) Earnings per Share ($) Share Price (W$) 42.1 3.5 784 1.52 21 Gross profit 1857 MESSAGES: Auditors report your stock levels are too high. Auditors report your expenses are too high Shareholders are concerned about your current financial performance. Economists predict a slow down in the economy, but the government denies there will be a recession One of your robots malfunctions and injures its owner, they are suing you for W$1million. Completed R & D: 3, 4, 16, 18, MARKET SUMMARY u Team 2 Supply: Production (units) 1830 Closing Inventory (units) 372 Lost Sales (units) 0 Salaries (W$200 p.p. p.a.) 11.0 Demand: Price 6106 Special Order Price 2500 Market Share (%) 17.2 Sales Volume (units) 1565 Special Order Volume 100 N.B. Special Order contracts are excluded from the Sales numbers & Market Share calculations Financials (W$000): Revenue Profit After Tax Net Assets Bank Overdraft 3 7601 182 2612 Gross Profit Margin Analysis 2030 Variables 2031 Variables 1600 1500 Production quantity Sales quantity Retail sales price Raw material cost per unit Wage rate 1600 1479 5000 2300 10 Production quantity Sales quantity (max = 321 + production qty_ Retail sales price Raw material cost per unit Wage rate 4500 2200 11 2030 Gross Profit Margin 2031 Gross Profit Margin Total Per Unit W$000 ws 5916 4000 Total W$000 5400 Per Unit ws 3600 Per Unit Change % Change -400 104.5% Revenue Revenue 3402 1155 3332 1264 Raw material cost of sales Direct labour cost of sales Cost of Sales Gross profit 2300 781 3081 919 Raw material cost of sales Direct labour cost of sales Cost of Sales Gross profit 2221 843 3064 536 79 -61 17 -383 -20.5% 16.0% -4.5% 100.0% 4596 4557 1359 804 Gross profit margin ratio 23.0% Gross profit margin ratio 14.9% -35.2% 3 World No. Team 2 Bionic Sciences PLC. Year: 2031 STATEMENT OF PROFIT OR LOSS STATEMENT OF FINANCIAL POSITION W$000 W$000 5504 W$ 000 REVENUE Materials Direct labour COST OF SALES -2877 -1080 - W$000 NON-CURRENT ASSETS: Property, plant & equipment 1944 Development costs 0 Investments Total Non Current Assets -3957 1944 1547 GROSS PROFIT OPERATING EXPENSES: R&D Marketing Administration Overheads Total Expenses -300 - 110 -278 -865 CURRENT ASSETS: Inventory Receivables Prepayments Cash at bank Total Current Assets TOTAL ASSETS 1503 1357 4 00000 -1553 2864 4808 -6 OPERATING PROFIT Investment income Interest receivable Interest payable NET FINANCE COST 0 0 -88 CURRENT LIABILITIES: Payables Bank overdraft Accruals Provisions Total Current Liabilities 1058 398 9 70 -88 -94 1535 PROFIT BEFORE TAX TAXATION PROFIT FOR THE YEAR -94 NON CURRENT LIABILITIES Long term loan 1000 Total Non Current Liabilities TOTAL LIABILITIES 1000 2535 STATEMENT OF CASH FLOWS NET ASSETS 2273 -0006 +0216 +0000 EQUITY: Share capital Share premium Retained profits 120 0 2153 TOTAL EQUITY 2273 Operating profit Add: Depreciation Add: Amortisation Change in working capital: 1. Inventory change 2. Receivables change 3. Prepayments change 4. Payables change 5. Accruals change 6. Provisions change Total change in working capital Cash generated from operations Finance income received Finance expenses paid Tax paid Net cash flow from operations PERFORMANCE INDICATORS -0514 +0102 -0004 -0105 +0009 +0070 -0442 -0232 +0000 -0088 -0000 -0320 Staff Morale Staff Skills Staff Turnover (%) Product Quality Consumer Satisfaction Retailer Satisfaction Brand Awareness (%) 5 5 13 5 4 6 10 Less: Purchase of PP&E Less: Purchase of intangible assets Less: Amount spent on investments Add: Investment income received Net cash flow from investing -0000 -0000 0000 +0000 +0000 Proceeds from share issue Draw down (repayment) of loan Dividend paid Net cash flow from financing +0000 +0000 -0000 +0000 Net Cash Flow -0320 Team 2. Bionic Sciences Plc. Year: 2031 KEY FINANCIAL RATIOS & METRICS SUPPLY AND DEMAND Return on Capital Employed (%) Return on Net Assets (%) Operating Margin (%) Gross Margin (%) Operating Expenses to Sales (%) Revenue on Capital Employed (W$) -0.2 -4.1 -0.1 28.2 28.2 1.68 Sales Volume (units) Lost Sales (units) Production (units) Total Capacity (units) 1251 0 1401 1632 GROSS PROFIT PER UNIT ANALYSIS (W$) Current Ratio Acid-Test Ratio Inventory Days Receivables Days Payables Days 1.87 0.89 139 90 98 Net sales price 4399 Material cost Direct labour cost Total cost 2300 863 3163 Gearing (%) Interest Cover EBITDA (W$ 000) Earnings per Share (W$) Share Price (W$) 38.1 -0.1 210 -0.78 19 Gross profit 1236 MESSAGES: Auditors report your stock levels are too high. Shareholders are concerned about your current financial performance. Completed R&D: MARKET SUMMARY Team 1 Team 2 Supply: Production (units) Closing Inventory (units) Lost Sales (units) Salaries (W$000 p.p. p.a.) 1401 471 0 10.0 10. Demand: Price 5500 Special Order Price 0 Market Share (%) 15.7 Sales Volume (units) 1251 Special Order Volume N.B. Special Order contracts are excluded from the Sales numbers & Market Share calculations Financials (W$000): Revenue Profit After Tax Net Assets Bank Overdraft 5504 -94 2273 398 3 World No. Team 2 Bionic Sciences PLC. Year: 2032 STATEMENT OF PROFIT OR LOSS STATEMENT OF FINANCIAL POSITION W$000 W$000 W$000 6838 REVENUE Materials Direct labour COST OF SALES -3249 -1483 W$000 NON-CURRENT ASSETS: Property, plant & equipment 1750 Development costs 960 Investments Total Non Current Assets -4732 2710 2106 GROSS PROFIT OPERATING EXPENSES: R&D Marketing Administration Overheads Total Expenses 948 1686 - 1040 - 160 -305 -860 CURRENT ASSETS: Inventory Receivables Prepayments Cash at bank Total Current Assets TOTAL ASSETS 00000 -2365 2634 5344 -259 0 OPERATING PROFIT Investment income Interest receivable Interest payable NET FINANCE COST -192 CURRENT LIABILITIES: Payables Bank overdraft Accruals Provisions Total Current Liabilities 965 657 0 -192 -451 1622 PROFIT BEFORE TAX TAXATION PROFIT FOR THE YEAR -451 NON CURRENT LIABILITIES Long term loan 1900 Total Non Current Liabilities TOTAL LIABILITIES 1900 3522 STATEMENT OF CASH FLOWS NET ASSETS 1822 -0259 +0194 +0240 EQUITY: Share capital Share premium Retained profits 120 0 1702 TOTAL EQUITY 1822 Operating profit Add: Depreciation Add: Amortisation Change in working capital: 1. Inventory change 2. Receivables change 3. Prepayments change 4. Payables change 5. Accruals change 6. Provisions change Total change in working capital Cash generated from operations Finance income received Finance expenses paid Tax paid Net cash flow from operations PERFORMANCE INDICATORS +0555 -0329 +0004 -0093 -0009 -0070 +0058 +0233 +0000 -0192 -0000 +0041 Staff Morale Staff Skills Staff Turnover (%) Product Quality Consumer Satisfaction Retailer Satisfaction Brand Awareness (%) 6 7 8 6 7 8 13 Less: Purchase of PP&E Less: Purchase of intangible assets Less: Amount spent on investments Add: Investment income received Net cash flow from investing -0000 - 1200 0000 +0000 - 1200 Proceeds from share issue Draw down (repayment) of loan Dividend paid Net cash flow from financing +0000 +0900 -0000 +0900 Net Cash Flow -0259 Team 2. Bionic Sciences PLC. Year: 2032 KEY FINANCIAL RATIOS & METRICS SUPPLY AND DEMAND Return on Capital Employed (%) Return on Net Assets (%) Operating Margin (%) Gross Margin (%) Operating Expenses to Sales (%) Revenue on Capital Employed (W$) - 7.0 - 24.8 -3.8 30.8 34.6 1.84 Sales Volume (units) Lost Sales (units) Production (units) Total Capacity (units) 1554 0 1401 1644 GROSS PROFIT PER UNIT ANALYSIS (W$) Current Ratio Acid-Test Ratio Inventory Days Receivables Days Payables Days 1.62 1.04 73 90 74 Net sales price 4400 Material cost Direct labour cost Total cost 2091 954 3045 58.4 Gearing (%) Interest Cover EBITDA (W$ 000) Earnings per Share (W$) Share Price (W$) -1.3 175 -3.76 9 Gross profit 1355 MESSAGES: Auditors report your stock levels are too high. Shareholders are concerned about your current financial performance. Completed R&D: 4, 16, MARKET SUMMARY Team 2 Supply: Production (units) Closing Inventory (units) Lost Sales (units) Sal 1401 318 0 11.0 fla Demand: Price 5500 Special Order Price 0 Market Share (%) 18.4 Sales Volume (units) 1554 Special Order Volume 0 N.B. Special Order contracts are excluded from the Sales numbers & Market share calculations Financials (W$000): Revenue 6838 Profit After Tax -451 Net Assets 1822 Bank Overdraft 657 010 7/8 3 World No. Team 2 Bionic Sciences PLC. Year: 2033 STATEMENT OF PROFIT OR LOSS STATEMENT OF FINANCIAL POSITION W$000 W$000 W$000 7773 REVENUE Materials Direct labour COST OF SALES -3422 - 1509 W$000 NON CURRENT ASSETS: Property, plant & equipment 1575 Development costs 912 Investments Total Non Current Assets -4931 2487 2842 GROSS PROFIT OPERATING EXPENSES: R&D Marketing Administration Overheads Total Expenses 592 1278 -448 -210 -305 -856 CURRENT ASSETS: Inventory Receivables Prepayments Cash at bank Total Current Assets TOTAL ASSETS 01084 -1819 2954 5441 1023 OPERATING PROFIT Investment income Interest receivable Interest payable NET FINANCE COST 0 0 -218 CURRENT LIABILITIES: Payables Bank overdraft Accruals Provisions Total Current Liabilities 1075 1075 0 0 @ -218 805 PROFIT BEFORE TAX TAXATION 1075 PROFIT FOR THE YEAR 805 NON CURRENT LIABILITIES Long term loan 1900 Total Non Current Liabilities TOTAL LIABILITIES 1900 2975 STATEMENT OF CASH FLOWS NET ASSETS 2466 +1023 +0175 +0288 EQUITY: Share capital Share premium Retained profits 120 0 2346 TOTAL EQUITY 2466 Operating profit Add: Depreciation Add: Amortisation Change in working capital: 1. Inventory change 2. Receivables change 3. Prepayments change 4. Payables change 5. Accruals change 6. Provisions change Total change in working capital Cash generated from operations Finance income received Finance expenses paid Tax paid Net cash flow from operations PERFORMANCE INDICATORS +0356 +0408 +0000 +0110 +0000 +0000 +0874 +2360 +0000 -0218 -0000 +2142 7 8 Staff Morale Staff Skills Staff Turnover (%) Product Quality Consumer Satisfaction Retailer Satisfaction Brand Awareness (%) OVO OY 7 1e 21 Less: Purchase of PP&E Less: Purchase of intangible assets Less: Amount spent on investments Add: Investment income received Net cash flow from investing -0000 -0240 0000 +0000 -0240 +0000 +0000 Proceeds from share issue Draw down (repayment) of loan Dividend paid Net cash flow from financing -0161 -0161 Net Cash Flow +1741 Task 2: Evaluation of Big Store Inc. Export Opportunity (25% of the coursework portfolio) Assume today's date is 1 January 2034. The Board of Directors has asked you to evaluate an opportunity to export robots to a potential new overseas retail customer, 'Big Store Inc.'. 'Big Store Inc.' would like to run a trial promotion of your robots. The company would like to buy 100 robots from your company in 2034 at a special net sales price of W$2,500 per robot. If the 2034 trial is successful, the company has indicated it is likely to double the order quantity and would be prepared to match the net price you charge to your home customers in 2035 Further information is provided below: 1. Special Equipment The robots for this contract with 'Big Store Inc.' will require some modifications from the standard robot which your company produces and this will involve additional annual fixed production overheads of W$25,000 to cover the cost of hiring the special equipment required for this purpose. 2. Raw Materials: Standard Components The robots manufactured for this order contract will require the same standard raw material components used in your business' regular production process. 3. Raw Materials: Special Components The robots required for this contract will also require some special component materials. The company has a stock of 150 units of these special components' in inventory which were purchased some years ago but which have been regarded as surplus to requirements and have been fully written off in the accounts. These 'special components' originally cost W$500 per unit and they currently cost W$600 per unit to purchase. If not used for this project, the inventory of 'special components' will be sold in 2034 for sales proceeds of W$400 per unit. One 'special component will be required per robot. 3 4. Staff Training Also, an extra W$12,000 as a 'one-off cost' for staff training will be required to ensure that production staff are able to use the special equipment required for this contract. 5. Use of Factory Space The project will require the use of some of the company's factory space which is currently surplus to requirements and would otherwise be sub-let, which would bring in income of W$16,000 in 2034. 6. Sales Staff Time One of your company's sales staff estimates she spent 20% of her working hours in 2033 on this project which included travelling for meetings with 'Big Store Inc.' executives. 7. Marketing Costs 'Big Store Inc.' will run a special advertising campaign in 2034 to support this trial which will cost W$80,000 but requires your company to pay for 50% of these costs. 8. Fixed Cost Recovery Rate For costing special projects such as this, your company has in the past applied a rate of 10% of net revenues arising when evaluating new orders in order to recover the business' recurring fixed costs (including admin expenses, overheads and direct labour costs). Required: Prepare a report for the Board of Directors in which you advise on whether or not the above order should be accepted. You should specifically address the following requirements: a) Explain the principles of relevant cost analysis, including the concept of 'opportunity costs! b) Calculate the annual total relevant cost and revenues of this order in both 2034 and thereafter using the table below: Workings Relevant cost/revenue 2034 w$ Relevant cost/revenue 2035 w$ 1. Special equipment 2. Raw materials: standard components 3. Raw materials: special components 4. Training 5. Use of factory space 6. Sales person's salary 7. Marketing costs 8. Fixed cost recovery rate Total relevant cost of the order (A) Total relevant revenue arising from the order (B) Surplus or deficit arising from the order (=B-A) c) Explain the reasoning for your treatment of each item (1 - 8) referred to in the information above as either relevant' or 'irrelevant' in your analysis as appropriate. Make clear any assumptions made. 5 d) Discuss two further considerations beyond the relevant cost analysis you have performed which you believe should be taken into account before a final decision is made. e) Advise management on whether the order should be accepted