Answered step by step

Verified Expert Solution

Question

1 Approved Answer

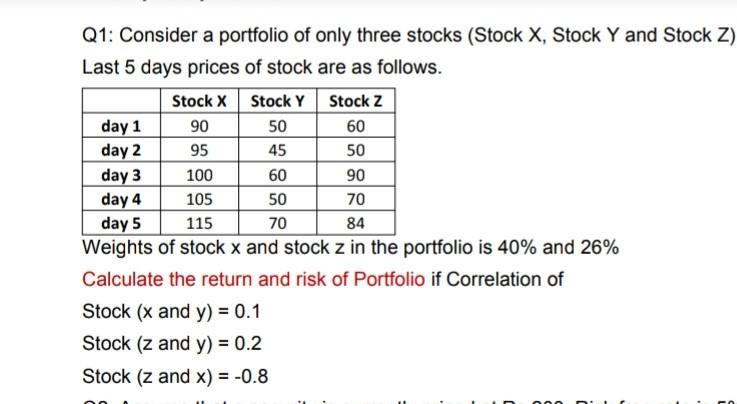

Q1: Consider a portfolio of only three stocks (Stock X, Stock Y and Stock Z) Last 5 days prices of stock are as follows. Stock

Q1: Consider a portfolio of only three stocks (Stock X, Stock Y and Stock Z) Last 5 days prices of stock are as follows. Stock x Stock Y Stock z day 1 90 50 60 day 2 95 45 50 day 3 100 60 90 day 4 105 50 70 day 5 115 70 84 Weights of stock x and stock z in the portfolio is 40% and 26% Calculate the return and risk of Portfolio if Correlation of Stock (x and y) = 0.1 Stock (z and y) = 0.2 Stock (z and x) = -0.8

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Pivotal Decade How The United States Traded Factories For Finance In The Seventies

Authors: Judith Stein

1st Edition

0300171501, 978-0300171501