Question

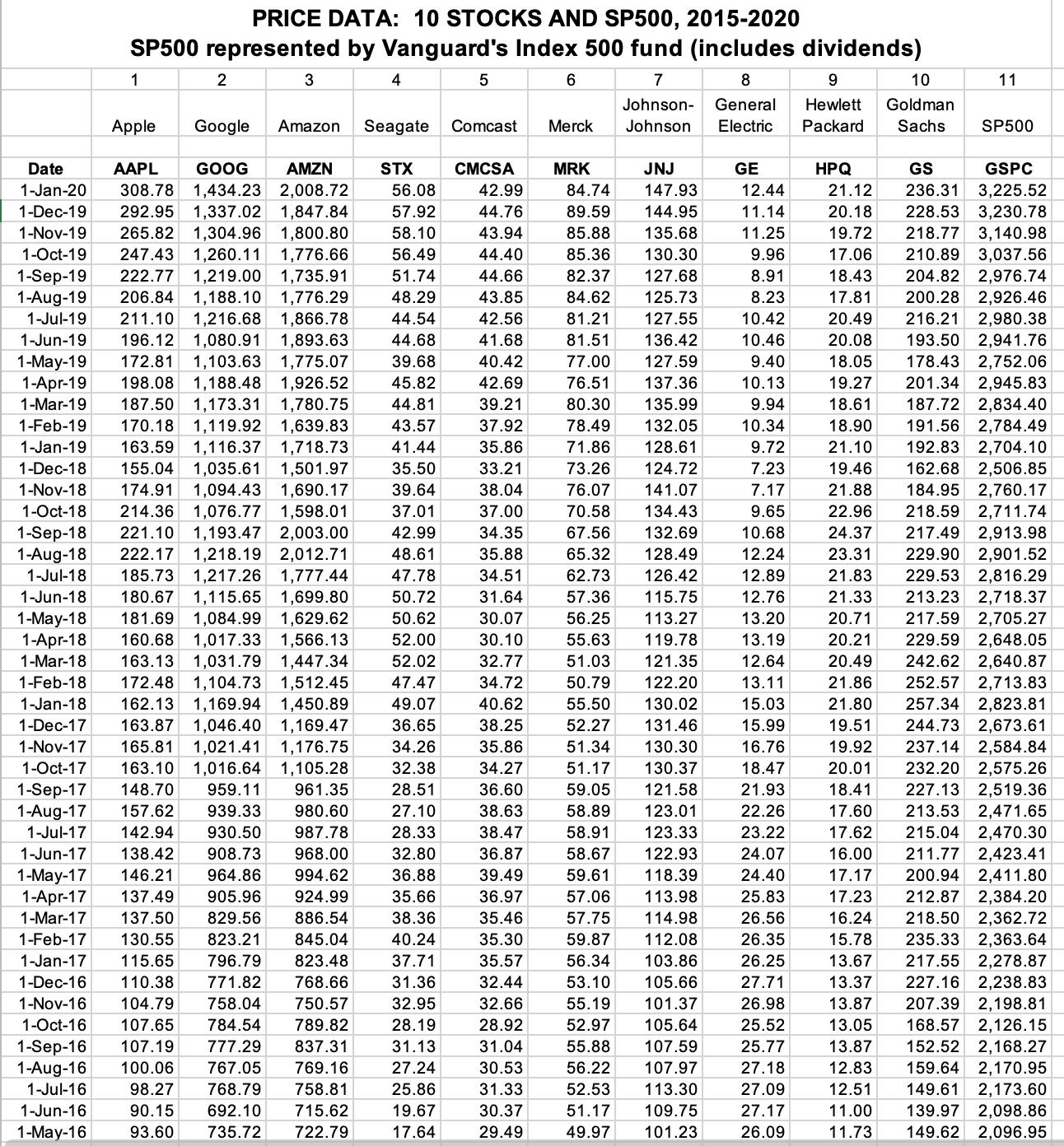

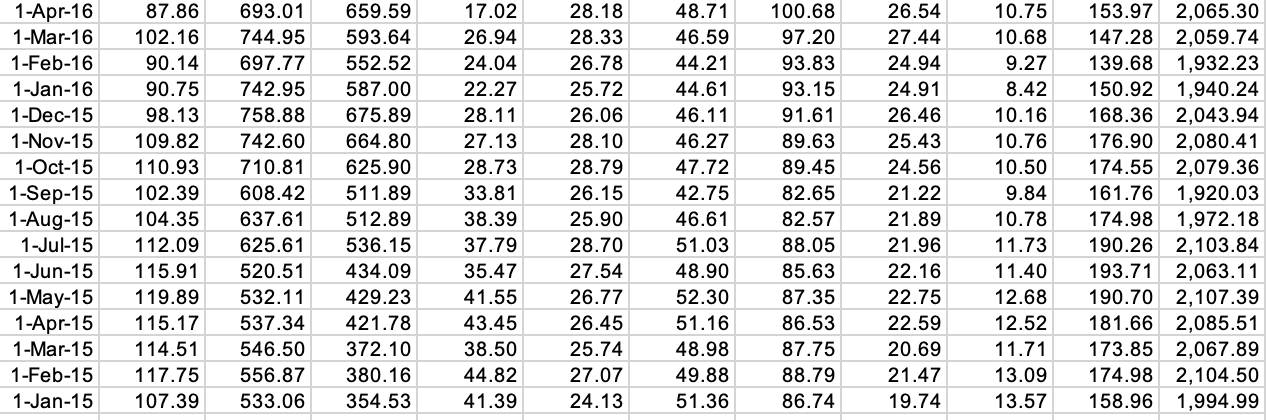

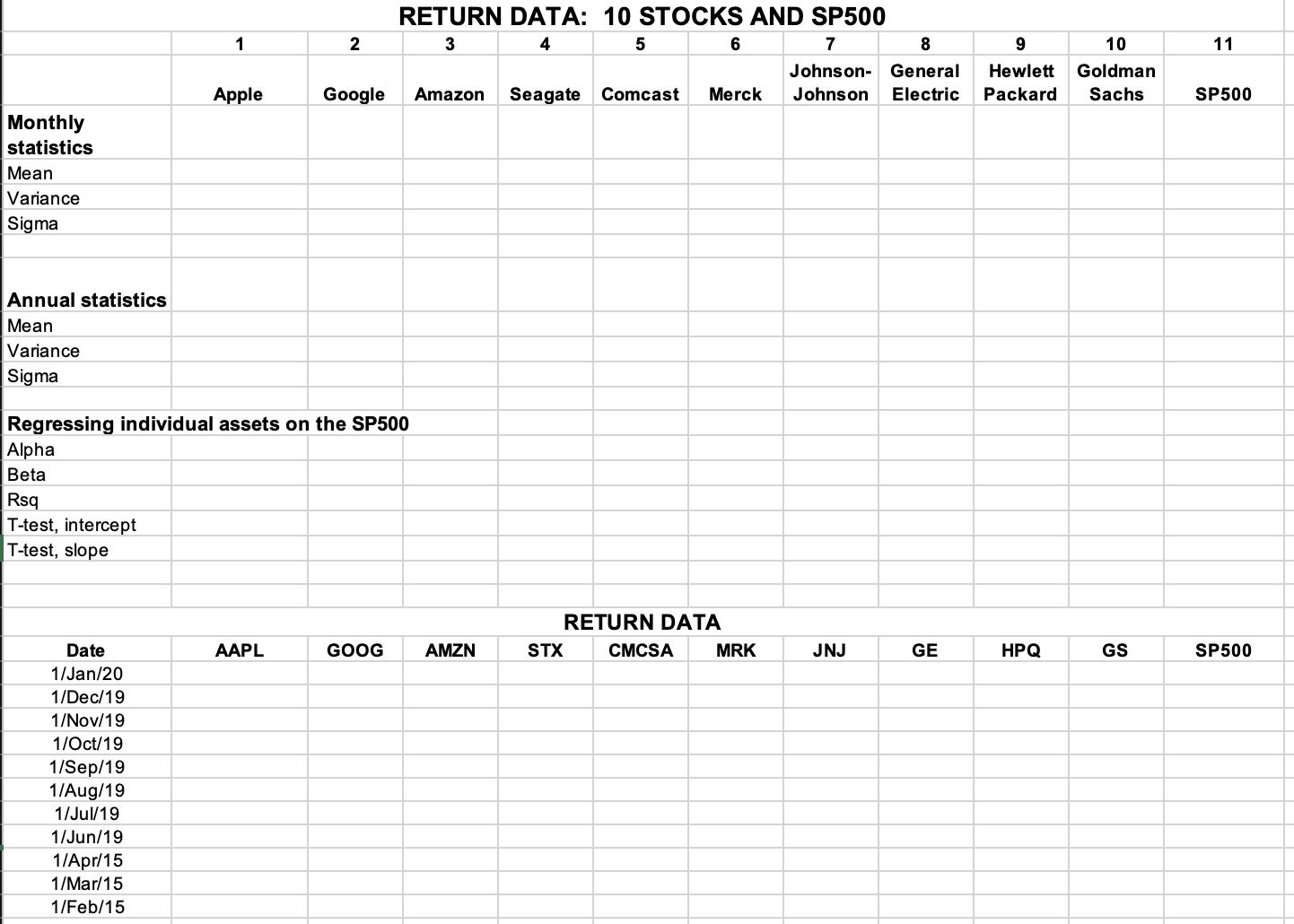

Q1: You are also given an Excel template in the attachment, please fill in the template file (in the second spreadsheet - calculating mean, variance,

Q1: You are also given an Excel template in the attachment, please fill in the template file (in the second spreadsheet - calculating mean, variance, and sigma of each stock).

Q2: Perform the second-pass regression: Regress the monthly average returns on the betas of the assets. Does this confirm that the S&P 500 is efficient?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A First Course in Differential Equations with Modeling Applications

Authors: Dennis G. Zill

11th edition

1305965728, 978-1305965720