Answered step by step

Verified Expert Solution

Question

1 Approved Answer

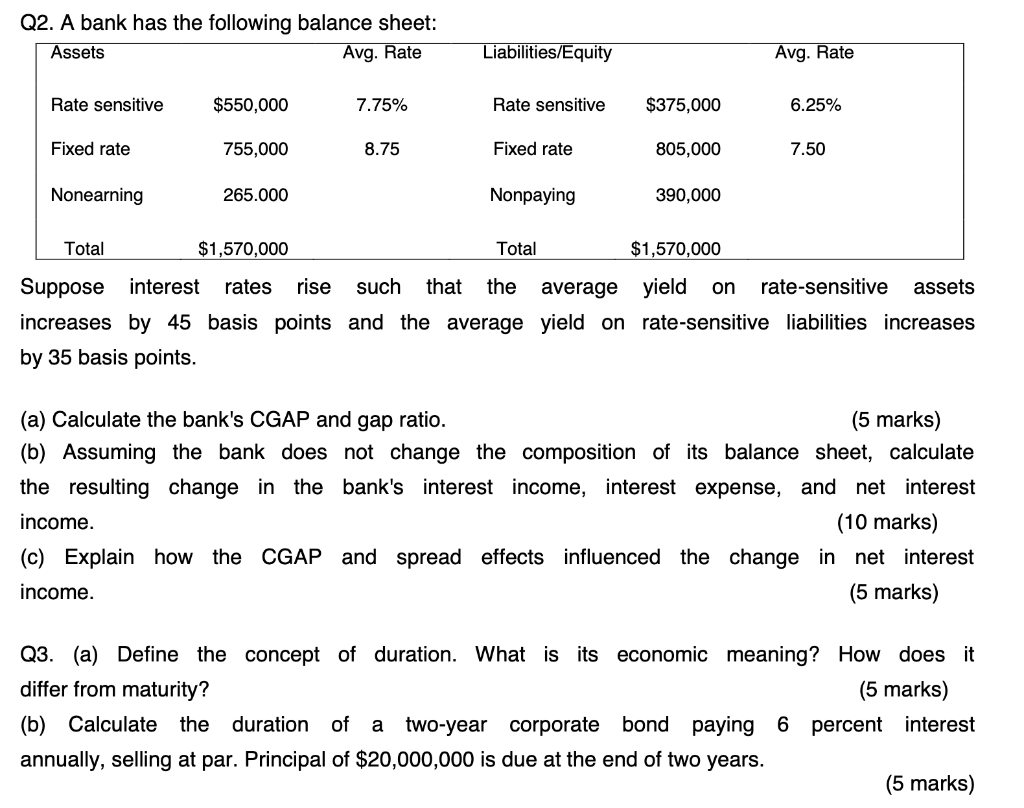

Q2. A bank has the following balance sheet: Assets Avg. Rate Liabilities/Equity Avg. Rate Rate sensitive $550,000 7.75% Rate sensitive $375,000 6.25% Fixed rate 755,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Future Of Financea The LSE Report

Authors: Chairman Adair Turner, Paul Woolley, Andrew Dr Haldane, Richard Layard, Andrew G. Haldane, Paul Wooley

1st Edition

085328458X, 978-0853284581