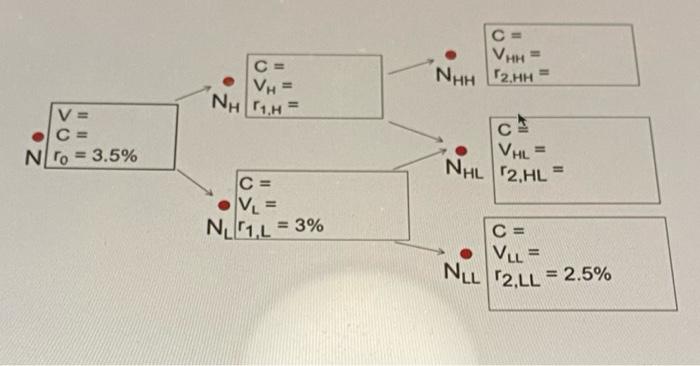

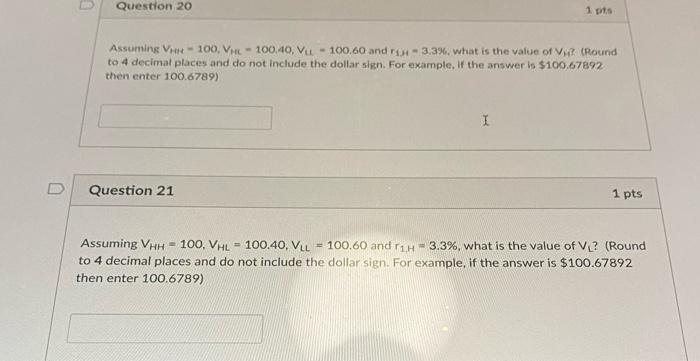

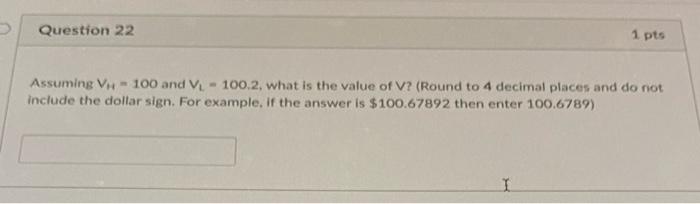

Use the following Information below to answer QUESTIONS 14-22 You have a 3% annual puttable bond that matures in three years. Assume o to be 7%. The bond is puttable at par (100). The option can be exercised any time after the first eighteen months. Using the binomial interest rate tree below answer the following questions, In the below higure you see the predicted interest rate trials for the outcomes when interest rates drop in both years going forward. Use what you have learned about building binomial trees to answer the following questions. I Remember: R1 is the one-year forward rate, at the start of year 2 Formula tip: Determine the corresponding value for the higher one-year forward rate from the lower one-year forward rate as r1(e) CE VH = NHH 2.HH . C= VW = NH 1.H V= C= No = 3.5% VHL= NHL 12.HL - C= .V= NL 1,2 = 3% C= VLL = NEL '2.LL = 2.5% Question 20 1 pts Assuming V-100, VHL - 100,40, Vu - 100.60 and - 3.3%, what is the value of V (Round to 4 decimal places and do not include the dollar sign. For example, if the answer is $100.67892 then enter 100.6789) 1 Question 21 1 pts Assuming VHH = 100, VHL - 100,40, VLL = 100.60 and 1-3.3%, what is the value of VL? (Round to 4 decimal places and do not include the dollar sign. For example, if the answer is $100.67892 then enter 100.6789) Question 22 1 pts Assuming V- 100 and V - 100.2, what is the value of V? (Round to 4 decimal places and do not include the dollar sign. For example, if the answer is $100.67892 then enter 100.6789) Use the following Information below to answer QUESTIONS 14-22 You have a 3% annual puttable bond that matures in three years. Assume o to be 7%. The bond is puttable at par (100). The option can be exercised any time after the first eighteen months. Using the binomial interest rate tree below answer the following questions, In the below higure you see the predicted interest rate trials for the outcomes when interest rates drop in both years going forward. Use what you have learned about building binomial trees to answer the following questions. I Remember: R1 is the one-year forward rate, at the start of year 2 Formula tip: Determine the corresponding value for the higher one-year forward rate from the lower one-year forward rate as r1(e) CE VH = NHH 2.HH . C= VW = NH 1.H V= C= No = 3.5% VHL= NHL 12.HL - C= .V= NL 1,2 = 3% C= VLL = NEL '2.LL = 2.5% Question 20 1 pts Assuming V-100, VHL - 100,40, Vu - 100.60 and - 3.3%, what is the value of V (Round to 4 decimal places and do not include the dollar sign. For example, if the answer is $100.67892 then enter 100.6789) 1 Question 21 1 pts Assuming VHH = 100, VHL - 100,40, VLL = 100.60 and 1-3.3%, what is the value of VL? (Round to 4 decimal places and do not include the dollar sign. For example, if the answer is $100.67892 then enter 100.6789) Question 22 1 pts Assuming V- 100 and V - 100.2, what is the value of V? (Round to 4 decimal places and do not include the dollar sign. For example, if the answer is $100.67892 then enter 100.6789)