Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Q29Q30 Use the following information to answer QUESTIONS 23 - 33 Current 1 year, 2 year and 3 year zero-coupon rates are 2.25%, 2.60% and

Q29Q30

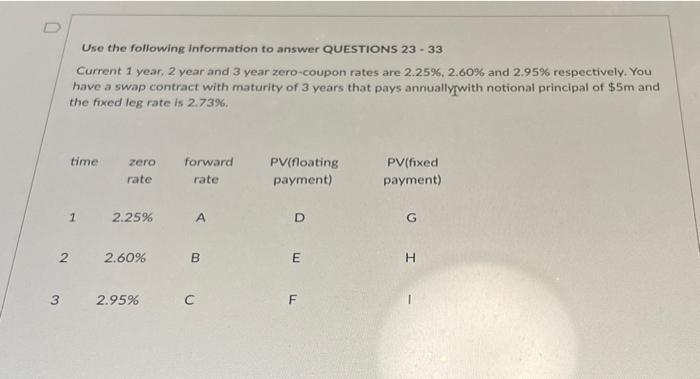

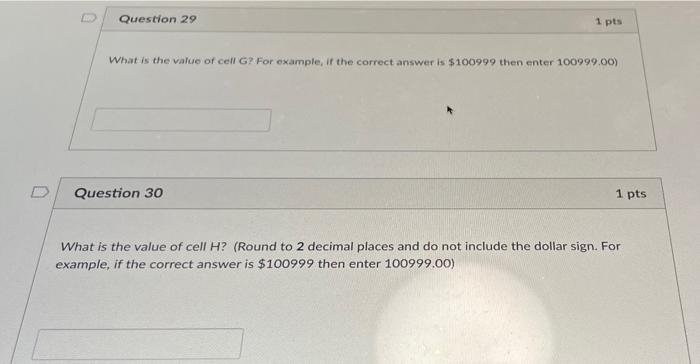

Use the following information to answer QUESTIONS 23 - 33 Current 1 year, 2 year and 3 year zero-coupon rates are 2.25%, 2.60% and 2.95% respectively. You have a swap contract with maturity of 3 years that pays annuallywith notional principal of $5m and the fixed leg rate is 2.73% time zero rate forward rate PV(floating payment) PV(fixed payment) 1 2.25% A D G 2 2.60% B E H 3 2.95% F Question 29 1 pts What is the value of cell G? For example, if the correct answer is $100999 then enter 100999.00) Question 30 1 pts What is the value of cell H? (Round to 2 decimal places and do not include the dollar sign. For example, if the correct answer is $100999 then enter 100999.00) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Occupational Pensions

Authors: Charles Sutcliffe

1st Edition

1349948624, 978-1349948628