Answered step by step

Verified Expert Solution

Question

1 Approved Answer

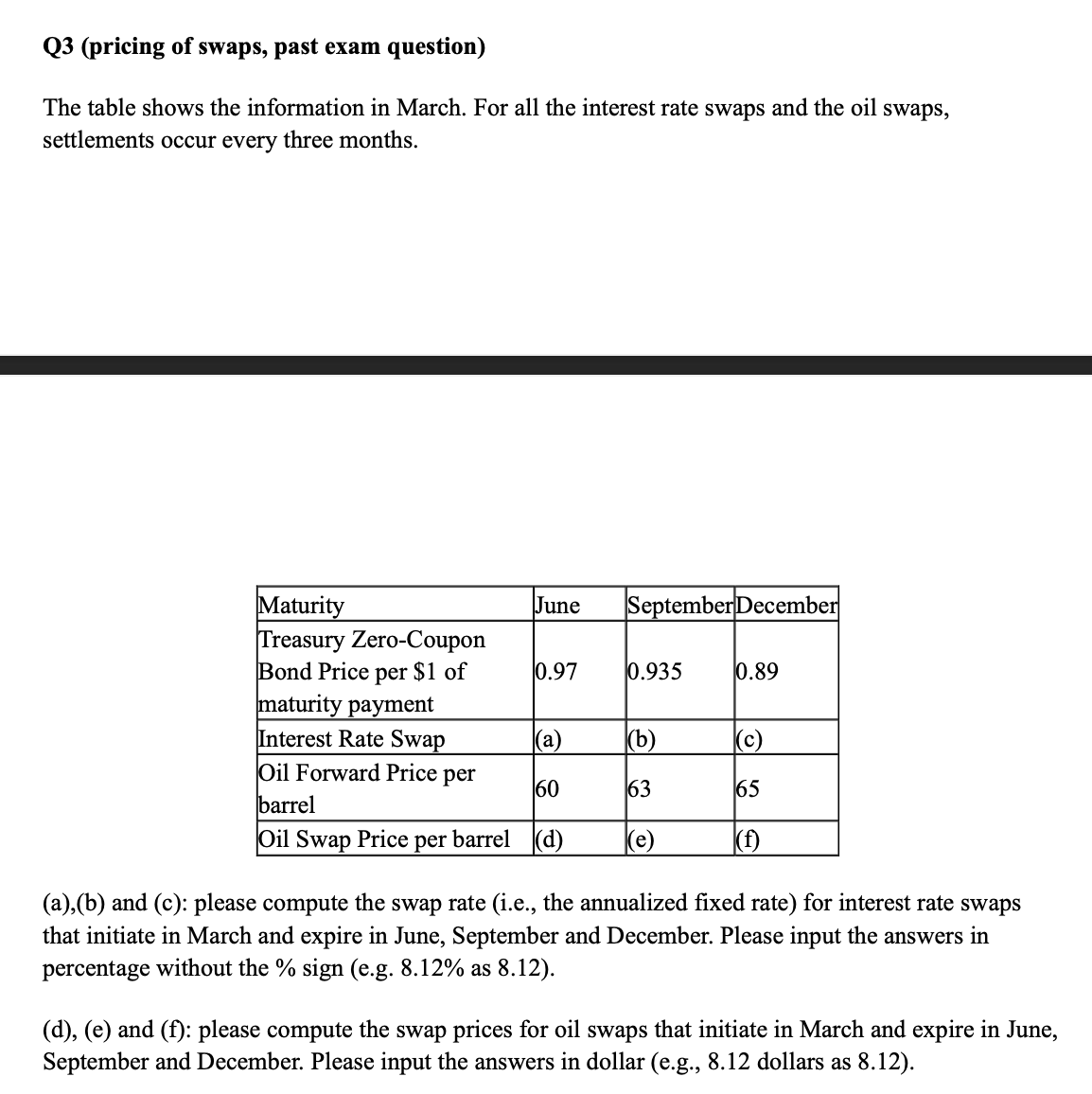

Q3 (pricing of swaps, past exam question) The table shows the information in March. For all the interest rate swaps and the oil swaps, settlements

Q3 (pricing of swaps, past exam question) The table shows the information in March. For all the interest rate swaps and the oil swaps, settlements occur every three months. (a),(b) and (c): please compute the swap rate (i.e., the annualized fixed rate) for interest rate swaps that initiate in March and expire in June, September and December. Please input the answers in percentage without the % sign (e.g. 8.12% as 8.12 ). (d), (e) and (f): please compute the swap prices for oil swaps that initiate in March and expire in June, September and December. Please input the answers in dollar (e.g., 8.12 dollars as 8.12)

Q3 (pricing of swaps, past exam question) The table shows the information in March. For all the interest rate swaps and the oil swaps, settlements occur every three months. (a),(b) and (c): please compute the swap rate (i.e., the annualized fixed rate) for interest rate swaps that initiate in March and expire in June, September and December. Please input the answers in percentage without the % sign (e.g. 8.12% as 8.12 ). (d), (e) and (f): please compute the swap prices for oil swaps that initiate in March and expire in June, September and December. Please input the answers in dollar (e.g., 8.12 dollars as 8.12) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The F And I Revolution Finance Reimagined

Authors: Michael A Bennett

1st Edition

1507777221, 978-1507777220