Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Q3 Stepl - The expected return and standard deviation of A are E(I3)=0.15, 1=0.1 - The expected return and standard deviation of B are E(r3)=0.25,

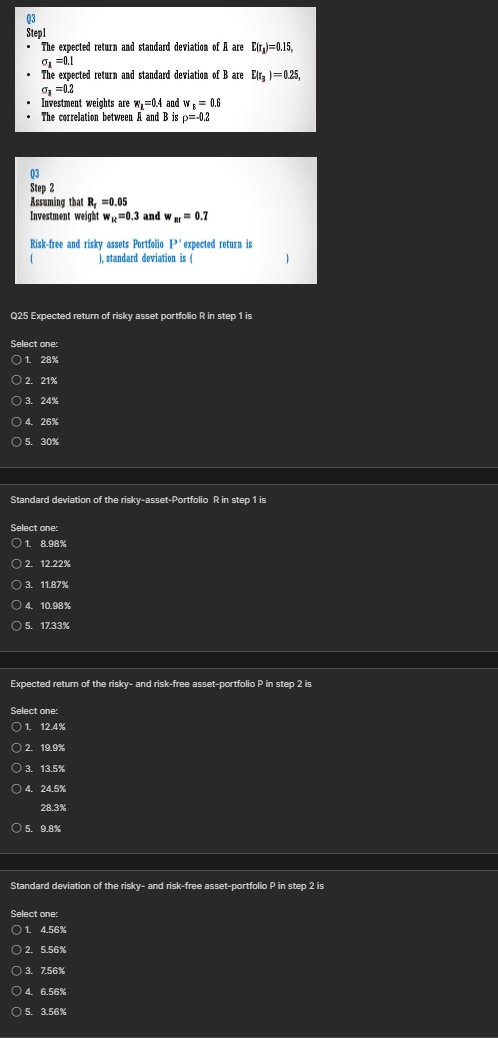

Q3 Stepl - The expected return and standard deviation of A are E(I3)=0.15, 1=0.1 - The expected return and standard deviation of B are E(r3)=0.25, 1=0.2 - Investment weights are FB=0.4 and wB=0.6 - The correlation between A and B is =0.2 Q3 Step 2 Assuming that Rt=0.05 Investment weight wR=0.3 and wnt=0.7 Risk-free and risky assets Portfolio P'expected return is I I, standard deviation is ( Q25 Expected return of risky asset portfolio R in step 1 is Select one? 1. 28% 2. 21% 3. 24% 4. 26% 5. 30% Standard deviation of the risky-asset-Portfolio R in step 1 is Select one: 1. 8.98% 2. 12.22% 3. 11.87% 4. 10.98% 5. 17.33% Expected return of the risky-and risk-free asset-portfolio P in step 2 is Select one: 1. 12.4% 2. 19.9% 3. 13.5% 4. 24.5% 28.3% 5. 9.8% Standard deviation of the risky-and risk-free asset-portfolio P in step 2 is Select one: 1. 4.56% 2. 5.56% 3. 7.56% 4. 6.56% 5. 3.56%

Q3 Stepl - The expected return and standard deviation of A are E(I3)=0.15, 1=0.1 - The expected return and standard deviation of B are E(r3)=0.25, 1=0.2 - Investment weights are FB=0.4 and wB=0.6 - The correlation between A and B is =0.2 Q3 Step 2 Assuming that Rt=0.05 Investment weight wR=0.3 and wnt=0.7 Risk-free and risky assets Portfolio P'expected return is I I, standard deviation is ( Q25 Expected return of risky asset portfolio R in step 1 is Select one? 1. 28% 2. 21% 3. 24% 4. 26% 5. 30% Standard deviation of the risky-asset-Portfolio R in step 1 is Select one: 1. 8.98% 2. 12.22% 3. 11.87% 4. 10.98% 5. 17.33% Expected return of the risky-and risk-free asset-portfolio P in step 2 is Select one: 1. 12.4% 2. 19.9% 3. 13.5% 4. 24.5% 28.3% 5. 9.8% Standard deviation of the risky-and risk-free asset-portfolio P in step 2 is Select one: 1. 4.56% 2. 5.56% 3. 7.56% 4. 6.56% 5. 3.56% Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essentials of Managerial Finance

Authors: Scott Besley, Eugene F. Brigham

14th edition

324422709, 324422702, 978-0324422702