Answered step by step

Verified Expert Solution

Question

1 Approved Answer

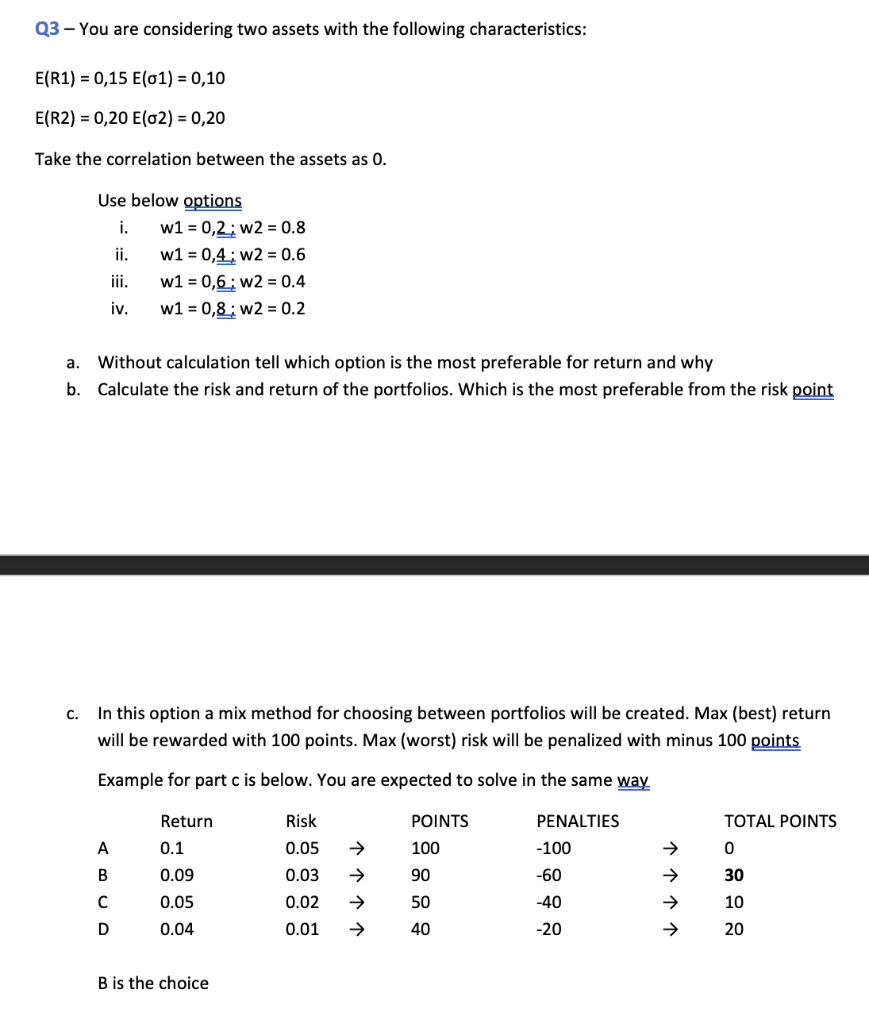

Q3 - You are considering two assets with the following characteristics: E(R1)=0,15E(1)=0,10E(R2)=0,20E(2)=0,20 Take the correlation between the assets as 0 . Use below options i.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Enterprise Risk Management Todays Leading Research And Best Practices For Tomorrows Executives

Authors: John R. S. Fraser, Rob Quail, Betty Simkins

1st Edition

1119741483, 978-1119741480