Answered step by step

Verified Expert Solution

Question

1 Approved Answer

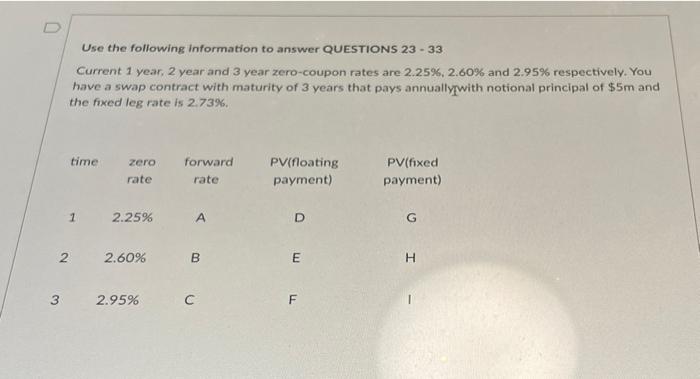

Q32 Use the following information to answer QUESTIONS 23 - 33 Current 1 year, 2 year and 3 year zero-coupon rates are 2.25%, 2.60% and

Q32

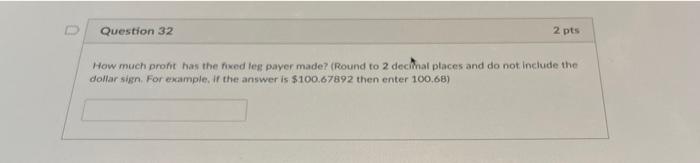

Use the following information to answer QUESTIONS 23 - 33 Current 1 year, 2 year and 3 year zero-coupon rates are 2.25%, 2.60% and 2.95% respectively. You have a swap contract with maturity of 3 years that pays annuallywith notional principal of $5m and the fixed leg rate is 2.73% time zero rate forward rate PV(floating payment) PV(fixed payment) 1 2.25% A D G 2 2.60% B E H 3 2.95% F Question 32 2 pts How much prohit has the fixed leg payer made? (Round to 2 decimal places and do not include the dollar sign For example, if the answer is $100.67892 then enter 100.68) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Global Financial Markets

Authors: Sabri Boubaker, Duc Khuong Nguyen

1st Edition

9813236647, 978-9813236646