Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Q5. [20 points total] Consider the following information for Amazon with average monthly returns for four well-diversified portfolios. The monthly risk-free rate is 0.1%.

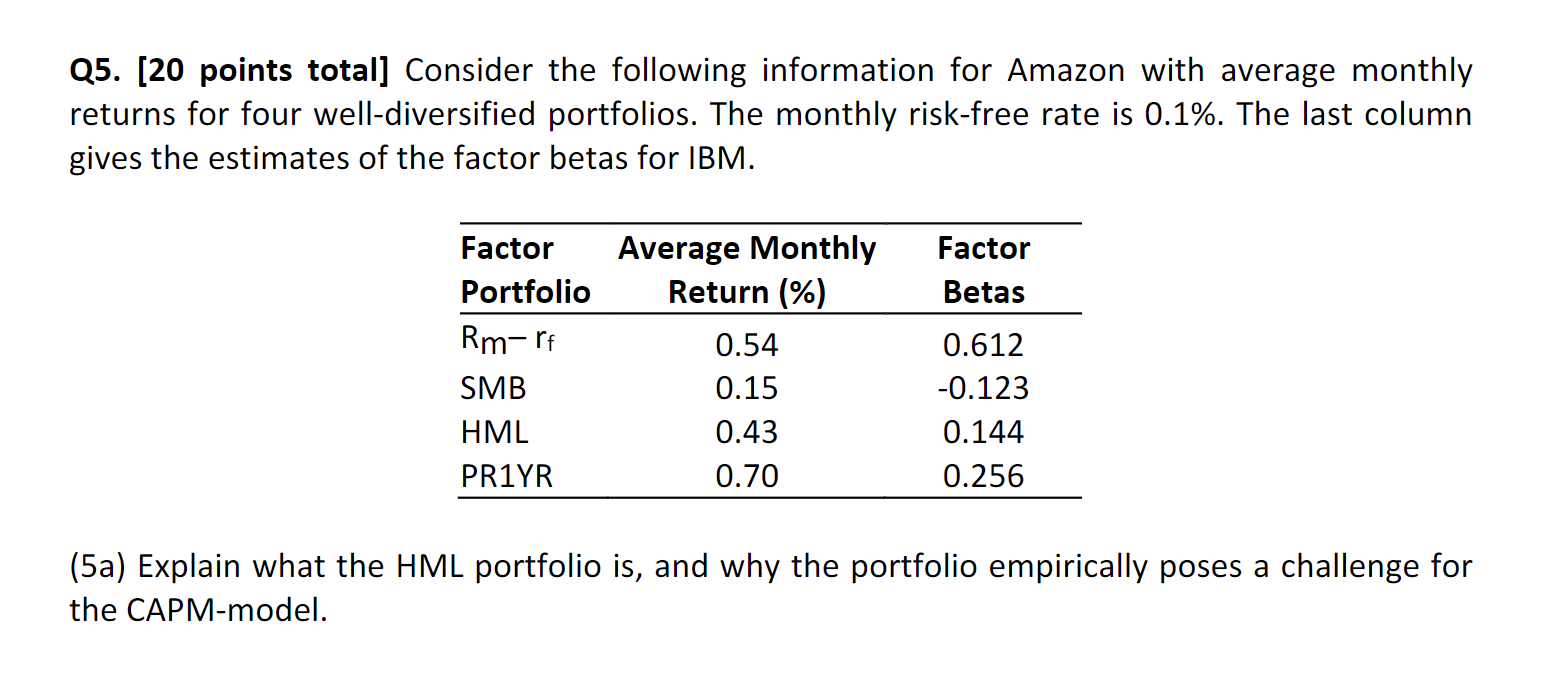

Q5. [20 points total] Consider the following information for Amazon with average monthly returns for four well-diversified portfolios. The monthly risk-free rate is 0.1%. The last column gives the estimates of the factor betas for IBM. Factor Portfolio Average Monthly Factor Return (%) Betas Rm-rf 0.54 0.612 SMB 0.15 -0.123 HML 0.43 0.144 PR1YR 0.70 0.256 (5a) Explain what the HML portfolio is, and why the portfolio empirically poses a challenge for the CAPM-model.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance for Non Financial Managers

Authors: Pierre Bergeron

7th edition

176530835, 978-0176530839