Answered step by step

Verified Expert Solution

Question

1 Approved Answer

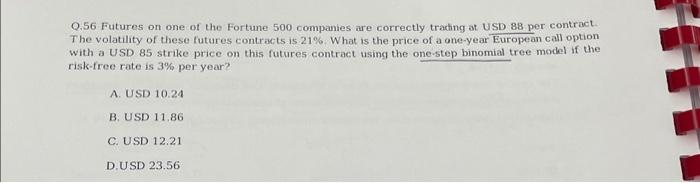

Q.56 Futures on one of the Fortune 500 companies are correctly trading at USD 88 per contract. The volatility of these futures contracts is 21%.

Q.56 Futures on one of the Fortune 500 companies are correctly trading at USD 88 per contract. The volatility of these futures contracts is 21%. What is the price of a one-year European call option with a USD 85 strike price on this futures contract using the one-step binomial tree model if the risk-free rate is 3% per year? A. USD 10.24 B. USD 11.86 C. USD 12.21 D.USD 23.56

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction To Social Media Marketing A Guide For Absolute Beginners

Authors: Todd Kelsey

1st Edition

1484228537, 978-1484228531