Answered step by step

Verified Expert Solution

Question

1 Approved Answer

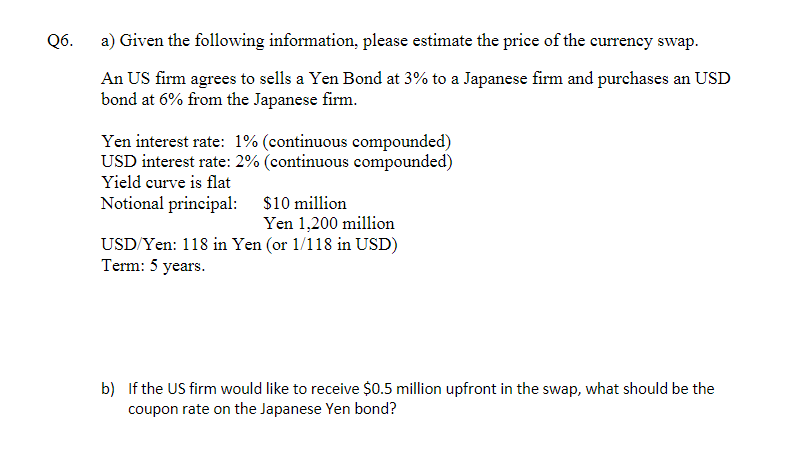

Q6. a) Given the following information, please estimate the price of the currency swap. An US firm agrees to sells a Yen Bond at 3%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting Tools For Business Decision Making Wileyplus Lms Student Package

Authors: Jerry J. Weygandt, Paul D. Kimmel, Donald E. Kieso

8th Edition

1119390249, 978-1119390244