Answered step by step

Verified Expert Solution

Question

1 Approved Answer

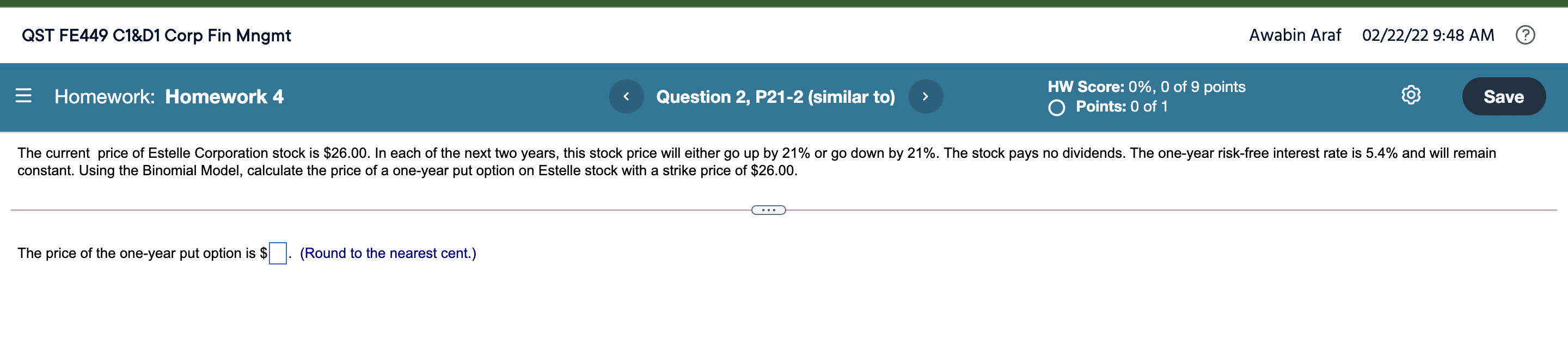

QST FE449 C1&D1 Corp Fin Mngmt Awabin Araf 02/22/22 9:48 AM = Homework: Homework 4 Question 2, P21-2 (similar to) > HW Score: 0%, 0

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Wealth Mastery Unveiled By Marcus M Dawson A Millennial S Guide To Financial Freedom And Success

Authors: Marcus M. Dawson

1st Edition

979-8865054313