Question 1 (1 point) an If price rises, what happens to quantity supplied for a product? Q It does not change. 0 Quantity supplied is

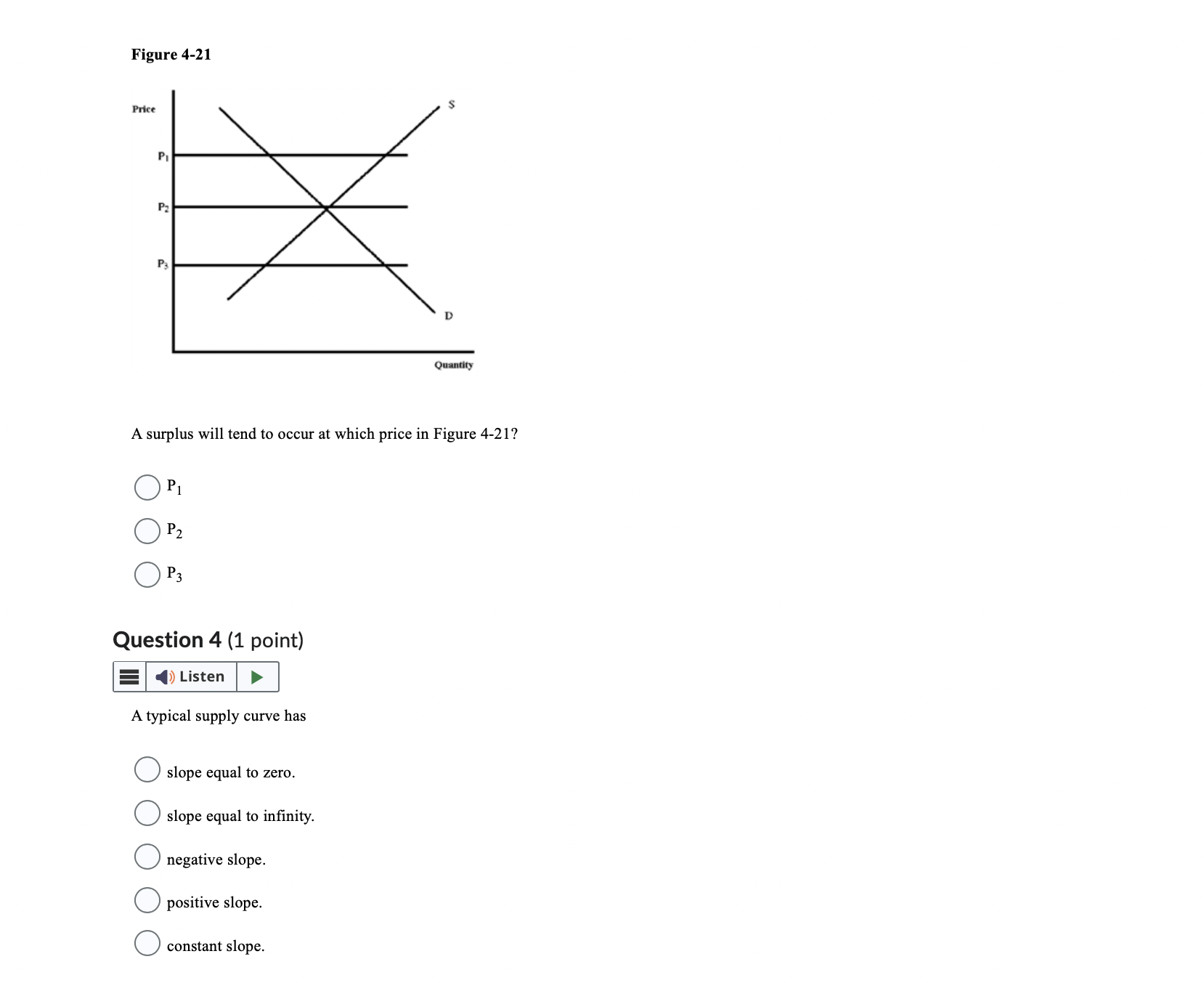

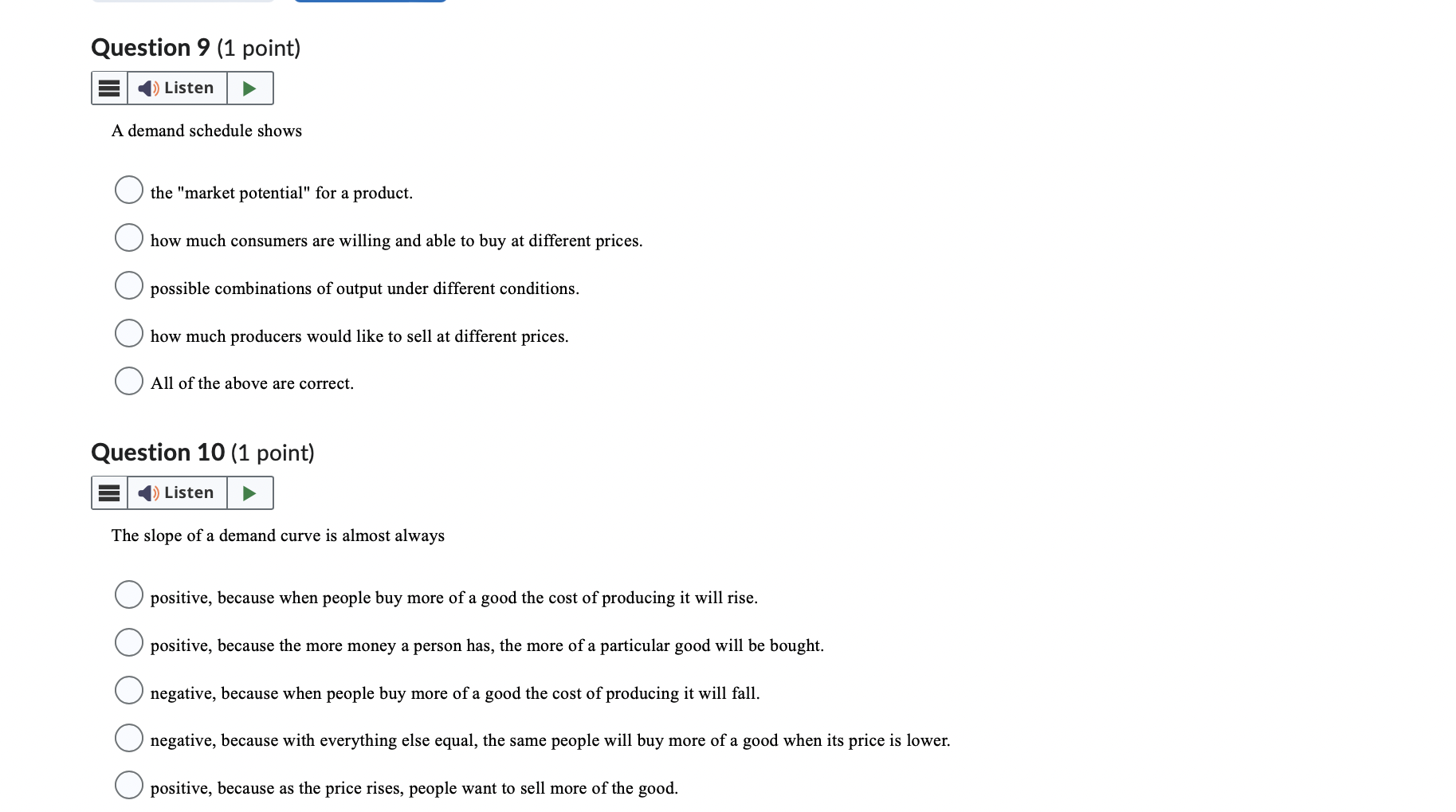

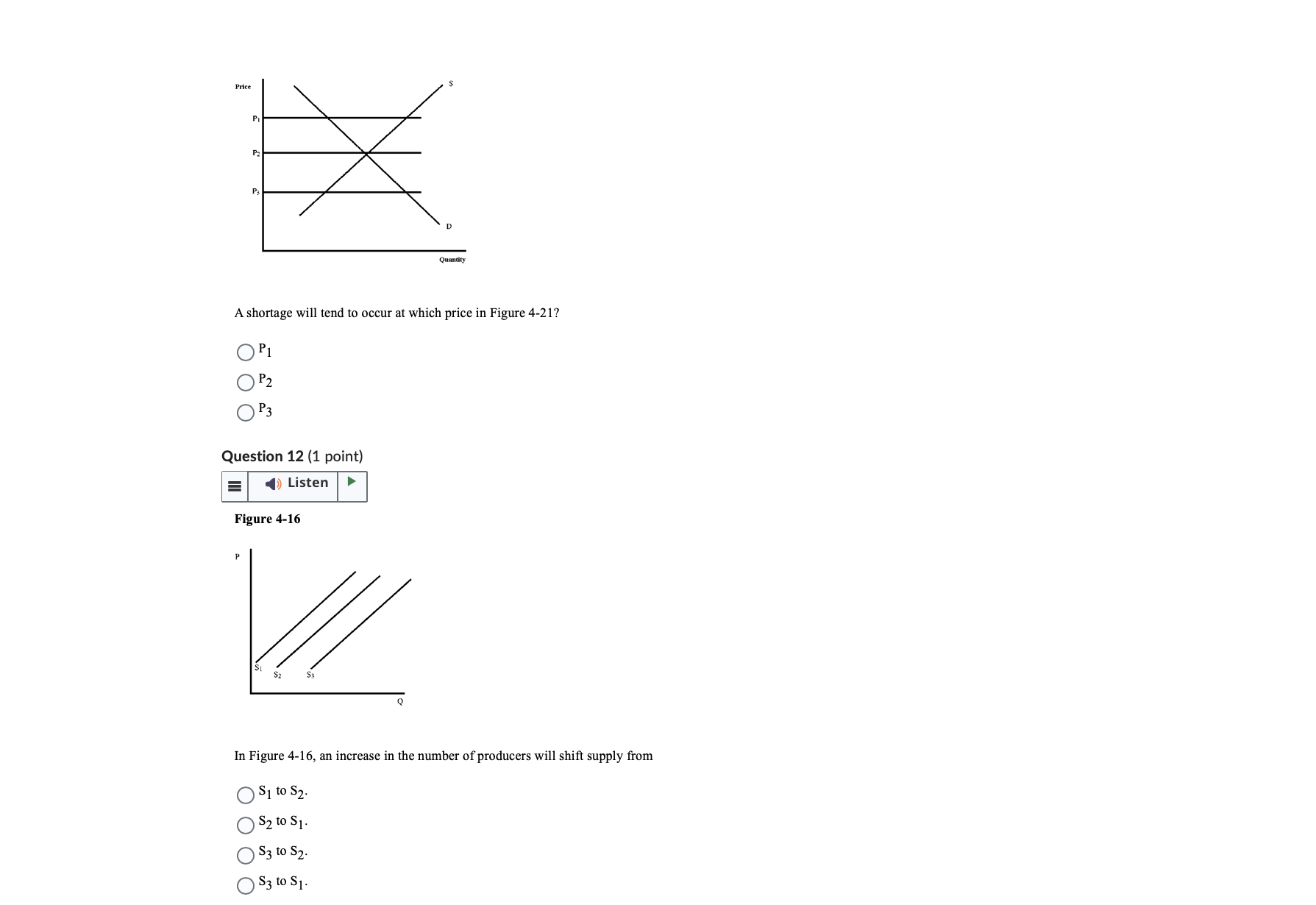

Question 1 (1 point) an If price rises, what happens to quantity supplied for a product? Q It does not change. 0 Quantity supplied is constant, but supply increases. Question 2 (1 point) E-Il An increase in demand will have what effect on equilibrium price and quantity? 0 Price will increase; quantity will decrease. 0 Price will decrease; quantity will increase. 0 Both price and quantity will increase. 0 Both price and quantity will decrease. Figure 4-21 Pure Pa A surplus will tend to occur at which price in Figure 4-21? Question 4 (1 point) E-Il A typical supply curve has 0 slope equal to zero. 0 slope equal to innity. O negative slope. 0 positive slope. O constant slope. Question 5 (1 point) The major drawback ofa price ceiling is O it causes a surplus. 0 government regulations of this kind are difficult to enforce. O it causes a shortage. Q There is no draw Jack. Question 6 (1 point) IEI 1)) Listen b Are markets always in equilibrium? 0 Yes, they are always at the equilibrium point, or very Close to it. 0 Yes, because few things tend to alter supply and demand. 0 No, but if there is no interference, they tend to move toward equilibrium. O No, they never "settle down" into a stable price and quantity. O Uncertain, economic theory has no answer to this question. Question 7 (1 point) E-II If price rises, what happens to supply for a product? 0 It does not change. 0 Uncertain-economic theory has no answer to this question. Question 8 (1 point) an The supply curve shows 0 the same basic information as the demand curve. 0 who will have an opportunity to produce or purchase an item. 0 the quantity produced as a function of the price. 0 plots of what quantities have been sold over the past few weeks or months. Question 9 (1 point) Listen A demand schedule shows the "market potential" for a product. O how much consumers are willing and able to buy at different prices. O possible combinations of output under different conditions. O how much producers would like to sell at different prices. All of the above are correct. Question 10 (1 point) Listen The slope of a demand curve is almost always O positive, because when people buy more of a good the cost of producing it will rise. O positive, because the more money a person has, the more of a particular good will be bought. O negative, because when people buy more of a good the cost of producing it will fall. negative, because with everything else equal, the same people will buy more of a good when its price is lower. OO positive, because as the price rises, people want to sell more of the good.Price Quantity A shortage will tend to occur at which price in Figure 4-21? OPI O P 2 OP3 Question 12 (1 point) Listen Figure 4-16 $2 In Figure 4-16, an increase in the number of producers will shift supply from O S1 to $2. O S2 to $1 O S3 to $2. O S3 to $1

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance