Answered step by step

Verified Expert Solution

Question

1 Approved Answer

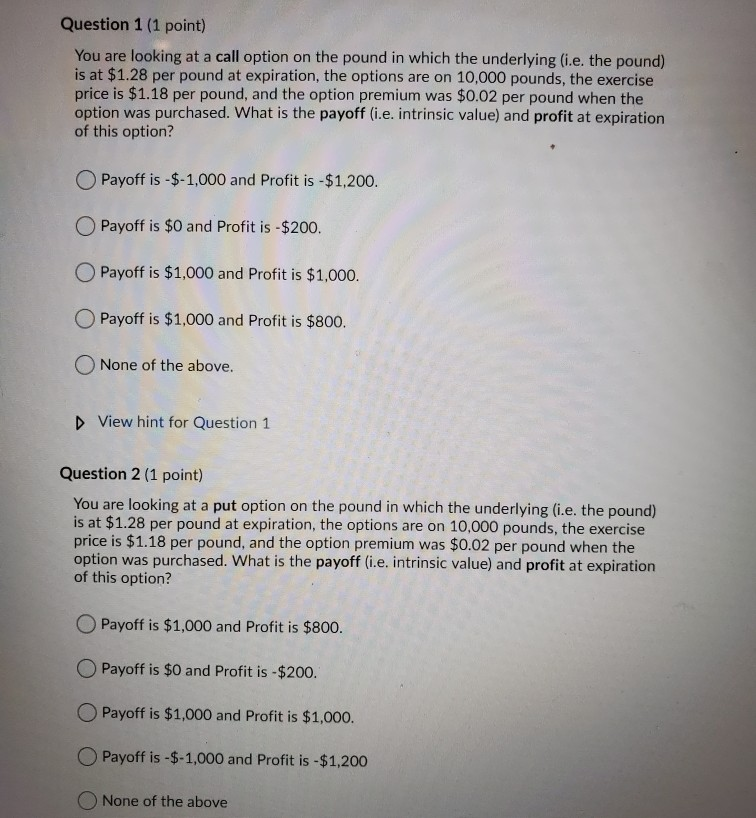

Question 1 (1 point) You are looking at a call option on the pound in which the underlying (i.e. the pound) is at $1.28 per

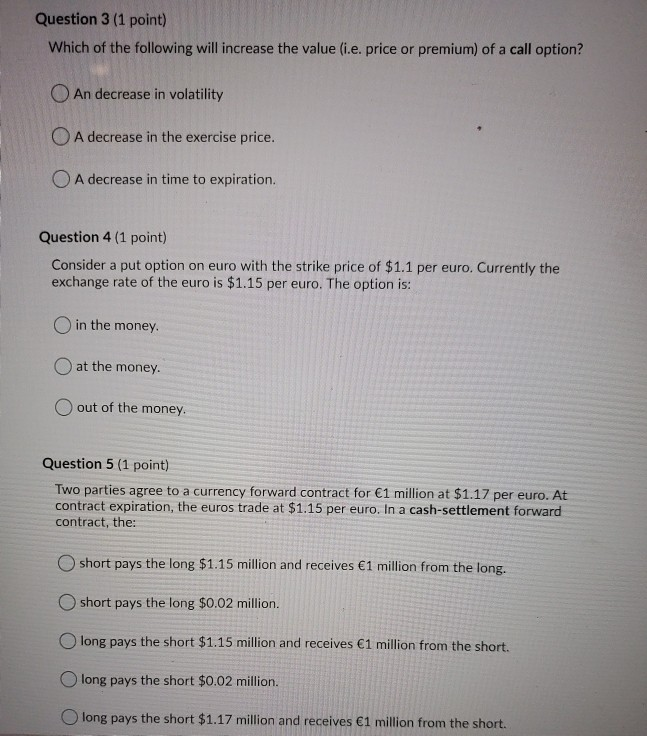

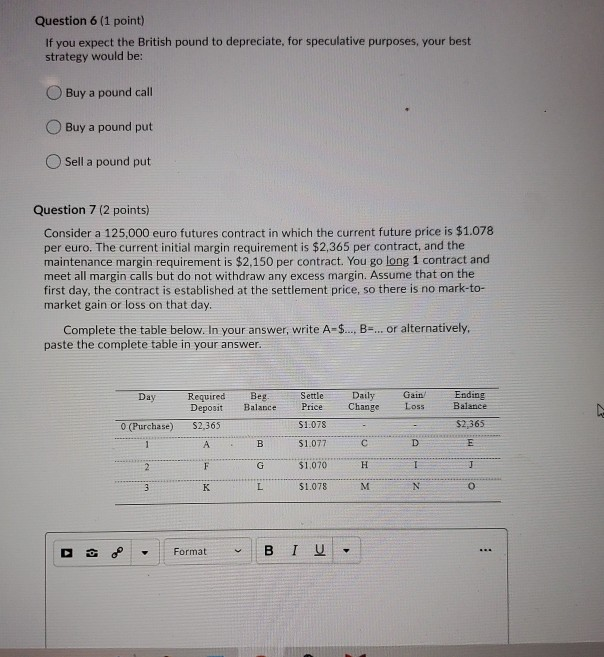

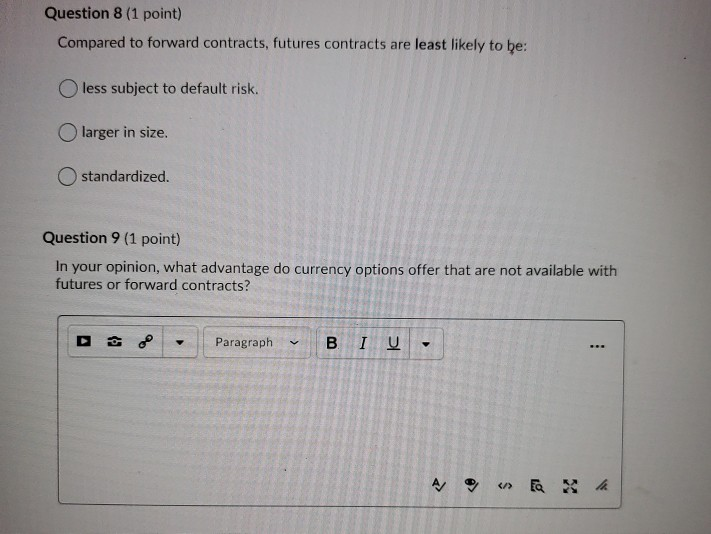

Question 1 (1 point) You are looking at a call option on the pound in which the underlying (i.e. the pound) is at $1.28 per pound at expiration, the options are on 10,000 pounds, the exercise price is $1.18 per pound, and the option premium was $0.02 per pound when the option was purchased. What is the payoff (i.e. intrinsic value) and profit at expiration of this option? O Payoff is - $-1,000 and Profit is -$1,200. Payoff is $0 and Profit is - $200. Payoff is $1,000 and Profit is $1,000. O Payoff is $1,000 and Profit is $800. None of the above. View hint for Question 1 Question 2 (1 point) You are looking at a put option on the pound in which the underlying (i.e. the pound) is at $1.28 per pound at expiration, the options are on 10,000 pounds, the exercise price is $1.18 per pound, and the option premium was $0.02 per pound when the option was purchased. What is the payoff (i.e. intrinsic value) and profit at expiration of this option? Payoff is $1,000 and Profit is $800. O Payoff is $0 and Profit is - $200. Payoff is $1,000 and Profit is $1,000. O Payoff is - $-1,000 and Profit is -$1,200 None of the above Question 3 (1 point) Which of the following will increase the value (i.e. price or premium) of a call option? An decrease in volatility A decrease in the exercise price. O A decrease in time to expiration. Question 4 (1 point) Consider a put option on euro with the strike price of $1.1 per euro. Currently the exchange rate of the euro is $1.15 per euro. The option is: O in the money. at the money. O out of the money Question 5 (1 point) Two parties agree to a currency forward contract for 1 million at $1.17 per euro. At contract expiration, the euros trade at $1.15 per euro. In a cash-settlement forward contract, the: Oshort pays the long $1.15 million and receives 1 million from the long. short pays the long $0.02 million. long pays the short $1.15 million and receives 1 million from the short. long pays the short $0.02 million. long pays the short $1.17 million and receives 1 million from the short. Question 6 (1 point) If you expect the British pound to depreciate, for speculative purposes, your best strategy would be: Buy a pound call Buy a pound put Sell a pound put Question 7 (2 points) Consider a 125,000 euro futures contract in which the current future price is $1.078 per euro. The current initial margin requirement is $2,365 per contract, and the maintenance margin requirement is $2,150 per contract. You go long 1 contract and meet all margin calls but do not withdraw any excess margin. Assume that on the first day, the contract is established at the settlement price, so there is no mark-to- market gain or loss on that day. Complete the table below. In your answer, write A-$..., B-... or alternatively, paste the complete table in your answer. Day Required Deposit S2,365 Beg Balance Settle Price Daily Change Gain Loss Ending Balance $2,365 (Purchase) $1.078 B $1.077 D E F G $1.070 I 2 3 K L $1.078 M N 0 Format I o Question 8 (1 point) Compared to forward contracts, futures contracts are least likely to be: less subject to default risk. larger in size standardized. Question 9 (1 point) In your opinion, what advantage do currency options offer that are not available with futures or forward contracts? Paragraph

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fanatical Prospecting The Ultimate Guide To Opening Sales Conversations And Filling The Pipeline By Leveraging Social Selling Telephone Email Text And Cold Calling

Authors: Jeb Blount, Mike Weinberg

1st Edition

1119144752, 978-1119144755