Answered step by step

Verified Expert Solution

Question

1 Approved Answer

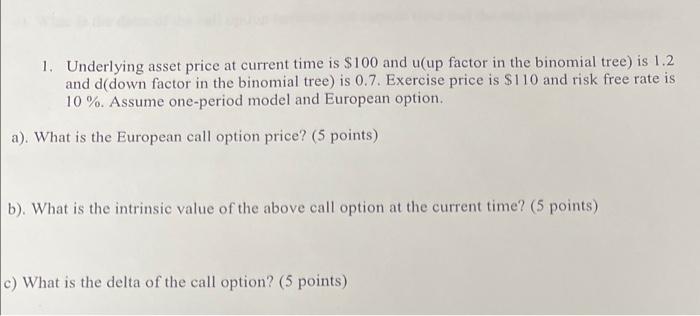

question 1 1. Underlying asset price at current time is $100 and u(up factor in the binomial tree) is 1.2 and d(down factor in the

question 1  1. Underlying asset price at current time is $100 and u(up factor in the binomial tree) is 1.2 and d(down factor in the binomial tree) is 0.7. Exercise price is $110 and risk free rate is 10 %. Assume one-period model and European option. a). What is the European call option price? (5 points) b). What is the intrinsic value of the above call option at the current time? (5 points) c) What is the delta of the call option? (5 points)

1. Underlying asset price at current time is $100 and u(up factor in the binomial tree) is 1.2 and d(down factor in the binomial tree) is 0.7. Exercise price is $110 and risk free rate is 10 %. Assume one-period model and European option. a). What is the European call option price? (5 points) b). What is the intrinsic value of the above call option at the current time? (5 points) c) What is the delta of the call option? (5 points)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Globalization Gating And Risk Finance

Authors: Unurjargal Nyambuu, Charles S. Tapiero

1st Edition

1119252652, 978-1119252658