Answered step by step

Verified Expert Solution

Question

1 Approved Answer

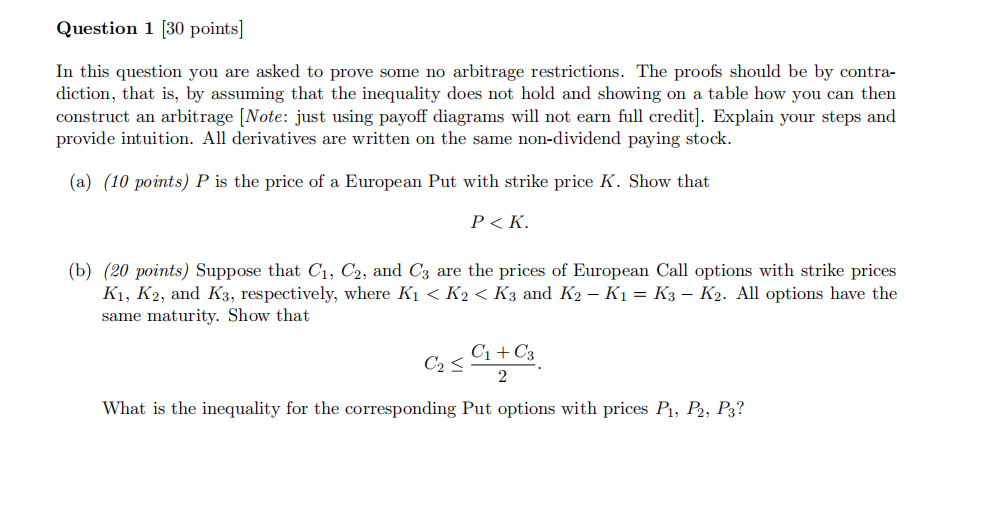

Question 1 [30 points] In this question you are asked to prove some no arbitrage restrictions. The proofs should be by contra- diction, that

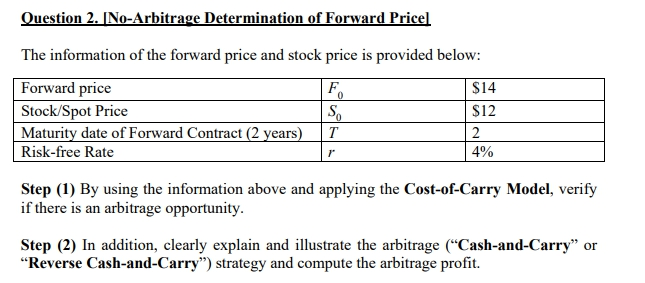

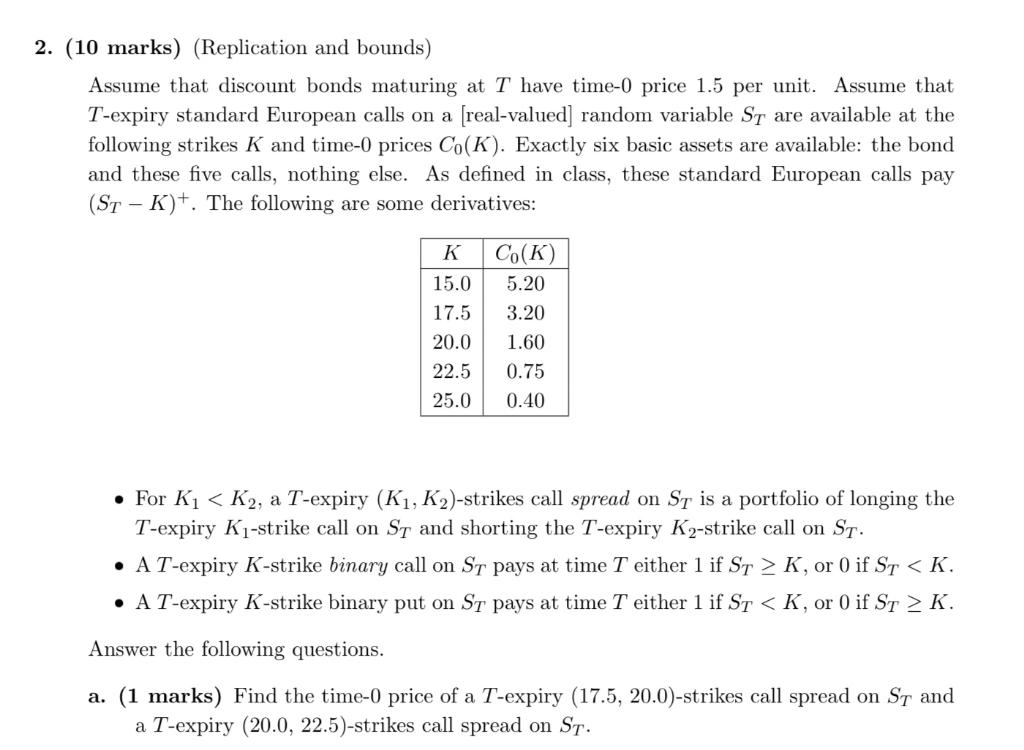

Question 1 [30 points] In this question you are asked to prove some no arbitrage restrictions. The proofs should be by contra- diction, that is, by assuming that the inequality does not hold and showing on a table how you can then construct an arbitrage [Note: just using payoff diagrams will not earn full credit]. Explain your steps and provide intuition. All derivatives are written on the same non-dividend paying stock. (a) (10 points) P is the price of a European Put with strike price K. Show that P Question 2. [No-Arbitrage Determination of Forward Price] The information of the forward price and stock price is provided below: Forward price F 0 Stock/Spot Price So Maturity date of Forward Contract (2 years) Risk-free Rate T r $14 $12 2 4% Step (1) By using the information above and applying the Cost-of-Carry Model, verify if there is an arbitrage opportunity. Step (2) In addition, clearly explain and illustrate the arbitrage ("Cash-and-Carry" or "Reverse Cash-and-Carry") strategy and compute the arbitrage profit. 2. (10 marks) (Replication and bounds) Assume that discount bonds maturing at T have time-0 price 1.5 per unit. Assume that T-expiry standard European calls on a [real-valued] random variable ST are available at the following strikes K and time-0 prices Co(K). Exactly six basic assets are available: the bond and these five calls, nothing else. As defined in class, these standard European calls pay (STK). The following are some derivatives: K Co(K) 15.0 5.20 17.5 3.20 20.0 1.60 22.5 0.75 25.0 0.40 For K < K2, a T-expiry (K1, K2)-strikes call spread on ST is a portfolio of longing the T-expiry K-strike call on ST and shorting the T-expiry K2-strike call on ST. AT-expiry K-strike binary call on ST pays at time T either 1 if ST > K, or 0 if ST < K. A T-expiry K-strike binary put on ST pays at time T either 1 if ST < K, or 0 if ST > K. Answer the following questions. a. (1 marks) Find the time-0 price of a T-expiry (17.5, 20.0)-strikes call spread on ST and a T-expiry (20.0, 22.5)-strikes call spread on ST.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial statements

Authors: Stephen Barrad

5th Edition

978-007802531, 9780324186383, 032418638X